ON DECK FOR WEDNESDAY, SEPTEMBER 3

KEY POINTS:

- Idiosyncratic local market developments await Friday’s payrolls

- Aussie dollar and yields lit up by GDP

- Won leads the pack on Korean GDP beat

- Turkish yields rocked by CPI

- US JOLTS—who cares?!

- US and Canadian vehicle sales on tap

- More hawkish ECB talk

- Oxymoronic Canadian productivity

- Carney’s retreat faces the unknowable on tariff and trade risks

Light overnight developments face a similarly light N.A. line-up of calendar-based developments, although there are a few gems worth considering. US Ts have a slight cheapening bias with 10s at about 4¼% but bigger rate and FX moves are occurring in markets like Australia, Korea and beleaguered Turkey. We’ve hit our year-end forecast for US 10s already but I’m not leaning toward major forecast changes going forward. Equities are broadly higher across US futures and European cash markets with the TSX lagging.

AUSTRALIA’S RESILIENT ECONOMY LIFTS A$ AND RATES

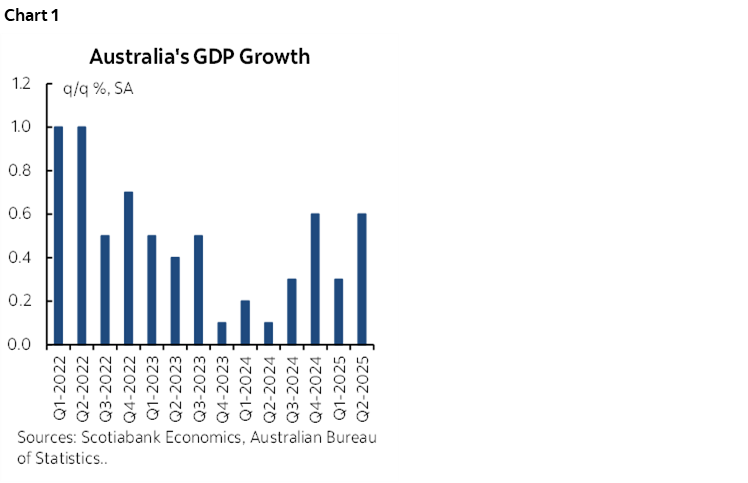

Australian yields spiked overnight led by a 7bps rise toward the front-end. The main culprit was Q2 GDP that surprised a touch higher than expected (0.6% q/q SA, 0.5% consensus), or 2.4% annualized, and with upward revisions (0.3% instead of 0.2% for Q1). Q2 growth tied with 2024Q4 growth for the strongest rates since the final quarter of 2022 (chart 1). Australia, it seems, has been resilient to global trade skirmishes and other considerations—at least so far. More impressive is that final domestic demand contributed a weighted 0.5% q/q SA nonannualized to GDP growth, with consumption adding 0.4 ppts. Exports add 0.5 ppts to GDP growth offset in part by a 0.3 ppts drag from imports. Inventories subtracted -0.1%.

EUROPEAN YIELDS STABILIZE FOR NOW

Across the pond, markets are largely shaking off ECB comments and the slow motion train wreck that is the UK government’s finances faces at least temporary calm today. Slovenia’s acting Governor expressed support for an ECB hold now but that the next move could either be down or up and said there is no reason to push through major forecast revisions at next week’s decision that would swing things in either direction. This follows comments by ECB Executive Board member Schnabel when she said yesterday that she does not see a reason for further easing, that policy is already accommodative, and that tariffs “are on net inflationary” while warning about the direction of future rate moves.

WON BUOYED BY GDP

South Korea’s economy also surprised to the upside with Q2 GDP up 0.7% q/q SA nonannualized (0.6% consensus). The won is the star pupil in FX land this morning.

TURKEY’S INESCAPABLE WOES

Turkey just can’t escape its woes. After yesterday’s assault on the opposition, today we have a mild upside surprise to inflation. CPI was up 2% m/m (1.75% consensus) and 33% y/y (32.6% consensus). Turkey’s 2-year yield climbed 52bps in a bear flattener move.

MINOR N.A. DATA RELEASES

US markets will monitor JOLTS job openings (10amET) that have basically been moving sideways along a mildly noisy path for about a year now (chart 2). They’ve been bouncing between 7–8 million postings throughout that whole period after declining from the early 2022 peak. It’s a lousy gauge for purposes of predicting payrolls. JOLTS has its own data issues, like the fact it lags, is prone to big revisions, has data collection issues, dead postings, and duplicate postings (or worse). And postings are a gross measure that speaks little in relation to net nonfarm payrolls.

The US also refreshes factory orders (10amET) that will fall given we already have the -2.8% drop in durable goods orders subject to revision, but in a more moderated sense if nondurable goods hold up better than the airplane effect on durables.

Also watch for auto sales in the US and Canada toward the end of the day. Industry guidance points to a decline in the US but to a still robust print of over 16 million SAAR. Canadian sales have held up well and had increased in July. There has been less tariff front-running in Canada because—unlike the US—tariffs don’t apply across the board which affords room for substitution effects.

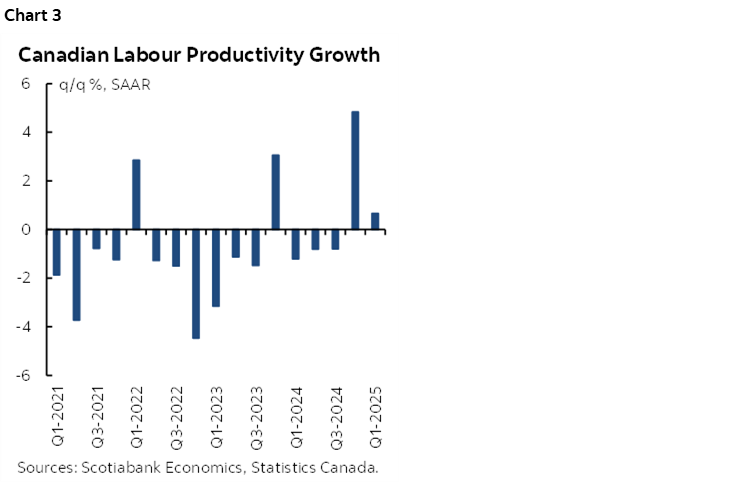

‘Canadian productivity’ is about as oxymoronic as things get. We’ll get another reminder of this when Q2 labour productivity readings arrive this morning in the wake of last Friday’s GDP figures (8:30amET). Hint: not good. In the past five years, productivity has only been on the plus side in six quarters out of 21 quarters and soon to be six in 22 (chart 3).

And lastly, Canadian PM Carney's two-day cabinet retreat starts today but don't look for much if anything by way of headlines with media barred this time (here). JF is among the presenters. It's all on the path to a Fall budget and a major projects list before then—along with whatever tariff and trade assumptions one wishes to make with the mess that the Trump administration has created. My macro view remains on the more optimistic side while warning of ongoing inflation risk and caution against expecting easier monetary policy.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.