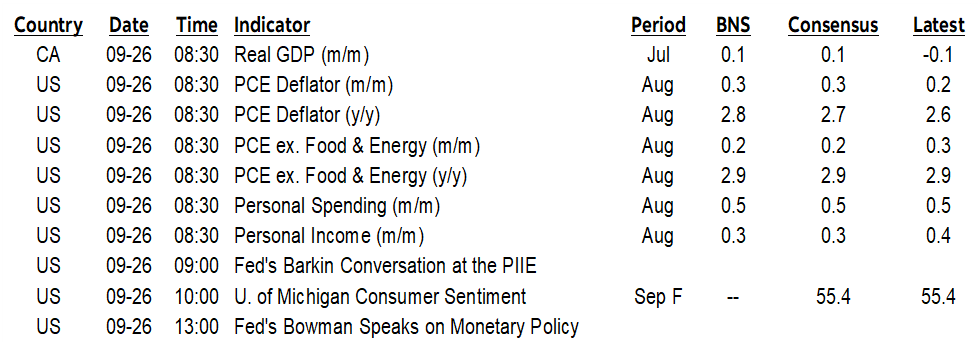

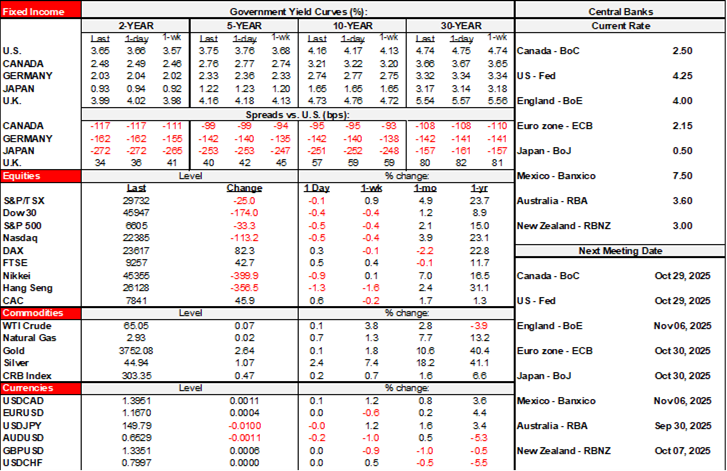

ON DECK FOR FRIDAY, SEPTEMBER 26

KEY POINTS:

- Global markets are shaking off Trump’s latest tariff tantrum

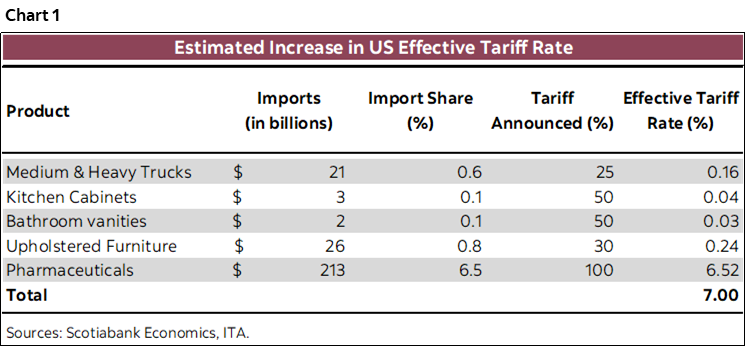

- The latest sector-specific tariffs will likely be a rounding error on the overall tariff rate

- US core PCE update on tap, but Powell already says to ignore it and many more!

- Canada’s economy is probably barely growing in Q3

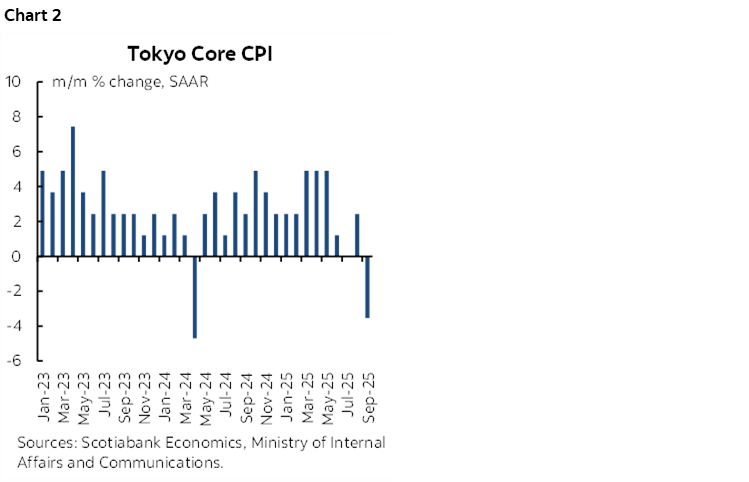

- Why JGBs and the yen ignored Tokyo core CPI’s m/m plunge

Global markets are mostly holding it together this morning in the wake of another round of misguided anti-business and anti-consumer tariffs from President Trump coupled with a disturbing escalation of his vengeful retribution against political opponents. Frankly, Trump should send Comey a thank you note for handing him the 2016 election by launching his investigation of Hillary’s emails days before the vote.

US Ts, EGBs, gilts and JGBs are trading within tiny shades of differences from one another. US equity futures are roughly flat and slightly underperforming European cash markets. FX markets are mixed.

TRUMP’S LATEST TARIFF ASSAULT

How ridiculous are Trump’s tariffs? Think bathroom vanities, the latest great threat to America’s national security that will be subject to a 50% tariff starting next Wednesday as announced last evening. Kitchen cabinets too; same rate, same time. Upholstered furniture will be tariffed at a 30% rate at the same time. Those dang coin-swallowing foldaway beds are a menace to America! This is purely farcical. I would think that the Supreme Court should have all the evidence it needs to conclude that Trump is totally abusing the IEEA provisions with Trump not helping his case with these latest actions.

Heavy trucks will be hit by a 25% tariff. What’s unclear is whether it’s just heavy as per Trump’s post, or also medium-trucks which the Commerce Department’s investigation was focused upon. If it’s heavy and medium then Mexico and Canada get slammed, but we need details.

The 100% tariff on branded, patented pharmaceuticals sounds devastating, except for the fact that companies with construction and production in the US market will be exempt. Sector analysts seem to be of the view that this would whittle the effect tariff imposed on pharmaceuticals down to much lower and possibly negligible rates.

We don’t have details on the tariffs which is one important caveat. All we have are Trump’s bombastic social media posts.

The shares of US imports for the combined categories is low at just over 1% and across both consumer and business products. The very high tariff rates applied to the import shares could result in a meaningful flow through to inflation before then considering substitution effects and the usual other debates that can influence pass through in the short-term versus long-term. Chart 1 shows what the pure math would look like if we took the tariffs literally before considering the above arguments. In reality, the pharma exemption and the small shares of total imports of the other categories would probably mean a nearly negligible impact on the overall weighted average effective tariff rate on imports coming into the US. Then consider substitution effects and crimped spending to further whittle down the effects.

Needless to say that Trump is harming American businesses and consumers who will face less choice, less competition and higher prices as a consequence to all of his tariffs. Over time, not even the protected companies will benefit as they’re likely to get lazy, invest less, innovate less, be less mindful toward containing costs, and hence less competitive internationally. Tariffs, directed investment, policies that damage growth in the labour pool, publicly admonishing businesses, and attacking institutions are not right-of-center business-friendly policies in my books, whatsoever the delusional thoughts of others may be.

WHY SOFT TOKYO CORE INFLATION WAS IGNORED

Tokyo core CPI excluding both food and energy registered its weakest reading since April 2024 at -3.5% m/m SAAR (chart 2). Shorter-dated JGBs barely flinched and the yen is little changed. Why? Partly because of a distortion as the Tokyo government changed daycare eligibility in a way that local analysts estimate knocked 0.3% m/m off CPI in non-annualized terms. It’s also partly because the Tokyo and national inflation figures have been uncoupled of late; national core CPI has been trending much warmer in month-over-month terms. The national gauge arrives on October 23rd—one week before the BoJ. Ergo, I’d advise waiting for the national reading to firm up expectations as markets remain on the fence between a BoJ hike and a hold on October 30th.

CANADA’S ECONOMY IS PROBABLY BARELY GROWING IN Q3

We get the revised estimate to the initial flash reading of 0.1% m/m SA GDP growth in July along with details, plus the preliminary estimate for August sans details (8:30amET). The combination will improve our tracking of Q3 GDP growth that is looking like it’s well under 1% q/q SAAR (chart 3).

US CORE PCE PLAYS SECOND FIDDLE TO JOBS

We get another update on US core PCE inflation this morning for the month of August (8:30amET). I’m on the fence on this one. My estimate leans toward 0.2% which is what I marked down. 0.24% is to the second decimal point. That reflects a) core CPI, b) weighting differences between core CPI and core PCE, c) weighted contributions from pertinent PPI components. Those are not the only differences between CPI and PCE, however, such that because the estimate is so close to the midpoint it wouldn’t take much to bump it toward 0.2 or 0.3.

But who cares, Powell says it’s all transitory, so here we go again. He says that policy is not on a pre-set course which is fine, except for the fact that he has pre-set a dismissive stance toward any upside in inflation as supply chain effects including but not limited to tariffs rattle through. That’s a mistake as inflation risk remains elevated in long-wave fashion beyond the street’s typically myopic focus.

Powell also says it’s about taking out insurance against a further erosion of the labour market. If that’s the aim, then they need to act in meaningful fashion; a handful of cuts won’t restore greater job market momentum.

The US releases will also include what are expected to be a solid gain in consumer spending that outpaces a modest gain in incomes such that the personal saving rate of 4.4% may dip.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.