ON DECK FOR THURSDAY, SEPTEMBER 25

KEY POINTS:

- Mild risk-off sentiment across equities faces higher US data risk

- US GDP, PCE revisions to stretch back five years in time…

- …as multiple sources of new information are incorporated

- Can US core durable goods orders keep up the momentum?

- Banxico to cut today

- Why it’s wrong for American taxpayers to be bailing out Argentina

- SNB held, open to returning to negative rates

- Canadian payrolls: lagging, incomplete and wickedly revised

- Fed-speak to drone on

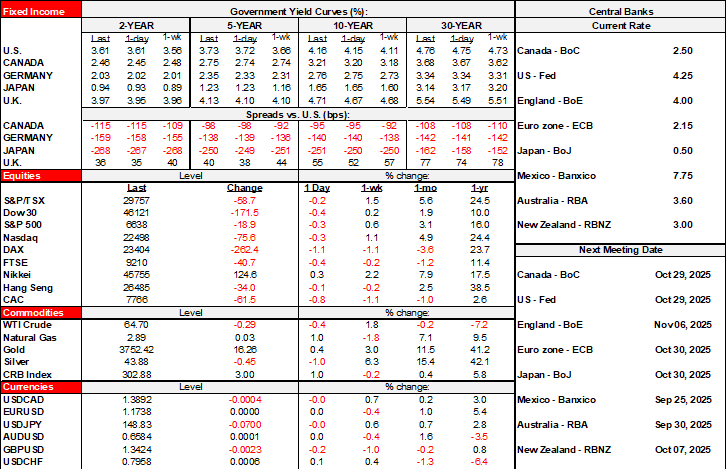

Mild risk off sentiment in stocks is accompanied by relative stability in sovereign bonds and FX markets. A significant amount of US data is on tap after SNB’s decision and ahead of Banxico.

SNB HELD, OPEN TO GOING NEGATIVE

The Swiss National Bank held its policy rate at 0% as widely anticipated. President Schlegel said that while they’re well aware of the costs to going negative, “if it’s really necessary to fulfill our mandate we are ready to use all the tools that are available—also negative interest rates.” OIS markets have a minor 10–15% chance at going negative priced over coming meetings.

BANXICO EXPECTED TO CUT

Another 25bps cut is widely expected this afternoon in a follow-the-Fed sense but reinforced by domestic considerations and tariff uncertainty. Chart 1 compares our forecast to the consensus.

Guidance provided at the August 21st meeting that accompanied a 25bps rate cut shifted more to the affirmative in replacing wording that policy was merely being ‘calibrated’ to now how it was “deemed appropriate to continue the rate-cutting cycle.”

Another reason for the cut is that while it doesn’t always follow the Fed, Banxico frequently does so and the FOMC just restarted what we think will be a material easing campaign. US tariffs and uncertainty around USMCA negotiations add to motivations to ease. Recent data has been mixed as jobs and wages hold up quite firmly, but industrial output has fallen over the past couple of months. The peso has appreciated from about 20.8 to the dollar in April to 18.4 now. Such forces will nevertheless be accompanied by a weary eye turned toward core CPI inflation that has risen back to about 4¼% y/y over recent months.

US DATA RISK INTENSIFIES TODAY AND TOMORROW

A fair amount of US data starts to roll this morning and into tomorrow when PCE inflation gets updated.

Revisions are back. This time it’s not just the Q3 estimate of 3.3% growth that incorporates fuller services data from the Census Bureau’s quarterly survey; most of us expect no material revision but some expect a tick or two upward revision (8:30amET).

More important may be annual GDP revisions back to 2020 including how the effects of the annual benchmarking revisions for payrolls will be incorporated (8:30amET). Multiple new sources of information are incorporated and explained here. Last year’s annual revisions are summarized here in a BEA briefing to give some context; a similar set of communications is expected today. In that previous annual exercise, GDP levels were revised up and so was growth for most of the five years (chart 2). How the downward revisions to payrolls from April 2024 to March 2025 may impact GDP for that year is unclear a) because the effects could involve competing trade-offs, and b) because it’s just one set of data being incorporated in the revisions, and c) five years of GDP will be revised which could impact the 2023 jumping off point into 2024 and hence the 2024 growth estimates themselves.

Durable goods orders are expected to be soft based on airplane orders but key will be core orders (ex-defence and air) that could find the prior month’s surge of 1.1% m/m to be a tough act to follow (8:30amET).

Weekly initial and continuing claims and the advance goods trade figures for August are also due at the same time (8:30amET).

A heavy line-up of Fed-speak is also on tap today.

IGNORE CANADIAN PAYROLLS

As for Canadian payrolls, I never pay much attention to them (8:30amET). They’re lagging, with today’s release for July but with September’s LFS jobs due in a couple of weeks. The US releases both job market measures on the same day and why Canada has to scatter them two months apart is unclear. SEPH payrolls are subject to frequently very high revision risk in the tens of thousands of jobs each month (charts 3, 4). They track a subset of the labour market in a country where off-payroll employment is big and only captured in the LFS measure.

WHY ARE AMERICAN TAXPAYERS BAILING OUT ARGENTINA?

Yesterday’s US policy supports to Argentina settle nothing about the risks facing President Milei’s administration while raising serious questions over what the US is doing and getting itself into.

Treasury Secretary Bessent’s social media post (here) outlined the intentions. Pledging to directly buy Argentina’s bonds through the Exchange Stabilization Fund’s roughly $30B or so of liquid funds is precedent setting; the US has supported LatAm debt markets in the past such as through Brady bonds and other supporting measures, but never by using taxpayer money to directly buy another country’s bonds in the secondary and primary markets. A US$20B swap line with Argentina’s central bank is also among the measures.

The way I see it, all Bessent is accomplishing is to provide holders of Argentina’s debt a way out—for those that haven’t already exited—ahead of high uncertainties surrounding the October 26th midterm elections in Argentina and the high uncertainties that surround Milei’s reforms. Milei needs major advances to call it a success and thwart veto efforts against his reforms by the opposition that has been climbing in the polls including in the local elections earlier this month.

In a more general sense, the US moves continue the pattern of overtly interfering in another nation’s political affairs. Witness Brazil. Witness Canada. Cue the line-up of other countries seeking direct bail outs by US taxpayers. What will the US do if Milei’s reforms fail and/or he suffers political defeat later in October? Will Bessent double down on bond purchases or bail and leave US taxpayers with losses and perhaps no way out? The prime motivation for the US actions seems to be nothing more than supporting a political supporter who says kind things about President Trump. Further, the US cannot cry foul when other countries interfere with its elections.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.