ON DECK FOR TUESDAY, SEPTEMBER 23

KEY POINTS:

- Global markets paying little heed to PMIs with Japan out

- Global PMIs signal slowing economies everywhere except Germany

- Miran’s embarrassing amateur hour

- Fed’s Powell to speak on the outlook

- BoC’s Macklem to speak on trade. Again.

- Sweden’s Riksbank gives with one hand, takes with the other

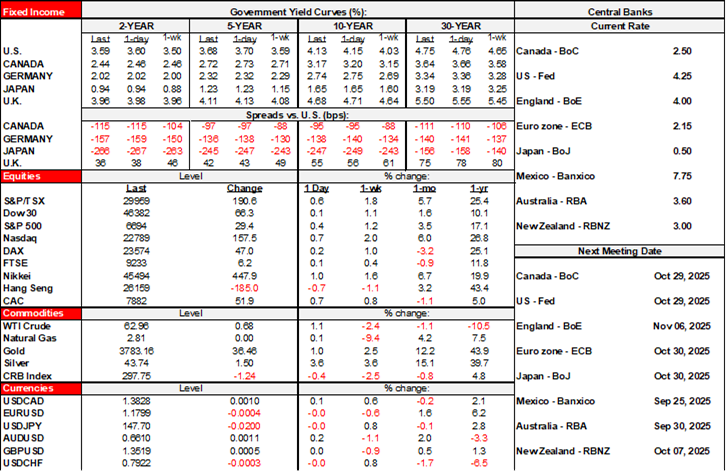

Global markets are generally paying little heed to softer PMIs that are signalling a deterioration in global growth. There is a slight bid to US Ts and gilts but little change across EGBs. Currencies are mixed with the post-Riksbank krona outperforming. Equities are mixed with US futures flat but most other European benchmarks a touch higher and with Tokyo out for a holiday. Central bank speak will also factor into markets with Powell and Macklem on tap after Miran’s hack talk yesterday.

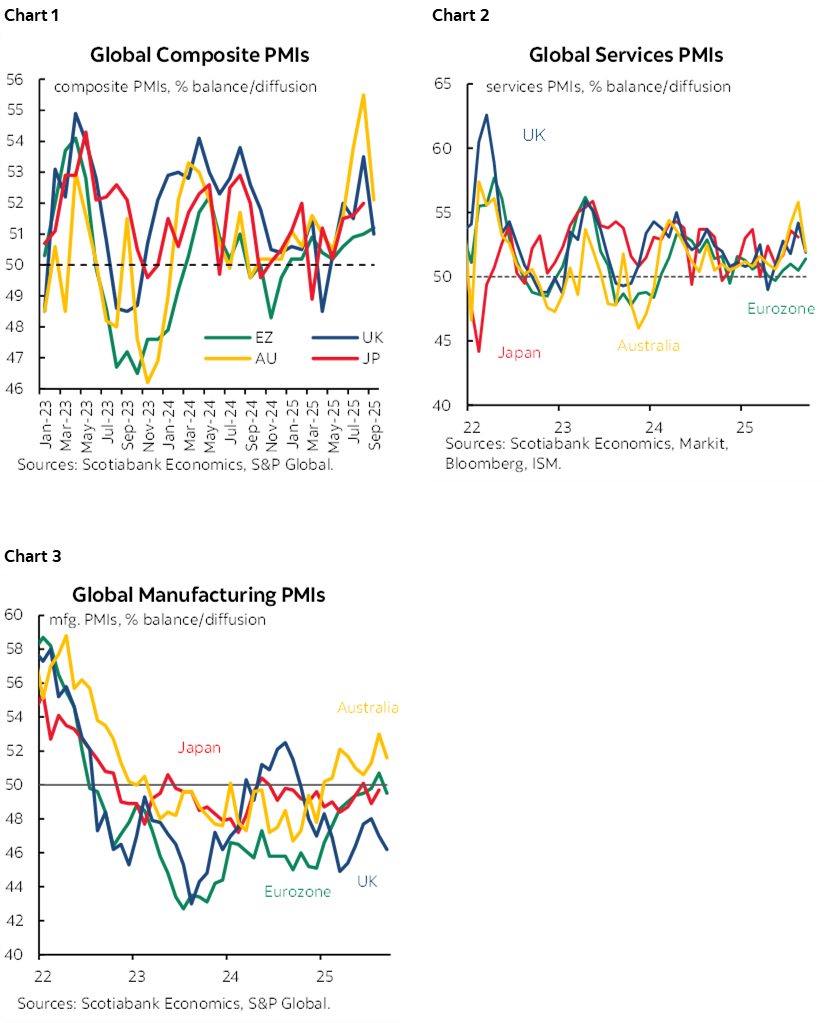

GLOBAL PMIS SLOW EVERYWHERE EXCEPT FOR GERMANY

With the US and Japan pending, here’s the rundown of the latest purchasing managers’ readings. Global growth is clearly being damaged as earlier fits and starts on tariffs give way to more binding effects that are just beginning. See charts 1–3.

- The Eurozone composite PMI was roughly unchanged (51.2, 51.0 prior), a mere 0.2 up-tick which for soft data is well within the noise bands. A slight acceleration in services (51.4, 50.5 prior) was offset by manufacturing’s dip into sub-50 contraction (49.5, 50.7 prior).

- Within the Eurozone we only get the German and French PMIs now and the rest later. Germany’s acceleration offset France’s deceleration. Germany’s composite PMI was up 1.9 points to 52.4 as services accelerated (52.5, 49.3 prior) but manufacturing slipped into contraction (48.5, 49.8 prior). France’s composite PMI pushed further into sub-50 contraction (48.4, 49.8 prior) because both services and manufacturing are in contraction as tariffs and fiscal woes hit confidence.

- The UK economy slowed in September as the composite PMI fell by 2.5 points to 51.0 because manufacturing remains in contraction (46.2, 47.0 prior) but services slowed (51.9, 54.2 prior).

- India’s composite PMI fell by 1.3 points to 61.9 as both manufacturing (58.5, 59.3 prior) and services (61.6, 62.9 prior) slowed.

- Australia’s economy slowed with the composite PMI falling by 3.4 points to 52.1 and still in mild expansionary territory. Services cooled (52.0, 55.8 prior) and manufacturing also eased off (51.6, 53.0 prior).

- The US updates its PMIs later this morning (9:45amET) and Japan will do so this evening.

BOC’S MACKLEM TO SPEAK ON TRADE—AGAIN

Bank of Canada Governor Macklem speaks today on ‘global trade and capital flows.’ The speech embargo lifts at 2:15pmET and there will be a press conference at around 3:45pmET following speech delivery and audience Q&A. Major new points are unlikely to be shared in relation to what was shared this past week and other speeches. Trade is front and center in terms of BoC concerns for readily apparent reasons, hence why he has delivered so many speeches on it over about the past year.

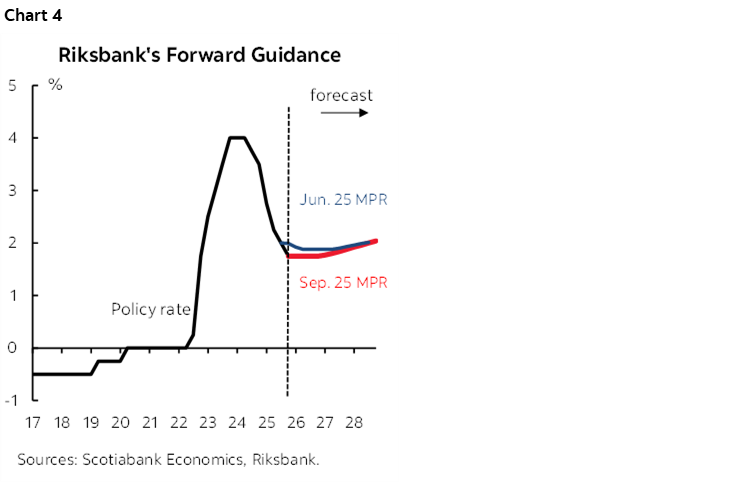

RIKSBANK LIGHTS UP THE KRONA

The Riksbank’s hawkish cut lit up the krona overnight. The central bank surprised some in consensus by cutting its policy rate by 25bps but took it back on the bias. Thirteen out of 22 expected a hold and the rest a 25bps cut. The bias explicitly stated there were no further planned cuts over the entire policy horizon into 2028 (chart 4). We’ll see about that, but for now, the clear signal is not to expect anything from the central bank barring an exceptional shock. The krona is the best performing cross to the USD among the majors and semis this morning. Sweden’s rates curve is marginally underperforming other benchmarks in a mild bear steepener.

MIRAN’S UNSERIOUS SPEECH TO GIVE WAY TO POWELL

On that note, we’ll get other Fed-speak today after Governor Miran’s unserious exercise in cherry-picking what’s changed and what hasn’t and the views around the effects in his speech yesterday.

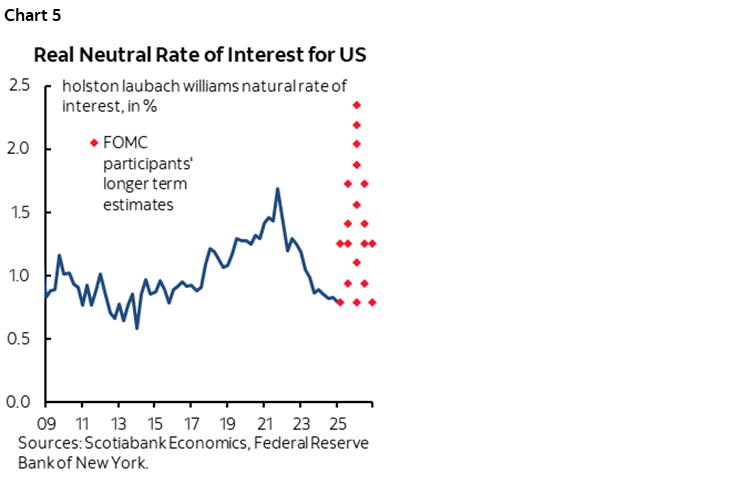

Miran not only did a full about face on his prior argument in March 2024 that the neutral rate had pushed higher—not lower—but also confused neutral rates with nearer term policy considerations which violates anyone’s understanding of monetary policy 101. Neutral is a vague, long-run concept that describes an economy in perfect equilibrium absent any shocks. Nobody really ever knows what it is; chart 5 shows the scattered opinions of the FOMC members about the real neutral rate. The conditions under which neutral holds as a concept clearly do not described the US today, and so current monetary policy has to be conducted in line with current and nearer term expectations over how the dual mandate will evolve. Think of neutral as akin to a sailor’s north star; it’ll generally help, unless clouds and stormy weather blot it out for a long time and you could bust up on a pile of rocks if that’s all you’re going by. This is amateur hour. There is absolutely nothing about the neutral rate concept that says you must be there now, or by December, versus where you **might** be ages from now in a more stable world that doesn’t seem to be coming any time soon! Miran also naturally made no mention of moral hazard—as any Fed official wouldn’t—but that doesn’t mean we shouldn’t. Rapid easing would either embolden the Trump administration to pursue more unwise policies that would cause further damage to the US and global economies, and/or lose market confidence.

Anyway, outside of the maga base, Miran’s -150bps dot this year is to be ignored as the government’s view, so moving on.

Back to reality, key will be Chair Powell’s speech on the economic outlook early this afternoon (12:35pmET).

Governor Bowman (9amET) and regional Presidents Goolsbee (8:30amET) and Bostic (10amET) also speak.

The US also updates the Richmond Fed’s manufacturing gauge (10amET) as one other source of input into expectations for the next ISM-manufacturing reading. Other readings have been mixed including a sharp drop in the Empire gauge but a sharp gain in the Philly Fed’s measure. All such US data is stale on arrival in my view as frontloading of production faces severe worker shortages and lagging tariff effects.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.