ON DECK FOR TUESDAY, SEPTEMBER 2

KEY POINTS:

- Risk-off sentiment as September volatility arrives

- How the late Friday tariff ruling could be impacting stocks and bonds

- Eurozone CPI surprises a touch higher

- SK, Peruvian inflation surprise lower

- US ISM-manufacturing on tap

- Global Week Ahead—Will Nonfarm Support Powell’s Pivot? (reminder here)

Markets are wasting no time reminding us that September can be a rough month for risk appetite. Stocks are broadly lower with US futures down ¾% to 1%, TSX futures slightly lower, and European cash markets mostly lower by over 1% in Germany. Sovereign bond yields are broadly higher and led by the US longer-end. The dollar is broadly stronger.

THE TARIFF RULING’S COMPLICATED AFTERMATH

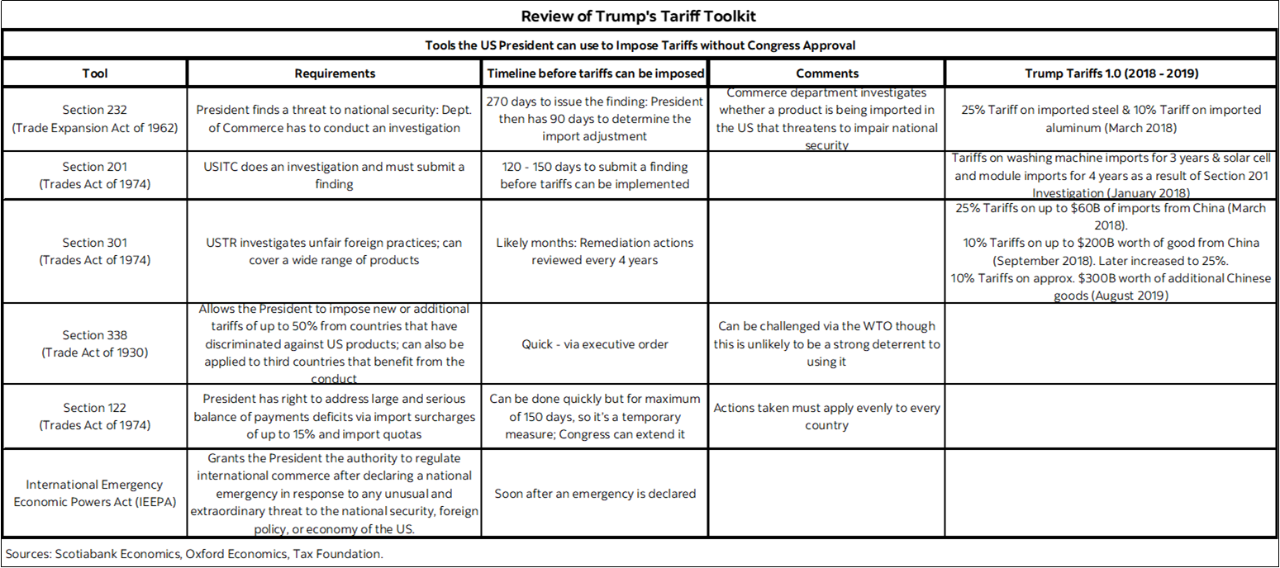

There are few fresh catalysts. Some of this may be spillover from the late-Friday US court ruling against the April 2nd ‘Liberation Day’ reciprocal and fentanyl tariffs. Uncertainty surrounding next steps increased by contrast to those who argued that even though tariffs are foolish, set rates gave something to plan around. The Supreme Court will likely have to weigh in at some point over coming months. The federal court ruled against them but kept them in place and pushed the issue back to a lower court. One uncertainty is whether striking them down only applies to the parties in the lawsuit or more broadly. Trump could shift tools and tactics; only IEEPA tariffs were struck down in the suite of options shown in the table on the next page. The absence of tariff revenues is a plus for the US and world economies but could end the diversion of revenues from American businesses and consumers to government; hence higher yields.

Apprehension ahead of the week’s US data particularly Friday’s nonfarm payrolls may be another consideration. Who knows, maybe the anti-democracy gathering of Putin, Xi Jinping and Modi over the weekend isn’t helping the mood either.

MIXED INFLATION READINGS

Overnight releases were very light.

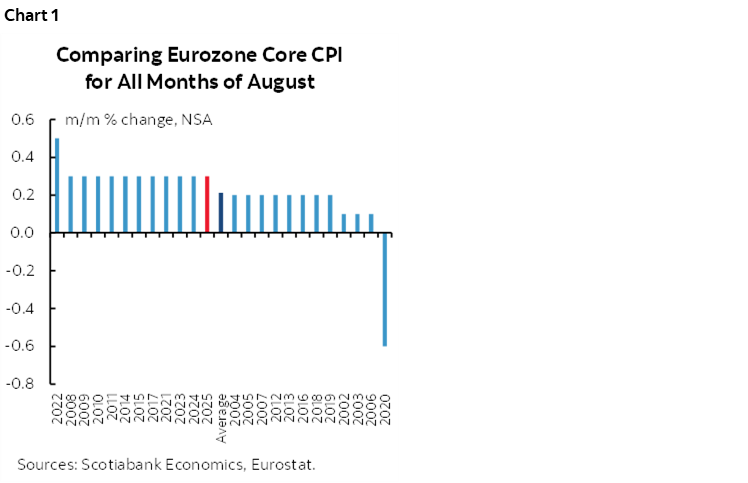

- Eurozone CPI landed at 0.2% m/m (0.1% consensus) and core inflation held at 2.3% y/y (2.2% consensus). Core m/m was among the stronger historical readings (chart 1). Most of the information was digested as individual countries released late last week.

- South Korean CPI was softer than expected (-0.1% m/m NSA, +0.2% consensus). Core inflation fell to 1.3% y/y (1.7% consensus, 2.0% prior).

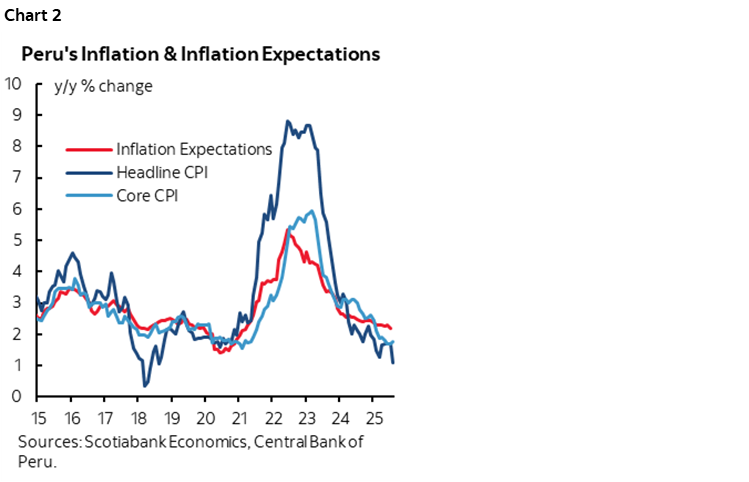

- Peru’s inflation also landed softer than expected (-0.3% m/m NSA, +0.2% consensus) as the y/y rate fell to 1.1% (1.7% prior) for its softest reading since 2018. Chart 2.

US MANUFACTURING SECTOR IN FOCUS

The main focus into the N.A. session will be US data and namely the ISM-manufacturing reading and is forecast to improve a touch (10amET). Watch supply chain measures, price pressures and industry anecdotes, but Thursday’s ISM-services matters much more to the broad economy. Construction spending in July is also due out (10amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.