ON DECK FOR THURSDAY, SEPTEMBER 18

KEY POINTS:

- FOMC’s dovish cut continues to reverberate through global markets

- BoE cuts QT plans roughly as expected, and holds Bank Rate

- Was the spike in US initial jobless claims temporary?

- Norges delivers a hawkish cut

- BCB and CBCT held, SARB might also hold

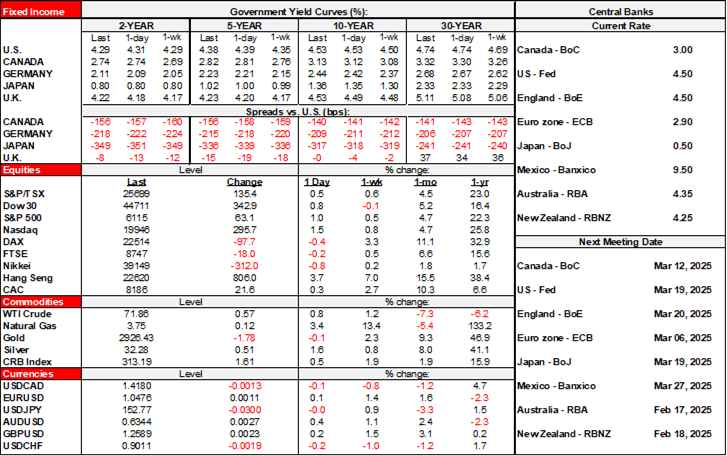

There is modest follow through on the FOMC's dovish cut as US Ts richen somewhat further this morning. Stocks are getting a lift globally with benchmarks up by +/-1%. More central banks and US labour market data are focal points today. Recaps of yesterday’s FOMC and BoC decisions are available here and here. The Canada curve is also slightly richer this morning with markets one the fence for the October 29th BoC decision and mostly priced for a cut by December.

ANTIPODEAN RATES RALLY

Antipodean rates rallied overnight on a combination of factors.

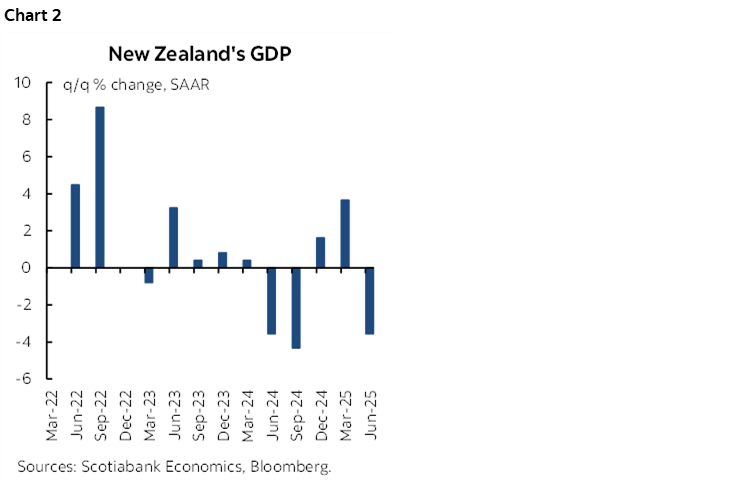

It started with NZ GDP that sharply undershot consensus. The economy shrank by -0.9% q/q versus consensus and the RBNZ's estimate at -0.3% and with only a minor upward revision to the prior quarter (chart 2). The kiwi curve bull steepened with the 2-year yield down about 12bps.

Then Australian jobs hit. Against consensus expectations for a gain of 21k, they fell by a modest -5.4k as full time jobs plunged by 41k and part time rose 36k. The job market’s momentum has softened over recent months (chart 1). That contributed to about a 3bps rally across the Aussie rates curve.

Then a revised RBA estimate of the neutral rate pushed lower to 2.9% from 3.6% previously. That doesn't necessarily speak to near-term monetary policy considerations but implies policy may be a bit more restrictive than previously thought relative to a longer-term guidepost.

BANK OF ENGLAND REDUCES QT PLANS

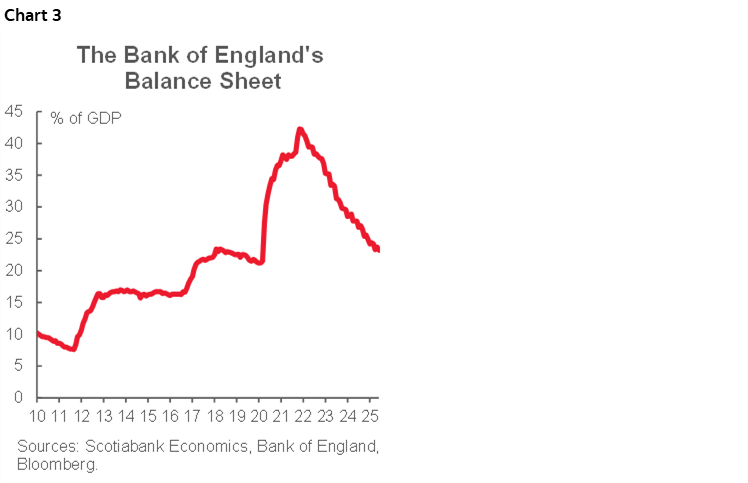

The Bank of England preserved its cut-hold-cut pattern by holding Bank Rate unchanged 4% as priced and widely expected. Quantitative tightening plans were revised roughly in the ballpark of expectations; see the market notice here. The BoE now says they plan to reduce gilts holdings by about £70 billion over the year from next month to next September. That’s a slower pace of QT than the past year’s £100B roll off. Out of 66 responses to a recent BoE market participants survey, most expected the annual reduction of gilt holdings to be between about £60–75 billion. The BoE basically walked roughly down the middle. The BoE’s balance sheet has sharply retrenched from a peak equal to 42.3% of NGDP in November 2021 to about 23% now (chart 3). The forward bias was taken by markets to reinforce pricing for no further rate change this year and 1–2 cuts next year.

NORGES BANK DELIVERS A HAWKISH CUT

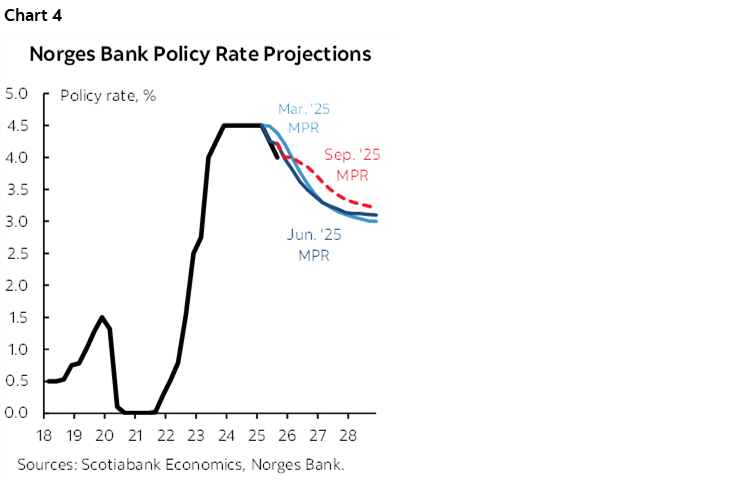

Norges Bank cut its deposit rate by 25bps to 4% as many but not all had expected. The hawkish cut pushed yields a little higher across the curve. The uncertainty into the decision had to do with vague guidance toward another cut before year-end which may or may not have been at this meeting. Explicit forward guidance raised the rate profile going forward compared to previously and now guides the rate to decline to just above 3% by 2028 (chart 4). Norges considered pause at this meeting, said a restrictive stance is warranted, and flagged a better performing economy than expected.

BCB AND CBCT HELD, SARB COMING UP

Brazil's central bank held at 15% as widely expected last evening because they guided going in that they would be on a prolonged hold after a sharp tightening campaign.

SARB is expected to hold at 7% this morning (9amET). A sizeable minority thinks they may cut.

Taiwan’s central bank also held as widely expected with the discount rate left at 2%.

DATA RISK

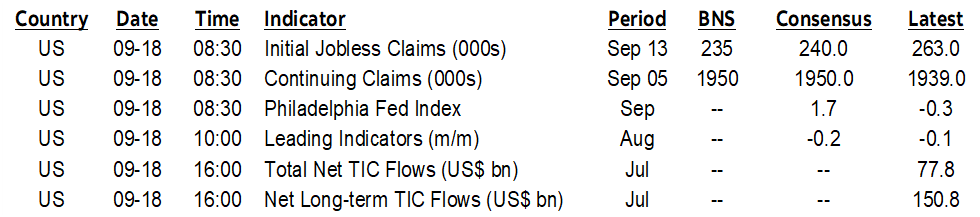

Was the spike in US initial jobless claims two weeks ago to 263k the start of a new trend higher or a flash in the pan? We’ll find out shortly (8:30amET). Some states were estimated that week. DOGE packages for federal government employees are also maturing this month. Another spike would likely reinforce the FOMC's dovish cut but it would remain unclear whether the rise will last. The US also updates the volatile Philly Fed gauge this morning (8:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.