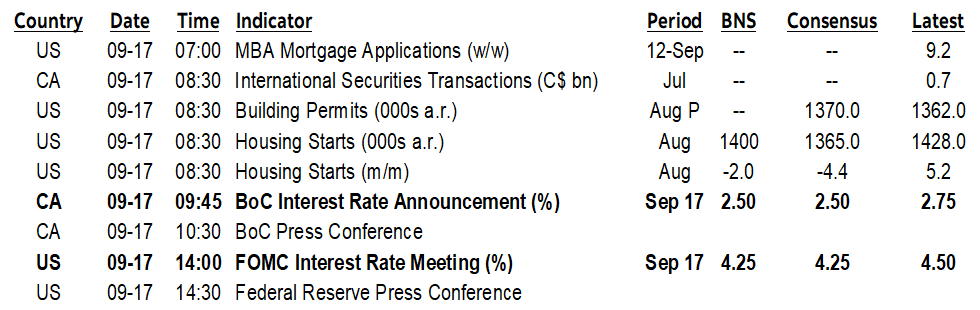

ON DECK FOR WEDNESDAY, SEPTEMBER 17

KEY POINTS:

- Global asset classes hanging tight before the Fed

- Fed to cut 25; a hold or upsized surprise would be out of character for Powell

- FOMC’s dots likely to pull forward easing, add to 2026, leave neutral unchanged…

- ...but fade them as stale and weak guides amid dissenters and political risk

- Why the Fed won’t be too concerned about funding market pressures just yet

- BoC to cut 25bps, offer cagey forward guidance

- Did Carney delay the Federal Budget to influence the BoC’s October meeting?

- UK core CPI was softer than usual, but won’t influence the BoE tomorrow

- Brazil’s central bank won’t do anything after the Fed

- Bank Indonesia surprised—again!

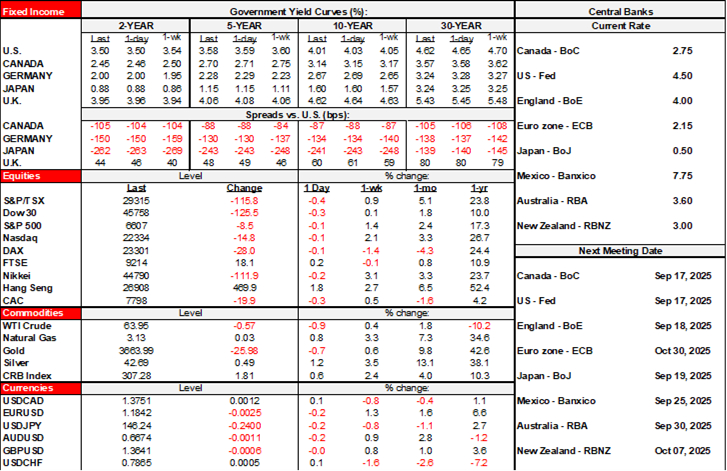

Broad asset classes are generally little changed so far this morning as they await the Federal Reserve and Bank of Canada decisions. Overnight developments included soft UK core CPI, and another Bank Indonesia surprise cut amid political turmoil. Brazil’s central bank is also on tap after the Fed.

See my week ahead for full previews of the Fed and Bank of Canada meetings (here).

BANK OF CANADA TO CUT, GUIDANCE TO BE CONSERVATIVE

The BoC should be a slam dunk. A 25bps cut is expected and fully priced. It will be a statement-only affair (9:45amET) sans MPR/forecasts and followed by the usual press conference (10:30amET). Macklem delivers a speech next week as well with the topic to be disclosed. It’s premature to expect much beyond jawboning on CORRA. See my week ahead article for the arguments for an overnight rate cut and for a hold to get a balanced take on the outlook. Also see the post-jobs note on 09/05 (here) when the call was changed partly reflecting jobs and several other new pieces of information. Yesterday’s CPI (recap here) wasn’t going to change anything going in and didn’t on the way out either for the five reasons I gave in yesterday morning’s daily note.

I don’t expect meaningful forward guidance; Macklem is typically loath to provide any and when he occasionally flirts with guidance, it’s often not helpful anyway. In any event, trade and fiscal policies remain up in the air. His predilection is to tell folks to do their jobs and to speak in riddles, but he’s a more polished communicator than Poloz who at times would give several competing views on the same day. I find -50bps cumulative is borderline meaningful to take out a bit of insurance on downside future risks to the inflation target with lagging effects but without overdoing it in potentially dangerous fashion and absent crisis conditions that would merit going down to a one-handled or lower rate.

Key may be how fiscal policy evolves. Why did PM Carney delay the Federal Budget until Tuesday November 4th and hence after the next two BoC decisions despite providing earlier guidance that it would be delivered in October? One possible theory is so that the BoC couldn’t factor in budget details in the October MPR and forecasts with the next chance to incorporate budget assumptions in forecasts not until the January MPR. Macklem might have been put in a tough place having to whiff at the October meeting after a cut today if a stimulative budget landed. That could backfire if Carney was thinking go ahead and cut twice and then we’ll heap on stimulus; maybe a skip is in order so that the Budget can be evaluated. #Headgames.

If the BoC holds with a very low probability, then the front-end reaction will be violent as I can’t see guidance containing the damage on a signal that they don’t have enough evidence to cut. I struggle to give that more than a 5% tail chance at this point. It’s meaningless that there is no MPR this time as the BoC has proven a willingness to move on non-MPR meetings and with a press conference available to explain things. It’s meaningless that there was no advance guidance ahead of time since the BoC doesn’t roll that way; it’s not a hand holding central bank.

FOMC: -25BPS, HOW MANY MORE, NOTHING ON FUNDING

The FOMC statement arrives at 2pmET along with the SEP projections including the dot plot. Chair Powell’s press conference will be held at 2:30pmET for up to 45 minutes to an hour.

The FOMC should be straight forward on a 25bps cut with only one forecaster out of 102 in consensus expecting an upsized 50 move and with 25 priced. Powell likes markets to be nicely set up on game day. If they were thinking of a whiff or upsizing a cut, then the typical playbook under his command would have probably found some way of signalling this. Developments since his Jackson Hole speech have only added to his spelled out case for commencing easing. The focus is on the dual mandate variables but it’s silly to ignore solid tracking of GDP growth has input into that given the implications for capacity considerations with the US economy still in excess demand in terms of output gaps and given the significant correlation between GDP growth and employment growth over time. This time around, the GDP and job growth correlations are messed up by AI and immigration policy shifts.

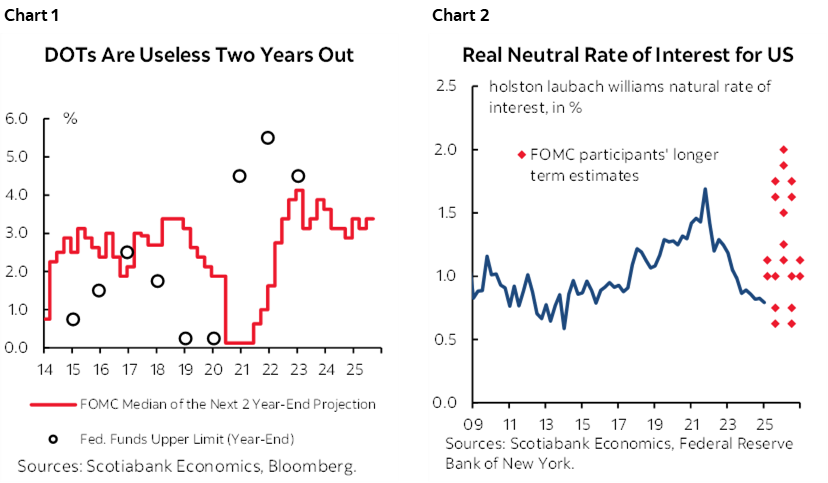

Key will be the dots at least for this year, while fading the dots in years 2 and beyond that typically don’t track very well (chart 1). The 7 on the Committee who thought there would be no cuts this year are likely to swing a lot with the key being whether they guide 50 this year or 75 as a median projection with tails in both directions. To repeat, for next year, the best advice I can give is to ignore what the dots show since they track poorly, but I’d be surprised if they went lower in 2026 than our 3.25% terminal rate for the upper bound. As for neutral, expect continued wide dispersion of views like we saw in June’s plot and probably at an unchanged nominal median of 3% with a 1% real neutral rate (chart 2). I think we’ll get a highly dispersed set of dots through all time frames which could lessen the significance of the median and in any event the risk of stacking the Fed’s Board and possibly the regional Presidents possibly makes the dots stale on arrival. We have six straight cuts down to 3.25% and stopping still reasonably around neutral.

Powell’s presser will be all about the full employment side of the mandate and transitory inflation; yes, that again. Time will tell.

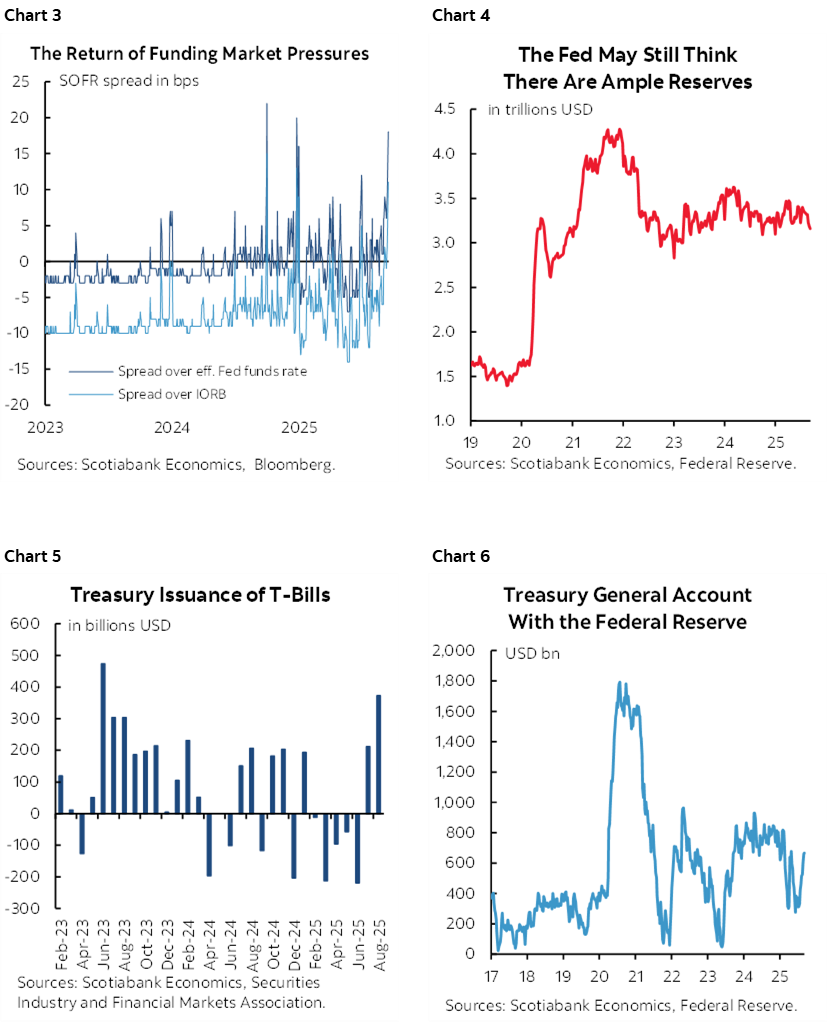

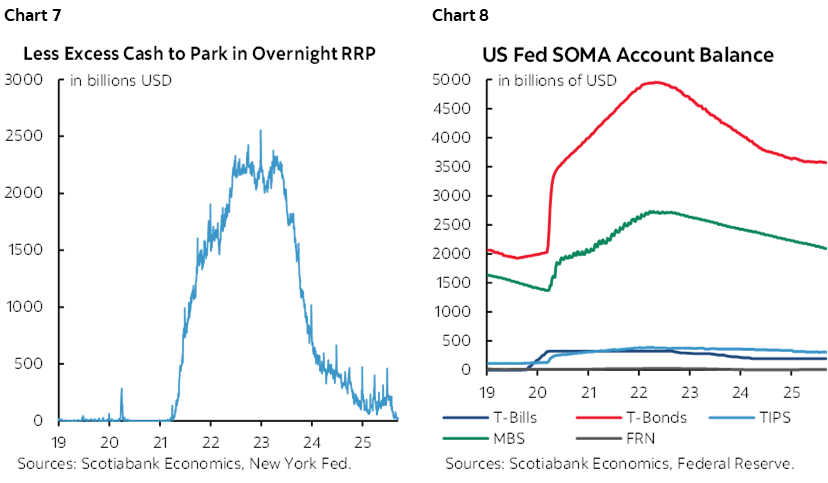

There will be jawboning about funding conditions but it’s unlikely that guidance around QT parameters or ample reserves will change as conditions are monitored over coming weeks into future funding pressures. The pressure is on the Fed to reassess conditions as SOFR spreads widen (chart 3). Key is whether about US$3.2 trillion in reserves in the banking system is still ample with some Fed officials estimating they remain about a half trillion above what may start to be considered as tight (chart 4). A surge of T-bill issuance (chart 5) is occurring to replenish the Treasury General Account used to fund the government after it was depleted during the latest debt ceiling fracas (chart 6). What that’s done is to deplete spare cash in the system such that there isn’t much being parked in overnight repo as one indication of tightened liquidity and pressure on spreads (chart 7). If this is temporary—until the TGA replenishment has stabilized—then perhaps the quantitative tightening that is driving the Fed’s SOMA holdings of Treasury securities and MBS lower (chart 8) need not be revisited before year-end. If the forces are judged to be more than just temporarily related to quarter-end funding pressures, tax season and TGS replenishment, then the Fed could move toward ending QT earlier than previously expected. The bottom line for today is that we don’t know the answer to this and so expect Powell’s press conference to emphasize that they are monitoring conditions but still view the system as having ample reserves for now.

In last week’s surveys for various media outlets I put down the risk of multiple dissenters in both directions; Waller and Miran and possibly Bowman if they don’t go bigger, maybe others who feel they shouldn’t ease. The likely statements by dissenters in the aftermath could extend the entertainment, especially Miran’s and especially if Trump says even he didn’t advocate for enough of a cut.

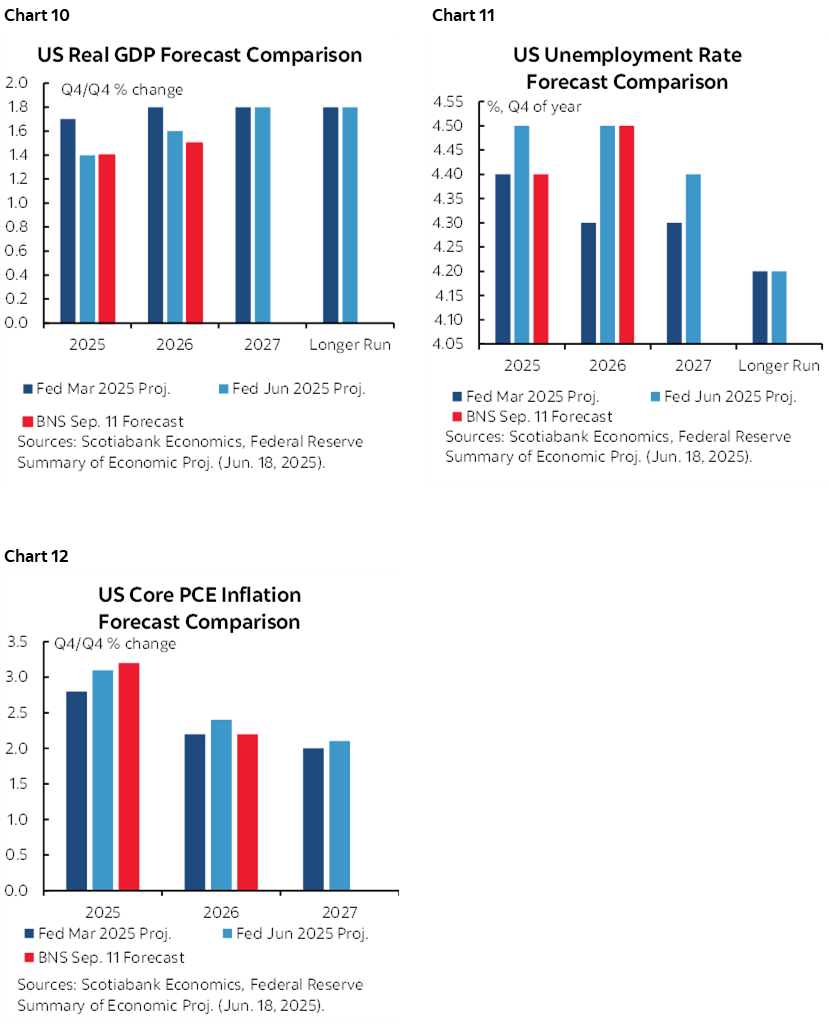

Also see the charts on the next page for how our current projections compare to the FOMC’s June SEP as an indication of where we think the risks lie in their forecast changes today.

OTHER DEVELOPMENTS—UK CPI, BI SURPRISE

Bank Indonesia surprised with a 25bps rate cut that only two out of 38 forecasters expected. It’s a volatile central bank that is prone to surprising. A dovish bias open to further easing is trading off domestic instability including political pressure on the government and protests against potential financial market instability through the effects on the rupiah.

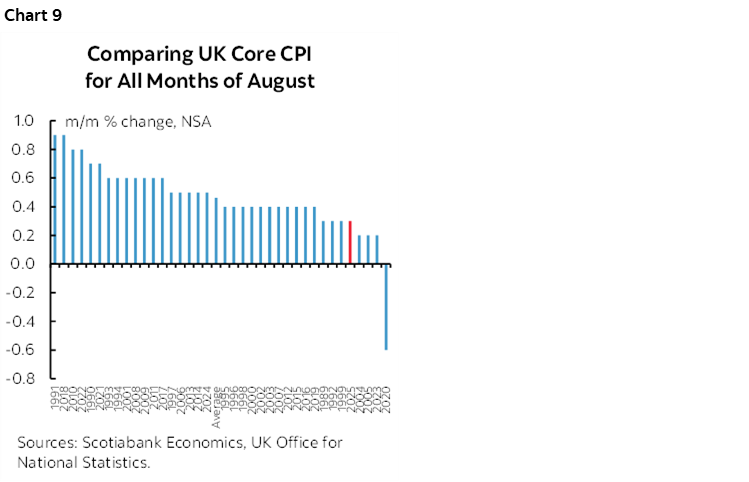

UK CPI was a bland affair. August’s reading of 0.3% m/m NSA matched headline expectations. Core CPI of 0.3% m/m NSA was among the lower readings on record for like months of August (since it’s not seasonally adjusted). Chart 9. Services inflation ebbed a touch more than expected to 4.7% y/y from 5%. Overall, the readings were taken slightly dovishly by the gilts front-end, but they will have no effect on tomorrow’s widely expected hold by the BoE.

Brazil’s central bank is widely expected to hold its Selic rate at 15% later today (5:30pmET) given guidance that a prolonged hold after a series of hikes lies in the cards.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.