ON DECK FOR TUESDAY, SEPTEMBER 16

KEY POINTS:

- Markets cautious into N.A. data, on eve of tomorrow’s central banks

- Canadian CPI: Five reasons why it shouldn’t matter to tomorrow’s BoC decision

- US retail sales are a tough act to follow July’s acceleration

- Senate confirms Stephen Miran as a weak addition to the Fed’s Board

- The case against Fed’s Cook is weak and getting weaker by the day

- Gilts mildly underperform after job market updates

- Canadian housing starts looking to extend summertime surge

Markets are going into Canadian and US data with a cautious bias and a careful eye toward more important developments in tomorrow’s central bank decisions. The dollar is softer. Gilts are mildly underperforming other global benchmarks. US equity futures are a touch higher while everyone else is a touch lower. There are four main considerations.

STEPHEN MIRAN CONFIRMED; COOK STICKING AROUND

One is last night’s final confirmation vote in the Senate for Stephen Miran’s nomination as Fed Governor just in time to crash the start of the two-day FOMC meeting today. He passed by a one-vote margin of 48–47 along party lines and because the GOP lacks the courage to confront Trump over a weak candidate who is a first in U.S. history as a direct appointment from a government role.

Miran will be joined by Governor Cook after an appeals court once again rejected the Trump administration’s case last evening as judges voted on party lines. The Supreme Court is next and who knows if they’ll get around to it before the October 29th FOMC decision or the next one after that on December 10th. Reuters has reported since Friday that she had properly disclosed her home as a vacation property and that local tax authorities reported no issues with her primary residence which would appear to negate the charges brought on by FHFA head Bill Pulte’s allegations. That would seem to lend credence to her counter lawsuits unless she’s convinced to take one for the FOMC team.

UK JOB MARKET UPDATES LARGELY SHAKEN OFF

Two is that UK job market readings drove mild underperformance of the gilts curve by largely just reinforcing market pricing for the BoE to do nothing on Thursday and for the two meetings after that one.

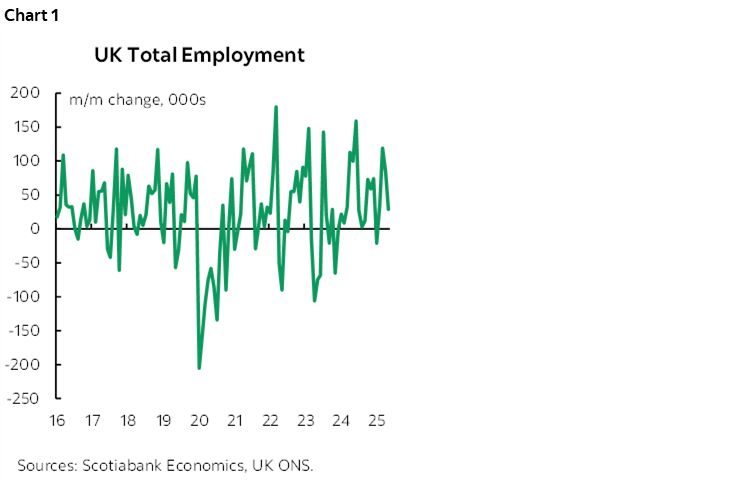

- UK total employment was up by 29k in July (chart 1). It lags payrolls but also includes off-payroll employers. That’s the fourth straight monthly rise.

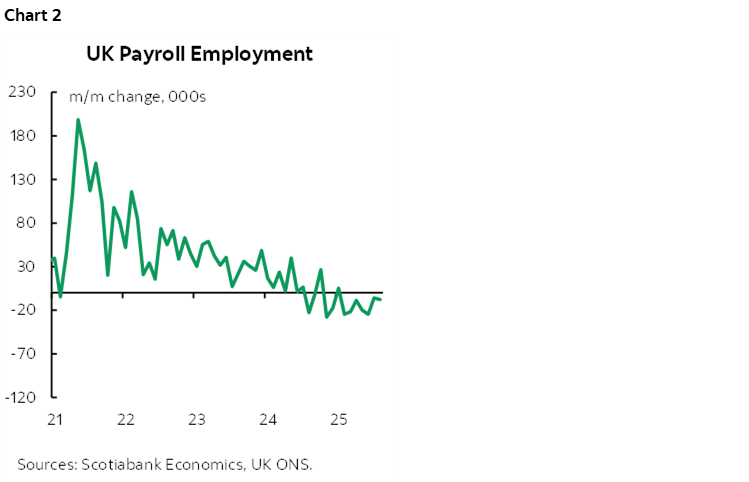

- UK payrolls fell by another 7.7k in August (chart 2). They have fallen for seven consecutive months and eleven of the past thirteen months.

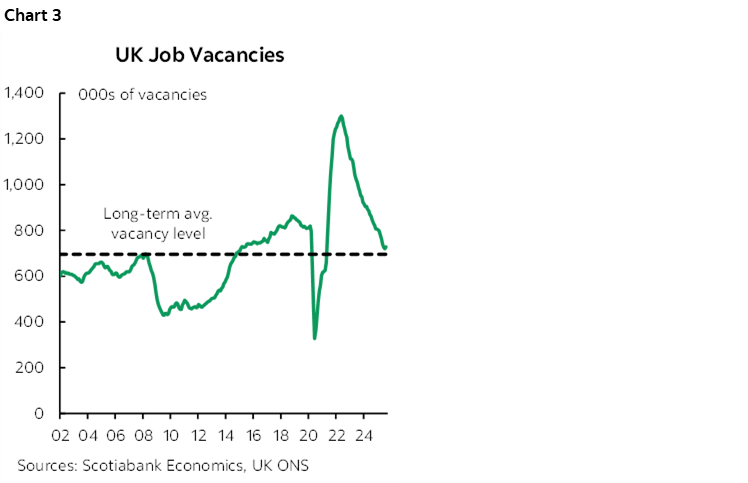

- UK job vacancies increased a touch in August and remain very slightly above the long-run average (chart 3).

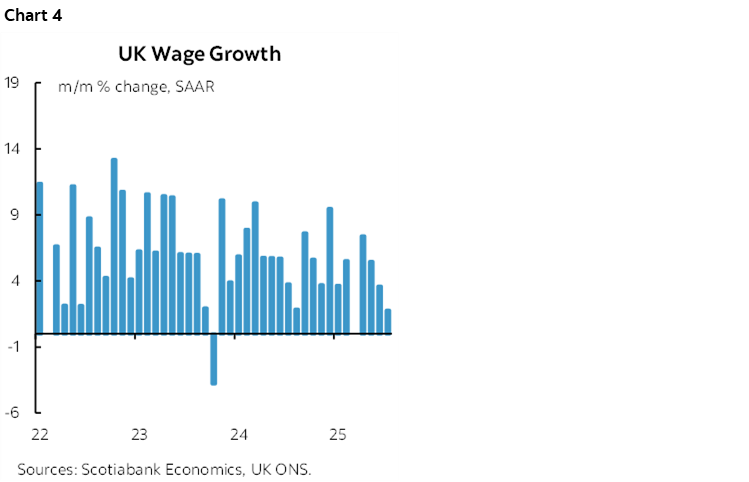

- wage growth cooled to 1.8% m/m SAAR in July. That’s the third monthly deceleration (chart 4).

US RETAIL SALES—REVISION RISK AND A TOUCH ACT THE FOLLOW

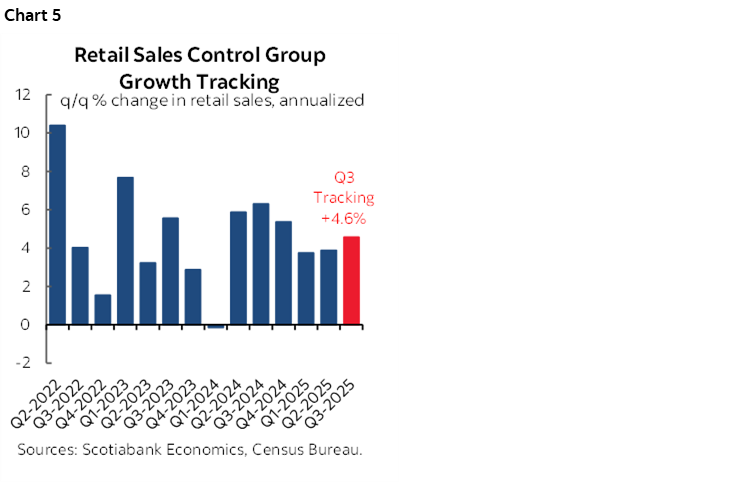

Three is that US retail sales are unlikely to repeat the prior month’s surge partly because we already know auto sales fell (8:30amET). Watch for revisions that are often substantial for this data. Key will be the control group that removes autos, food, gas, and building materials and is how the report gets incorporated into consumption estimates within GDP accounts. Q3 tracking is fairly robust going into the update (chart 5). Also bear in mind that the headline figures are nominal sales and need to be adjusted for inflation including tariff effects.

CANADIAN CPI—WHO CARES?

Fourth is Canadian CPI and it lands as the last bit of info before tomorrow’s morning’s BoC decision. The coincidental timing to US retail sales could mess up the market reactions somewhat.

See my week ahead for a preview that I won’t repeat (here). There is also a full BoC preview that lays out cases for a cut and for a hold and where I lean plus an argument for looking through CORRA’s overshoot that may be more temporary than structural.

Some shops have -0.1% m/m NSA for CPI, some are at 0% or 0.1% (Scotia) and one is at 0.2.

But does CPI matter to the BoC call ? That seems to me to be the most pertinent issue at hand. Some shops think it does. I think there is a very high bar for it to matter. In any case, it shouldn’t. Here’s why in the form of five reasons.

First, if anything matters, it’s the core gauges—not headline CPI. The BoC uses core gauges as the operational guide to achieving the headline CPI target over the medium term and generally dismisses short-term noise in the total CPI reading. I’ve seen stunningly flawed commentary from one person that since CPI is <2% y/y it’s an easy call to cut and almost as bad commentary from another that it’s m/m NSA headline they focus on.

Second, the way their meeting process unfolds by starting way in advance would make it unlikely that one report would make the difference to the dialogue they’ve already been having. They start the deliberations three weeks in advance of the decision. Staff briefings start the process. Staff recommendations are delivered one week before the publication of the decision. Governing Council meets over the rest of the week (ie: last week) and into early the following week (ie: this week). A consensus is struck and a press release is drafted. In other words, barring very unusual shocks, the decision-making process is very advanced by now.

Third, the BoC is likely to be primarily focused upon forward looking risks to their inflation target. Quite a while back they pivoted from concern about upside risks to inflation toward symmetrical risks (ie: equally concerned about new information that would put upside or downside risk to achieving 2% over the medium-term). They’re more balanced around a ‘current tariff’ July MPR scenario that thought inflation would fall back to 2.1% by the end of next year and 1.9 the year after. New information we’re getting recently may have them tilted toward greater concern about undershooting 2%, recent data be damned. That new information is highlighted in my weekly and previously.

Fourth, when it comes to recent data, the BoC looks at trends. Month-over-month trimmed mean and weighted median CPI have been in the mid-2s on a seasonally adjusted and annualized basis for the past three months. React to one report tomorrow? Please. Not unless Statcan massively plays with the SA factors on the prior readings (they don’t adjust the NSA prices data itself).

Fifth, PM Carney’s administration dropped retaliatory tariffs on September 1st. The BoC’s trimmed mean and weighted median CPI figures exclude direct effects of changes in indirect taxes like tariffs, but not the indirect effects if any. In other words, if there is any pass through from Canada’s retaliatory tariffs into Canadian prices then they could distort the core gauges. That would make the readings stale ahead of the following month’s data.

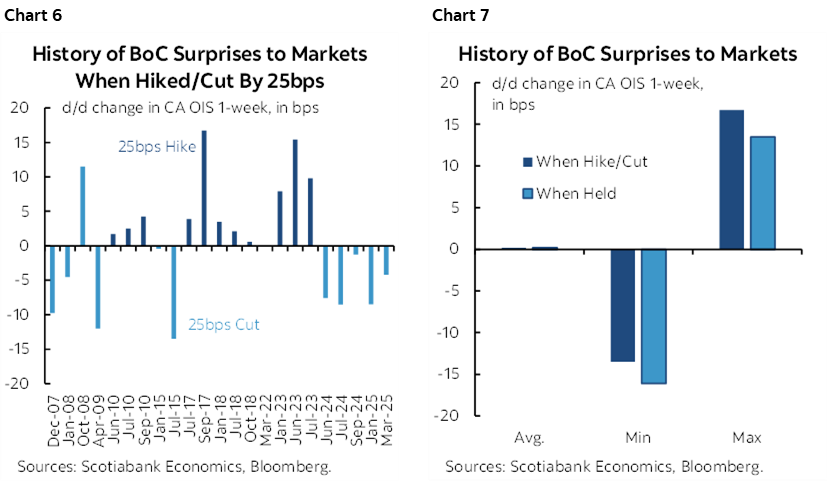

Separately, as for surprising markets, barring a massive change in meeting pricing today, the statistical odds of the BoC stuffing markets by as much as 22–23bps as presently priced are extremely low.

There are two ways of looking at this. First is the surprise factor when they’ve cut or hiked by 25bps; in about the past couple of decades, they’ve never surprised by more than 17bps and that was only once (chart 6). Second is the surprise factor when markets are priced for a 25 cut or hike and the BoC doesn’t deliver the goods; the biggest OIS miss in either direction was 16bps (chart 7).

They would have to have an extremely good narrative if they held and hence tightened financial conditions by a) wiping out current pricing, and b) sending a signal to markets to wipe out future easing which is what I think the aftershock would be like. Fail to cut and you’ve got a bigger communications problem now and subsequently than just cutting and shrugging shoulders on the bias which Macklem is typically loath to provide in any event.

OTHER STUFF

We’ll also get Canadian housing starts updated for August just before CPI and that have been on a tear for the prior four months (8:15amET) and then US industrial output, also for August (9:15amET). The US also updates import prices for August (8:30amET), business inventories for July (10amET) and the NAHB’s housing index including model home foot traffic as a guide to new home sales.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.