ON DECK FOR THURSDAY, SEPTEMBER 11

KEY POINTS:

- Markets await overlapping US CPI, ECB communications

- US CPI preview

- The FOMC’s mind is very likely to be already made up about next week

- Why tariffs could take much longer to show up…

- …than ideologically motivated and impatient voices pretend

- Supply chains are probably at a highly nascent stage of inflationary upheaval…

- ...a pre-tariff and post-tariff effects cause long-tailed inflation risk

- Data quality issues continue to mar the reliability of US CPI—and may get worse

- ECB to hold, guidance probably mixed…

- …as divided officials let fresh baseline forecasts do the talking

US CPI and the ECB are the main events. They will overlap upon one another which could complicate market effects. I think there is low risk that ECB communications will distort reactions to US CPI given widespread expectations for a hold and conflicting views across officials toward the future policy bias. ECB forecasts could be a wildcard.

US CPI PREVIEW

What follows is a bit of an elaboration on what I wrote in my weekly last Friday.

CPI for August (8:30amET) is highly unlikely to affect next week’s FOMC decision that is probably set in favour of a 25bps cut. Chair Powell clearly pivoted toward the labour market side of concerns and perhaps prematurely. I don’t see the arguments for upsizing, perhaps especially given bloated valuations across equity, credit, cybercurrencies etc. Broad GDP growth continues to track well albeit with mixed details. GDP is correlated with employment over time and GDP can inform output gaps which can influence inflation over time and so GDP is linked to dual mandate variables that the FOMC monitors.

Scotia’s house calls for headline and core CPI are 0.3% m/m SA for both. Out of 76 estimates for core within ’berg’s consensus, 57 expect 0.3%, 15 expect 0.4%, and four expect 0.2%. Everyone is dealing with high uncertainty to their estimates. In my judgement, the tail risk may be more skewed toward a softer reading if the prior surge in core services mean reverts, while the upside tail risk is likely more driven by tariff uncertainties.

As for drivers of major shares of the CPI basket:

- for headline CPI, gasoline should be a slight positive contributor.

- I don’t expect much of a contribution to total CPI from food prices.

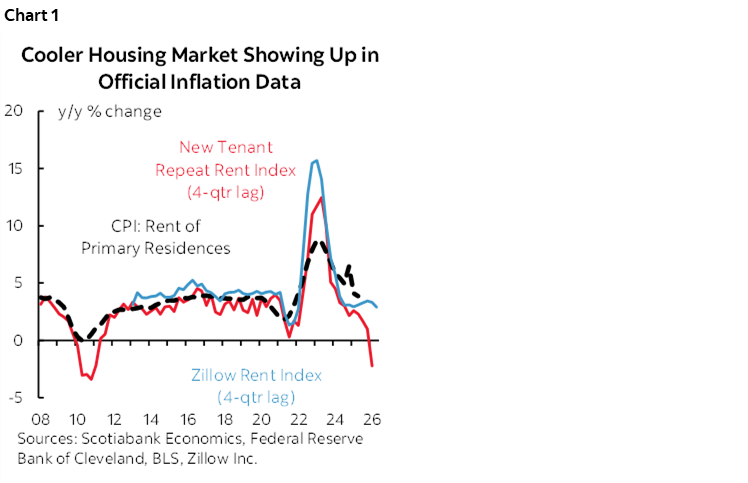

- housing’s weight of just over one-third of total CPI is likely to remain a small positive contributor primarily through owners’ equivalent rent. It has waned as an influence and will likely continue to moderate (chart 1).

- vehicle prices (~7% weight) are expected to be a small drag driven primarily by used vehicles.

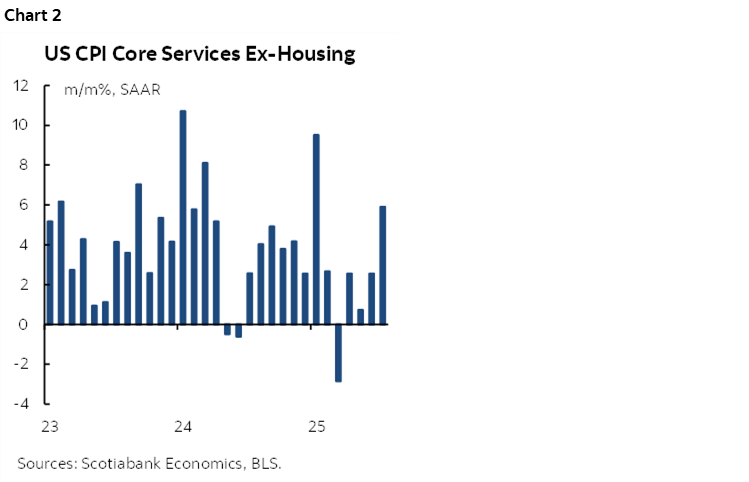

- where downside pressure could emerge may be through mean reversion in the core services less housing and energy services category. It was up sharply in July at 0.5% m/m SA (chart 2) and at about a 25% weight in the basket a prime driver of the warm total core CPI jump of 0.3% in July.

- for tariff effects, home in on the goods category named ‘commodities less food and energy’ and its components that carry about a 19% weight. There has been slight upward pressure over the past couple of months but nothing terribly unusual to date (chart 3).

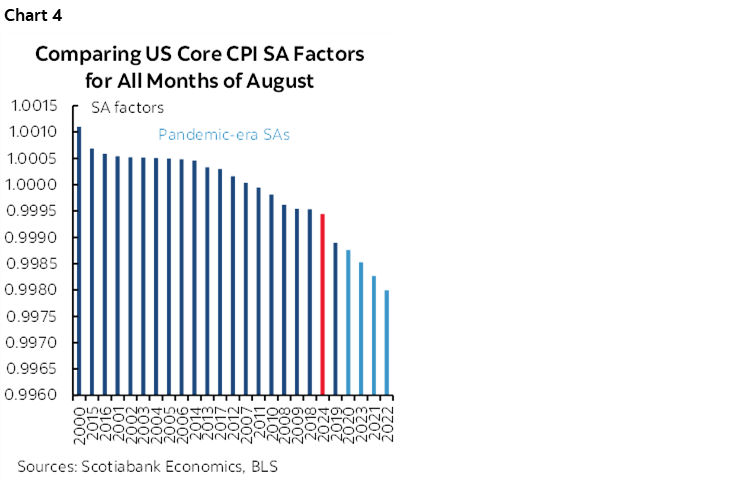

Seasonal adjustment factors could exert slightly abnormal downward effects on core CPI given the recency bias to how they are calculated which has pushed them lower over this decade (chart 4). That said, the 2024 core CPI SA factor edged higher than prior years so watch this carefully this morning to see if the recency bias in SA factors is maturing and pivoting.

Apart from m/m pressures, one driver of the y/y core rate is likely to be the shift in year-ago base effects that on its own would exert downward pressure if nothing else changed.

And we’ll hear the usual silliness on very short-term effects of tariffs, if any. I don’t trust anyone who says there will be no tariff pass through nor anyone who says there will be full pass through. There is an ideological bias behind both camps rather an empirical objectivity.

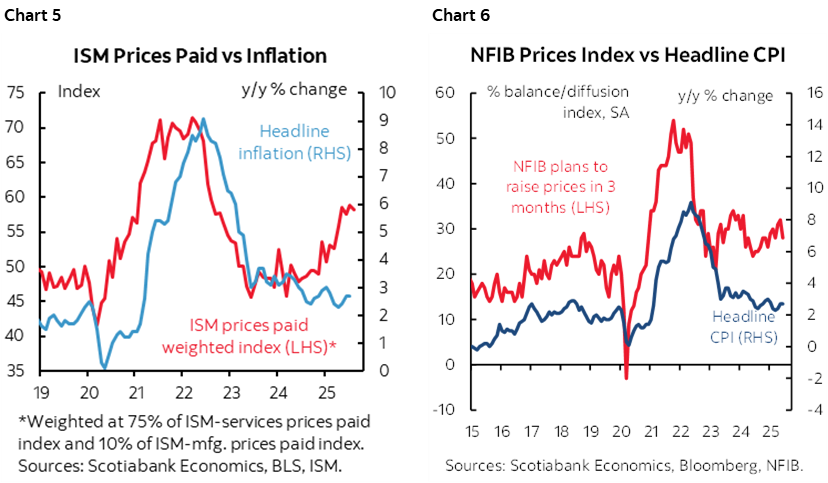

I also don’t trust arguments looking for immediate effects in each very short-term inflation reading. Gauges like ISM prices paid (chart 5), or the NFIB prices index (chart 6) indicate strongly correlated lagging upward pressure on inflation but timing it to the exact month is impossible versus the smoothed trend over coming months and quarters. Tariffs and supply-chain turmoil driven by tariffs and pre-tariff developments operate with long fuses. Nothing gets settled in one month, 3 months, 6 months, 12 months etc. Here are some of the forces that can drag out the effects:

- inventory at old prices. Until they are depleted, tariff effects will be slow to emerge. With all of the fits and starts for tariffs, companies engaged in serial bouts of tariff front-running on order books to exploit each delay in tariff implementation. That prolongs the adjustments. That process is stopping now that tariffs have been broadly applied but the effects will likely linger.

- seasonal factors like ordering for the holiday season, introducing new product lines such as for autos or smart phones, can create lagging effects of tariffs. Pricing models adjust with varying frequencies.

- profit margins can absorb tariffs at first but probably not indefinitely. S&P500 margins were high going into the tariffs. Companies may absorb tariffs at first, but if tariffs are sustained, then shareholders would likely pressure boards to be profit maximizers and pass on at least some of the tariffs according to industry-specific pricing power and incidence effects. If your job is to foist bonds onto the unsuspecting, then you probably lean on profit margins permanently absorbing tariffs which is bad for earnings and equities, probably good for Treasuries!

- companies may be reticent to adjust prices for tariffs at first while monitoring to see whether tariffs are a longer-lived factor to get used to or a shorter-term negotiating tactic. There are costs to adjusting prices and reputational factors with consumers to consider. The longer tariffs last, the more likely pass through occurs.

And underlying supply chain drivers can take years to work through. This is my biggest worry about inflationary pressures and traces itself to developments before tariffs and because of tariffs. Border frictions have risen over the past decade since the 2016 Brexit vote and 2016 US election through the first round of Trump 1.0 protectionism into the pandemic and through geopolitical conflicts and now into Trump 2.0 protectionism that is much more serious than under 1.0. For years, c-suites pursued massive outsourcing into the lowest cost jurisdictions of the world economy with little worry that more distant and more spread out supply chains could one day seize up. Higher border frictions to supply chains are profoundly changing this dynamic. They pivot companies away from lowering operating expense ratios as the sole motive toward lowering financial distress costs reflected in the inability to secure product when needed, foregone sales, or outright bankruptcy. Supply chains are under high pressure to tighten up, come closer together, absorb higher inventory levels and costs, and to abandon legacy assets in high-risk low-cost jurisdictions. All of this is a wave of cost pressures facing businesses and someone has to absorb that cost which means multiple stakeholders including consumers over time.

Once we have the CPI readings we can move toward calculating PCE. Take the core CPI change and adjust for the following:

- differing weights in CPI and PCE.

- Yesterday’s relevant PPI components add 0.07 ppts to core PCE. Since headline readings for inflation gauges are in the tenths of percentage points we need to round up. Basic arithmetic rounds that up to a 0.1 ppts contribution.

- Judgement around PCE versus CPI substitution effects. CPI adjusts spending weights once a year whereas PCE does it dynamically. In response to tariffs and other shocks, consumers may substitute away from the most affected products and toward alternatives or other types of spending.

- judgement around other methodological differences between PCE and CPI.

And throughout it all, don’t forget the role played by suspect data quality. That’s a serious issue. It’s serious not only in terms of the questionable seasonal adjustments, but also in terms of the falling survey response rates across a broad swath of US data. In terms of CPI, a record one-third of the CPI basket is imputed using different methods absent resources for accurately collecting prices due to recent budget cutbacks (chart 7). Just wait until the thoroughly unqualified and politically motivated E.J. Antoni takes over at the BLS. MAGA is sinking its teeth into data with the aim of lowering transparency and accountability.

ECB ON HOLD

The ECB is likely to remain on hold at 8:15amET followed by President Lagarde’s press conference 30 minutes later. Five dozen forecasters expect a hold and markets are fully priced for a hold with minimal chance at a deposit rate change for the next several meetings.

The ECB has already chopped its key rate in half since the end of last year. Opinions on next steps are divided across Governing Council members.

Moderates, like Estonia’s Müller, prefer to “take the time and monitor” new information. France’s Villeroy flags “very well controlled” inflation.

More hawkish minded members, like Board member Schnabel, think “we may be already accommodative and therefore I do not see reason for a further rate cut.” Acting member from Slovenia, Primoz Dolenc, noted that after a hold this time, the policy rate “could go in either direction” in future. Hawkish members can point to the fact that core inflation in m/m terms remains relatively high of late compared to like months of seasonally unadjusted figures and services inflation remains sticky (chart 11).

More dovish voices somewhat atypically come from the north with Finland’s Rehn “there are more downside risks to inflation” ahead.

New forecasts to be provided at this meeting will provide a balanced sense of where the consensus of policy markets stands on the path ahead.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.