ON DECK FOR WEDNESDAY, SEPTEMBER 10

KEY POINTS:

- Markets face two days of US inflation updates

- US producer prices matter for two reasons

- Judge rejects ‘cause’ argument for Trump to fire Fed’s Cook

- Crazy town brings more tariff threats

- China doesn’t care that it has no inflation...

- …and Mundell’s Impossible Trinity says why

- Record nonfarm downgrade still faces revision risk

- Chile’s central bank held as expected

- Brazil’s inflation update won’t matter to BCB…

- …but the pending Bolsonaro decision might

- The US Supreme Court’s ‘fast’ tariff review is anything but; uncertainty prolonged

The main focus is upon a few global inflation readings in the wake of at least a temporary block by a judge last night against Trump’s attempt to fire Federal Reserve Governor Cook. Tops will be US producer prices as a warm-up to tomorrow’s US CPI. That said, to flag data updates seems a rather pedestrian consideration in the context of other forces as follows.

RECAP OF US PAYROLL REVISIONS

This was covered with clients and chat rooms yesterday but here’s a refresher. Yesterday’s annual benchmarking revisions revealed the biggest annual downward revision to nonfarm payrolls on record (chart 1) but the still real likelihood of further material revisions in either direction when the final benchmarking exercise is complete in February. The QCEWS dataset that is the foundation for the annual payrolls benchmarking exercise is itself subject to wild quarterly revisions (chart 2). Still, what the revisions did was to cut in half the average monthly pace of payroll increases to only about 75k over the April 1st 2024 to March 31st 2025 period. QCEWS accounts also drive revisions to Gross Domestic Income and GDP that we’ll start to get with the next batch of GDP revisions on September 25th for Q2 but also Q1 to incorporate the wages and salaries numbers out of QCEW.

AMERICA’S SUPREME COURT TARIFF REVIEW IS ANYTHING BUT FAST...

Also beyond PPI we have the Supreme Court’s definition of ‘fast track’ that won’t have them running in the Olympics any time soon. They agreed to review the legitimacy of Trump’s tariffs by starting to hear arguments in early November. Starting. Then hopefully a decision by year-end. That means an optimistic scenario is that the tariffs will stick around for at least another three months or so and with it the uncertainty around how the bench that Trump stacked might view them.

...AS NEW TARIFF THREATS LOOM

The Court may have gotten even more reason to reject Trump’s abuse of national security legislation when imposing tariffs. Trump reportedly asked the EU to impose 100% tariffs on China and India and that the US would match them in order to pressure Russia to back off Ukraine. Crazy town just got crazier. The macroeconomic consequences of doing so would be profound for the world economy especially given likely retaliation, leaving the best hope being for the EU to simply say no. China has countless ways in which it can retaliate against the US and Europe as the world continues to become increasingly dangerous.

WHY US PRODUCER PRICES MATTER

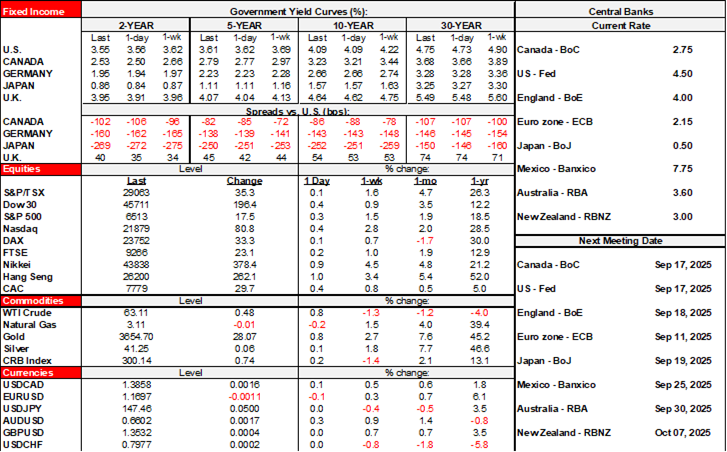

US producer prices for August get updated at 8:30amET. Headline and core are both expected to rise by 0.3% m/m SA. Take expectations with a lot of caution and not least of which because they were blown away the prior month. PPI matters for two reasons.

One reason is whether there is any further evidence of tariff pass through and other effects after core PPI smashed expectations with a jump of 0.9% in July. If so, then the next leg is the debate over pass through into consumer prices and the lags. July’s jump could be a tough act to follow in my opinion. Recall that 0.9% lift was more than four times consensus and categories that led the gain included ones directly and indirectly related to trade or with relatively high import content. They included categories like trade services (+2% m/m), transportation and warehousing (+1%), food (+1.4%), several capital goods categories and parts of finished consumer goods. Nah, no evidence on effects of tariffs and trade turmoil…

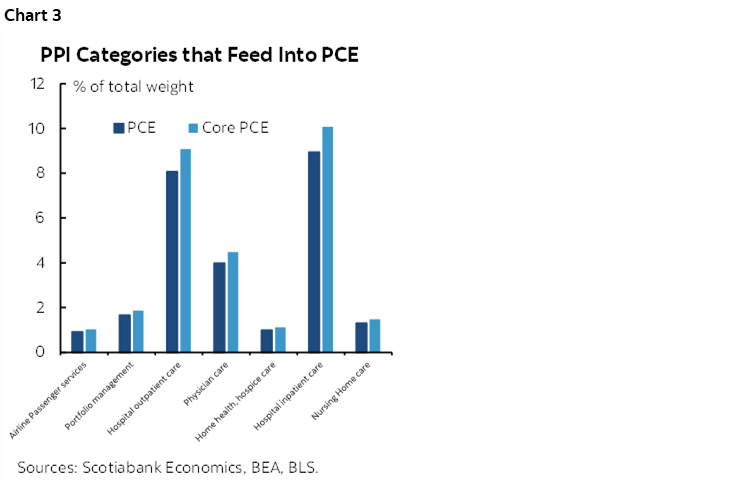

The second reason concerns the weighted components that flow through to PCE that we get on September 26th. The weights for the relevant categories are shown in chart 3. When the pertinent PPI categories are combined with the CPI release and CPI weight adjustments to PCE, the Fed will have pretty much all it needs to form a reasonable expectation for the PCE gauges by Thursday.

One other wild card in translating PPI and CPI to PCE is the substitution effect; PCE adjusts spending weights dynamically and hence may capture substitution away from some goods—especially tariffed ones—whereas CPI has fixed weights that are now updated annually. While the CPI weights are adjusted more frequently than in the past, they still may not adjust frequently enough at critical moments perhaps like today.

CHINA DOESN’T CARE ABOUT NO INFLATION AND HERE’S WHY

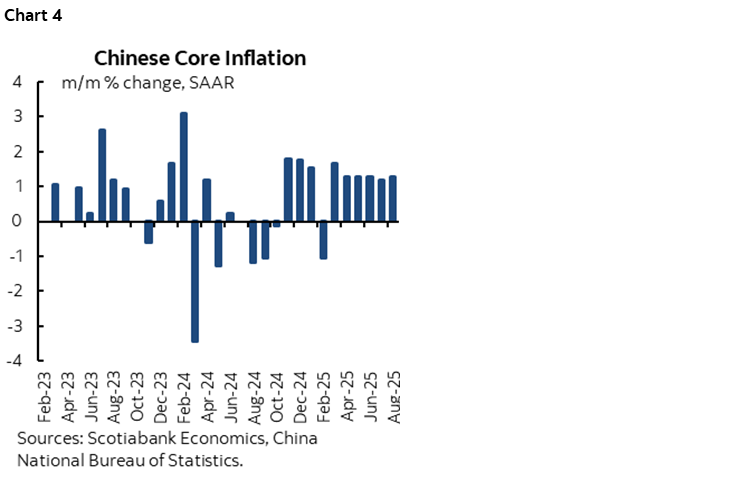

Chinese inflation remains non-existent as CPI landed at –0.4% y/y and core at 0.9% y/y. Core CPI is soft even on a month-ago seasonally adjusted and annualized basis (chart 4). The PBOC basically ignores the 2% target that itself was lowered this year from the previous 3% target they almost never hit. China generally illustrates Mundell’s Impossible Trinity that you cannot have fixed exchange rates (or dirty managed ones), independent monetary policy, and free capital flows simultaneously.

CHILE’S CENTRAL BANK HOLDS

Chile’s central bank held its overnight rate at 4.75% as widely anticipated last evening. They batted away the previous day’s weaker than expected inflation readings for August. Instead, they indicated a desire to gather more information on tariff and other effects on inflation before contemplating any potential further easing while revising up future core CPI expectations.

BRAZILIAN INFLATION PROBABLY WON’T MATTER TO BCB; BOLSONARO DECISION MIGHT

It’s doubtful that Brazil’s inflation report for August (8amET) will matter much to BCB’s decision on the Selic rate just hours after next week’s FOMC decision. BCB’s last decision seemed to end the hiking campaign by noting that a potential hold for “a very prolonged period” could ensue.

What might matter more is the pending decision by Brazil’s Supreme Court on the fate of former President Bolsonaro after his alleged involvement in a coup attempt. Two judges have voted to find him guilty. One more out of the remaining three must do likewise to have a conviction. This matters for two reasons: a) for anyone interested in Brazil, and b) because it may trigger more retaliation by Trump in defence of his kindred spirit.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.