ON DECK FOR MONDAY, OCTOBER 6

KEY POINTS:

- Political risk is in the driver’s seat

- Japan’s likely new PM drives large market moves…

- …on speculation she will be a fiscal expansionist

- France’s new PM resigns weeks into the job…

- …as political dysfunction continues to stymie fiscal reforms

- Global Week Ahead — Pick Your Subsidies (here)

Political risk is in the driver’s seat once more. The action is focused upon France and Japan amid an otherwise empty calendar. Spillover effects are driving bear steepening in US Ts.

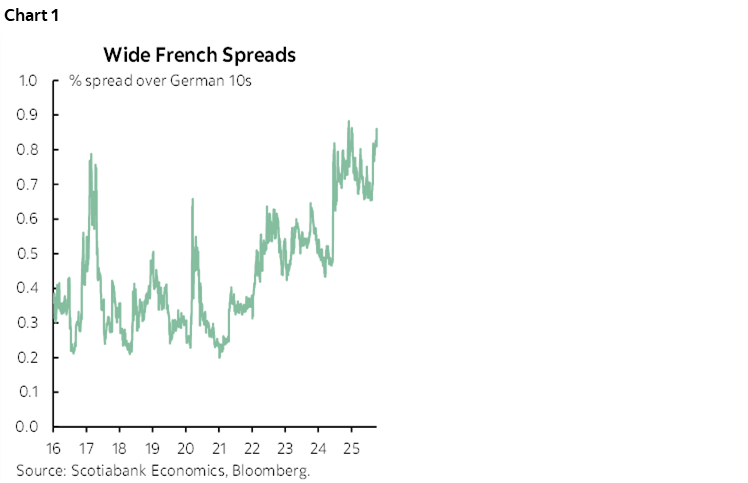

FRENCH POLITICAL TURMOIL CONTINUES

French bonds are getting hit by the latest crisis. Spreads over 10-year bunds are about 5bps wider and the CAC40 is underperforming with a 1½% drop.

The catalyst is that yet another French Prime Minister—this time Sebastien Lecornu—has resigned only a few weeks into the job. He wasn’t terribly successful at steering budget proposals, but the tipping point was when the opposition as well as a key figure from the center-right lashed out at President Macron’s appointment of essentially the same cabinet amid demands for fresh faces. France remains paralyzed by political dysfunction that is preventing fiscal reforms.

MARKETS SPECULATE THAT JAPAN’S NEW PM WILL BE A FISCAL EXPANSIONIST

The yen is about 2% lower to the dollar and leading underperformers. The Nikkei ripped higher by almost 5% overnight. The JGBs curve bull steepened with 2s richer by about 4bps.

The catalyst? Japan’s Liberal Democratic Party chose Sanae Takaichi as their leader and she is very likely to be voted in as PM next week. She was an ally of the late former PM Shinzo Abe and is widely viewed as being pro-stimulus and pro-reform while skeptical toward BoJ policy tightening. Clearly we need to see concrete proposals and in the context of a divided parliament in which her party no longer holds majorities in either chamber. For now, markets are behaving in knee-jerk fashion by assuming she will add to fiscal expansionism.

I’m not sure about speculation that BoJ hike pricing should be rolled back. Pricing for the October 29th decision was chopped from 14bps of a quarter point hike to 6 bps. A big ‘if’ is whether more fiscal stimulus can be pushed through, but if it is, then it might embolden BoJ hikes.

Other than watch for any further developments around the US government’s shutdown. No meaningful progress was made over the weekend.

There are no material releases due out.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.