ON DECK FOR THURSDAY, OCTOBER 30

KEY POINTS:

- Soft equity tone shakes off US-China agreement…

- ...while focusing more on mixed US tech earnings, Fed signals

- US-China agreement is more tactical hubris than any grand bargain

- Recaps: Fed not saying it will skip versus demanding more flexibility…

- ...while the BoC is clearly stating it is on an extended pause

- EGBs underperform as they catch up on the Fed, react to Eurozone inflation

- BoJ held and retained optionality toward hiking soon

- ECB to stay on hold at a neutral rate…

- ...after fresh warnings signs on inflation

- The Eurozone is barely eking out growth

- Mexico’s economy probably contracted in Q3

- Canada to update lagging payrolls. Yawn.

- Apple, Amazon to release in the after-market

Global markets are largely shaking off US-China developments as being long on hubris from the American side and short on substance. It has the look and feel of a minor de-escalation of tensions in a tactical set of arrangements that leave in place the deepest forms of trade and security tensions between the two economies.

There is also little follow through in rates on yesterday’s Fed (recap here) and BoC (recap here) communications, although a more cautious Fed may be a contributing factor behind a slightly soft tone in equities in addition to the influence of very mixed US tech earnings from Meta, Microsoft and Alphabet. The BoC is very clearly signalling they’re done while the Fed isn’t slamming the door on a December cut versus bending markets to provide more policy optionality around the meeting.

BoJ signals appeared to retain optionality to hike again at either the December or January meeting but were generally not very impactful. The ECB is on tap after upside surprises to German and Spanish inflation that built upon slightly higher EGB yields at the cash open. More key US tech earnings are on tap today after mixed results in yesterday’s after-market that are keeping equities playing defence.

LIMITED TACTICAL US-CHINA AGREEMENT

This is no grand bargain and it’s not looking like we’re on the path toward achieving one. What was announced by the US and China feels more like a minor set of tactical arrangements that deescalated tensions in some ways but without addressing the major issues. Here are some of the details.

- there is no formal agreement or joint statement that would give markets confidence that a firm deal is being achieved.

- Chinese export controls on rare earths and US export controls on some chips except for the most advanced Nvidia chips were postponed by one year.

- fentanyl tariffs were reduced from 20% to 10% on the condition that China controls the export of chemicals used to make fentanyl.

- the vast bulk of other US tariffs on China remain intact such that the tariff relief is minor. US tariffs on imports from China will be 45% after the reduction.

- China will buy more US soybeans which helps part of Trump’s base.

- The US will suspend for one year its plans to add export restrictions against certain Chinese companies.

- The US will suspend port fees on China’s shipbuilding industries for a year and China will suspend its related countermeasures.

- There was vague talk of China buying US energy but nothing substantive beyond Trump’s claims.

- Other sore points in the relations were not advanced, such as Taiwan and TikTok.

- Trump is to visit China in April and President Xi Jinping is to reciprocate.

BOJ HELD

The Bank of Japan held its target rate unchanged at 0.5% as universally expected but with two dissenters who preferred a hike at this meeting. Inflation forecasts were left unchanged with core CPI projected to land at 2.7% this year, 1.8% next, and 2.0% in 2027. Markets reduced some of the pricing for a hike in December to just under a 50–50 probability and reduced pricing for a hike in January by a few points but still to about 80% odds. Overall, Governor Ueda’s remarks were noncommittal but appeared to leave the door open to moving as soon as the next meeting while sounding encouraged that the next round of Spring wage negotiations will further reinforce a positive wage-price cycle.

ECB TO HOLD

The ECB is universally expected to remain on hold today with markets fully priced and consensus unanimous (statement 9:15amET), press conference 9:45amET). With the policy rate within neutral bands and faced with residual inflation risk, the ECB is likely on a long hold. Like elsewhere (eg. Canada for one), the ECB is focused upon an expected surge of fiscal policy easing as governments ramp up spending particularly on defence and related activities.

OVERNIGHT DATA

European inflation and GDP reports dominated overnight calendar-based data developments.

Germany’s economy remains weak. GDP was flat in Q3 as expected with a minor upward revision to Q2 (-0.2% q/q instead of -0.3%).

France’s economy surprised positively with GDP up 0.5% q/q in Q3 (0.2% consensus).

Italy’s economy was flat in Q3 (0.1% consensus).

We already had Spanish GDP yesterday that grew 0.6%.

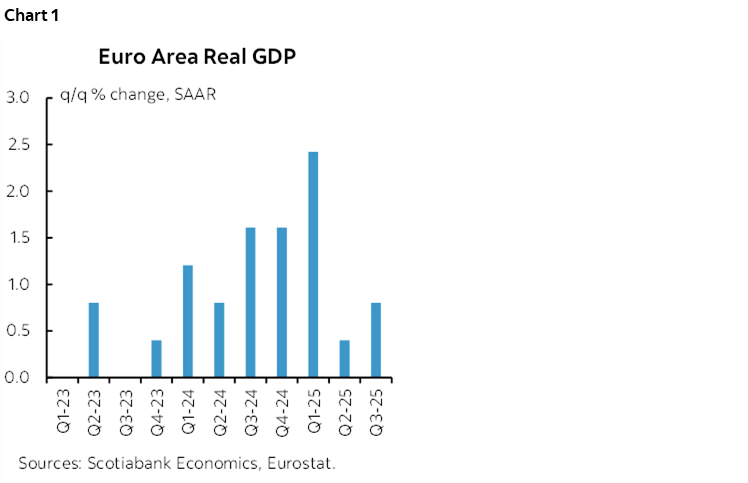

Overall Eurozone GDP therefore landed a tick above consensus at 0.2% q/q in Q3. Growth is very weak, but the Eurozone is avoiding technical recession so far (chart 1).

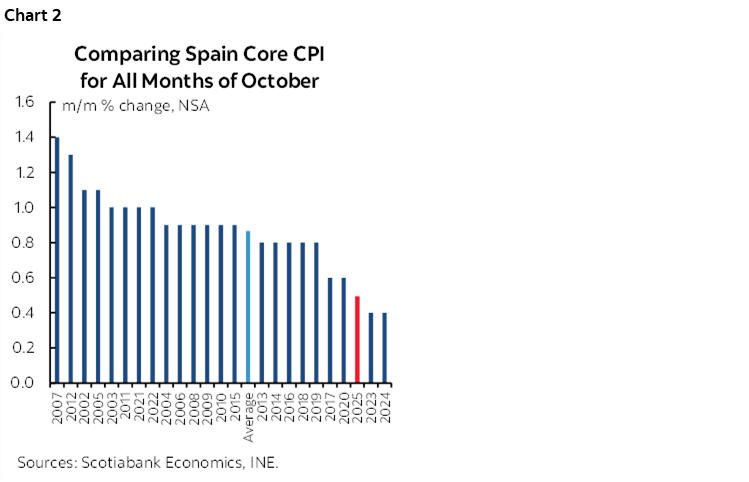

Spanish EU-harmonized CPI inflation surprised higher than expected at 0.5% m/m (0.3% consensus) with core one-tick higher than consensus at 2.5% y/y. Still, core CPI in m/m seasonally unadjusted terms was among the weakest Septembers on record (chart 2).

German inflation is also looking warmer than consensus expected. Individual states released estimates between 0.3–0.4% m/m this morning versus consensus estimates for total German CPI to be up 0.2% when we get the national reading a little later this morning (9amET).

CANADIAN PAYROLLS, MEXICAN GDP ON TAP

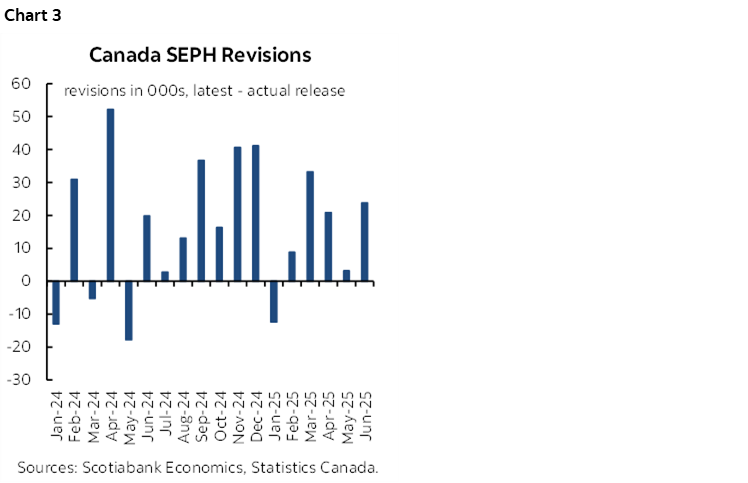

Ignore. That’s my usual advice. Canadian payrolls lag the more important Labour Force Survey by two months. We get August payrolls this morning (8:30amET), but we’ll have LFS for October next Friday. SEPH payrolls are *not* harder data which is a common misconception. They are wickedly revised every month (chart 3). Further, because they exclude off-payroll employers by definition, they provide a highly incomplete picture of the job market compared to the LFS report. I expect payback in next Friday’s LFS with jobs down 25k after the large positive surprise in September.

Mexico’s economy is expected to contract when we get Q3 GDP this morning (8amET). The economy is expected to contract by about -0.4% q/q SA.

MORE TECH EARNINGS

Two US-tech heavyweights land in the aftermarket today. We get Q3 earnings and guidance from Apple (consensus EPS US$1.77) and Amazon (consensus EPS US$1.56).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.