ON DECK FOR FRIDAY, OCTOBER 3

KEY POINTS:

- An anticlimactic end to the trading week

- Nonfarm payrolls will only be released after the US government shutdown ends

- ISM-services takes on more prominence given nonfarm’s absence

- The BoC’s academic exercise may be missing the point again

Equities are slightly bid and sovereign bonds are mostly treading water with a mild exception being slight outperformance by gilts. The dollar is a touch weaker against most of the majors except the yen. Overnight data was very light with just a large downside miss on French industrial output and higher than expected Turkish inflation.

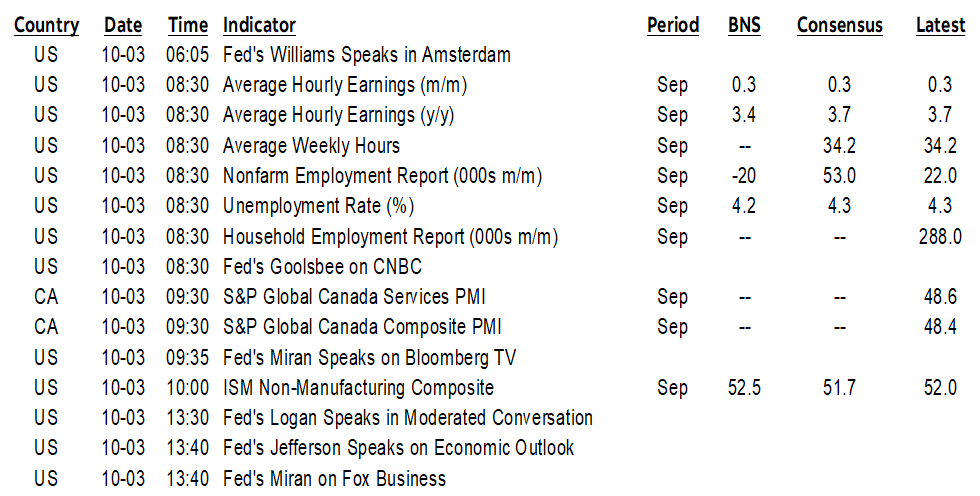

US ISM-services (10amET) will take on elevated importance in nonfarm’s absence given it will not be released until after the government reopens. Instead of being the second-fiddle trade to payrolls, it now becomes basically the only calendar-based trade to end the week. Little change is expected from the prior month’s 52.0 reading that indicated mild above-50 growth, but this measure is highly prone to surprises.

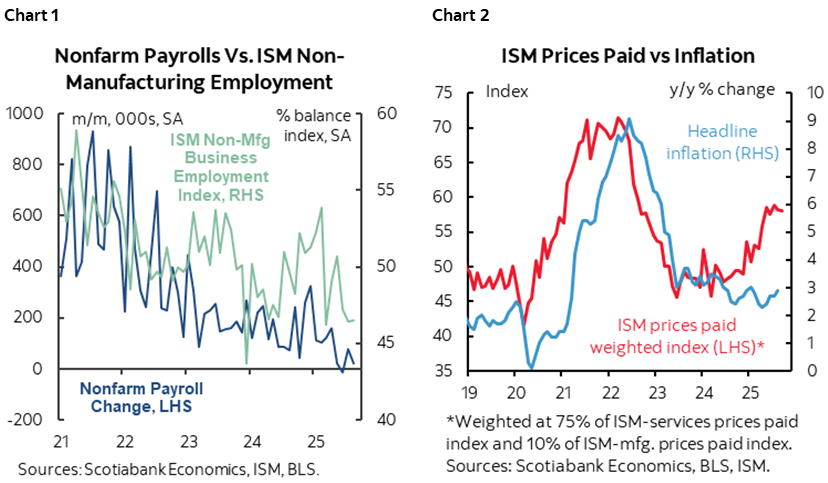

The employment subindex isn’t of much use to forecasting nonfarm payrolls (chart 1). We’ll also use the weighted prices measures from ISM-manufacturing and ISM-services together to update what purchasing managers are indicated may be coming to highly correlated moves in US inflation (chart 2).

More theatrics around the US shutdown are also expected perhaps resulting in targets for firings and department closings assuming it’s not just an idle or temporary threat.

THE BOC’S 5-YEAR REVIEW SHOULD EMPHASIZE SIMPLICITY AND CLARITY

One of the BoC’s Deputy Governors, Rhys Mendes, delivered a speech yesterday on what the BoC is thinking in terms of how to measure and track inflation (here). It was well articulated and built upon prior comments by Governor Macklem concerning next year’s 5-year review of its inflation targeting framework. Macklem had previously said here that they are looking at alternative measures of core inflation but reinforced that what’s not open to debate is the 2% medium-term inflation target itself.

Mendes deserves credit for delivering a focused speech on the topic. I’ll share a few opinions on elements of it.

First, his explanation of why they think underlying inflation is around 2½% instead of the y/y rates for trimmed mean CPI and weighted median CPI that are running at 3% felt weak. Somehow by fitting an arbitrary trend line to an arbitrary correlation spits out 2½%.

Maybe there is a simpler way of making the argument that Mendes should have explained and that I’ve been emphasizing as superior for years. It is that the TM and WM measures in m/m rates of growth at a seasonally adjusted and annualized rate have been running at around 2½% for the past couple of months (chart 3). This approach gets around the flaw in the TM and WM measures as commonly cited in y/y terms which is the issue that they turn far too slowly at inflection points. Both measures take each month’s weighted m/m contributions and compound them over twelve months. By the time they more heavily weight more recent price developments it may be too late for policy—and markets—to react. Maybe that’s a partial reason why the BoC was so slow-footed around inflation risk in the pandemic. We want a measure of core inflation that turns more rapidly if there are sudden shocks to new information, like, oh, pandemics and trade wars, but not so rapidly as to be very noisy. My suggestion has been to take a moving average of the m/m SAAR measures of both TM and WM say over three months and supplement with traditional core, breadth measures and judgement around emerging shocks.

Whatever the measure, if your judgement around those emerging shocks is off base—as the BoC’s was by downplaying inflation risk for far too long in the pandemic—then it doesn’t matter what measure of core inflation you say you are using.

But pointing to 2½% m/m SAAR of late could also be a dicey argument since the measures have only been around that rate over the past couple of months. Prior to that, these readings were spending much of this year in the 3% and 4% range in m/m SAAR terms as shown in the table. Core inflation has thrown many head fakes over the years in Canada and elsewhere and there are many complicated drivers, so we need more evidence that it is truly waning and expected to remain down. Further, Statcan’s tendency to revise seasonal adjustment factors and hence revise TM and WM measures each time they publish should also temper excessive reliance upon shorter-term data.

Mendes’ speech correctly notes the issues with mortgage interest cost, but it’s a moot point that most folks in this biz have long moved past. Everyone knows to strip it out one way or the other.

What I fear the BoC misses is the need for relative simplicity in the chosen measures of core inflation which is where my next comment on the speech comes in. Mendes raised concepts like ‘multivariate core trend inflation’ and ‘a clustering algorithm technique’ that uses artificial intelligence. Huh? Good heavens, I wouldn’t want to be behind a BoC official ordering a drink at Starbucks because it would take an hour to spit out their order and they’d probably complain it wasn’t done exactly right while holding everyone up for even longer! They will broaden the publication of more core measures in an interactive dashboard starting in 2026.

So, let’s count the measures now. Traditional core CPI ex-food and energy which seems good enough for many other central banks, trimmed mean, weighted median, common component that’s widely rejected, CPI excluding the 8 most volatile components both without and without indirect taxes, CPI ex-f&e and ex indirect taxes, ‘multivariate core trend inflation,’ ‘a clustering algorithm’ etc etc.

I get that there is somewhat more information to multiple measures, but the BoC risks widespread confusion over what its operational target is and what it may react to. At some point you’ve crossed the line between the value of more information and the disservice of confusing everyone. One key to an operational gauge is that it should be forecastable. Then again, perhaps when you don’t know how to conduct policy in an uncertain world you try to get everyone off your case by confusing the heck out of them over exactly what you follow and target in addition to how you are forecasting inflation and the judgement that should dominate models that have often failed.

The BoC did just that in its last review when it conducted a ‘horse race’ between entirely different targeting frameworks, like price level targeting, NGDP targeting, etc, only to conclude that it would stick to inflation targeting after all. Former Governor Poloz introduced the TM, WM and common component measures in 2016. Adding more and more measures of core inflation that you say you are tracking in next year’s review but not really and kinda sorta doesn’t help transparency and communications that are too often a weak point especially around forward guidance. Keep it simple, intelligent folks—it’s your judgement on what to expect that matters far more anyway.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.