ON DECK FOR WEDNESDAY, OCTOBER 29

KEY POINTS:

- Global markets await the Fed, BoC and US tech earnings

- BoC expected to cut with highly cautious bias…

- ...amid no rush to alter balance sheet plans yet, but it’s coming

- FOMC expected to cut, guide more easing, probably end QT

- RBA cut bets crushed by Aussie CPI

- BCCh held as expected, sounds patient toward future easing

- US big tech earnings in the after-market

The week starts today. A packed line-up lies in store with most of the focus on the Fed, BoC and high earnings risk with several big tech firms due out in today’s after-market. Overnight developments were mainly focused upon Australian CCPI and last evening’s expected hold by Chile’s central bank.

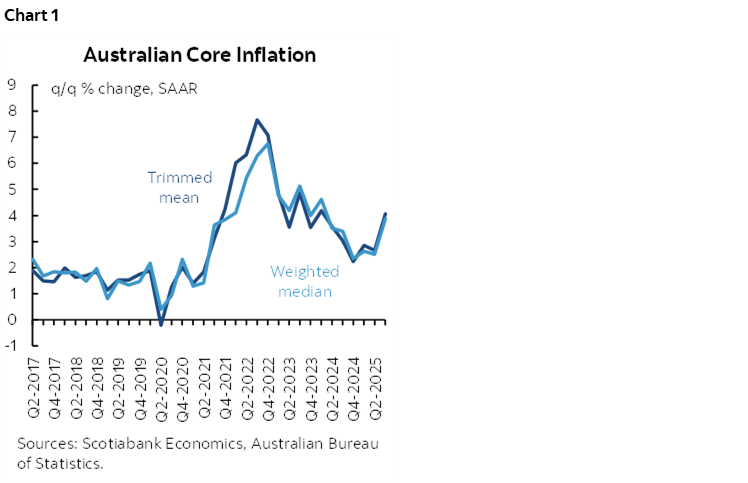

AUSSIE CPI CRUSHES RBA BETS

Stronger than expected Australian inflation slammed Australia’s rates curve and buoyed the A$. The curve bear flattened with the 2s yield up by about 12bps as pricing for the November 4th and December 9th RBA decisions largely removed a chance at a cut this year.

Q3 CPI was up 1.3% q/q SA non annualized (1.1% consensus). Core gauges also exceeded consensus with trimmed mean CPI up 1% (0.8% consensus) with a mild upward revision to Q2 and weighted median CPI was up 1.0% (0.9% consensus). Chart 1 shows the annualized quarter-over-quarter rates that were bottoming out and may be on a renewed upward path to be settled by more data the RBA should patiently observe.

CHILE’S CENTRAL BANK HOLDS

BCCh held its overnight rate at 4.75% last evening as widely expected. The decision was unanimous and the bias remained mildly dovish by indicating ongoing openness to further easing but a patient approach that wishes to gather more information on inflation risks.

BANK OF CANADA TO CUT WITH NEUTRAL-HAWKISH BIAS

The BoC is expected to cut 25bps this morning with all major shops in that camp and about 90% of a cut priced. The statement, MPR and Governor Macklem’s written opening remarks to his press conference arrive at 9:45amET and will be followed by the press conference at 10:30amET.

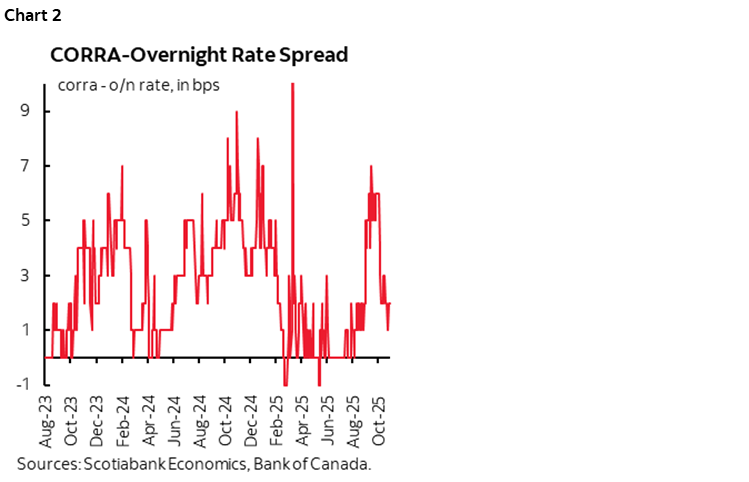

I don’t expect material developments around other policy instruments with CORRA coming back to be more in line with the o/n rate (chart 2). Guidance is expected to be neutral-hawkish, data dependent and highly measured.

Macklem has pledged to return to providing base case projections in this MPR because….erm….uncertainty has gone down. Righto, if you say so. Maybe he spoke too soon, but it’s too late now as they’ve committed to base case forecasts in a process that began weeks ago.

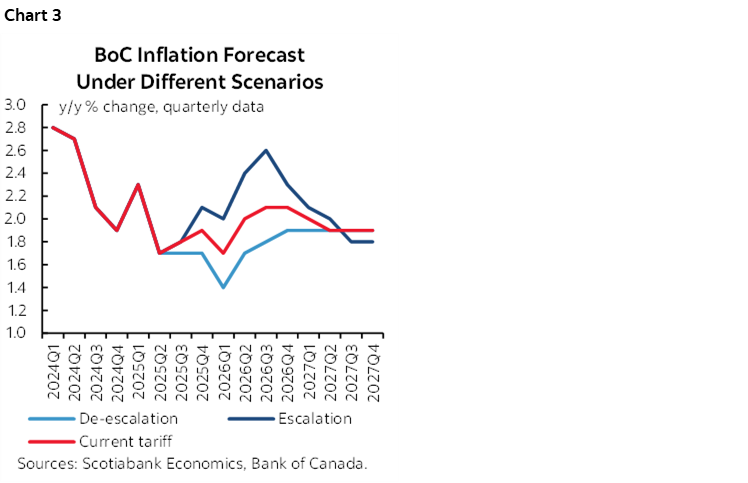

Watch for any signals in the medium-term inflation projections; the reason they are easing now is primarily to take out insurance against downside risk to sustainably achieving their 2% target which they roughly showed in the ‘current tariff’ scenario in the July MPR (chart 3). If they revise down despite a pair of recent cuts then it could be because they are biased toward more.

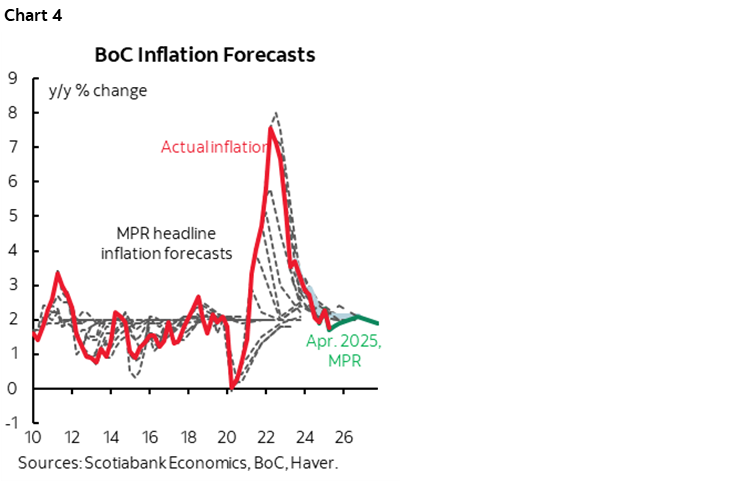

And take whatever forecasts their models spit out with a mountain of salt given the track record of various MPRs (dotted lines) compared to actual inflation (chart 4). They miss inflection points and routinely over—and undershoot for lengthy periods. Forecasting is more art than science and heavily driven by judgement. As the five-year review beckons, the differentiating factor in the BoC’s policy success going forward will rest upon improving judgement rather than fussing over which one of a bazillion current and possibly additional measures of core inflation may be the best.

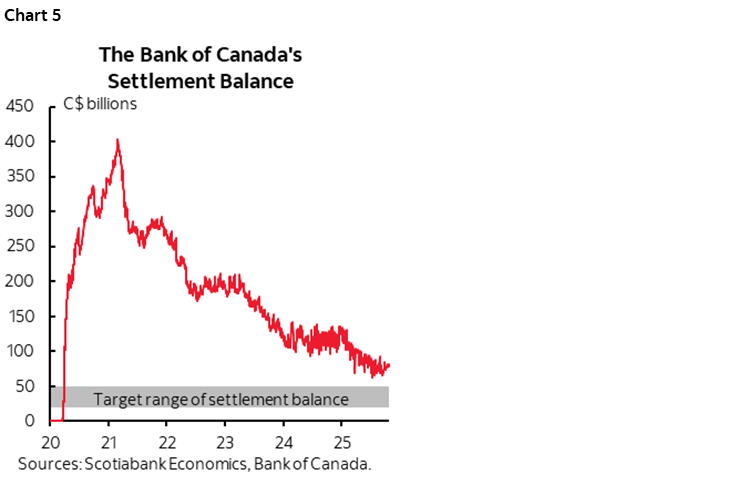

As for the balance sheet, settlement balances equal about C$78 billion and are therefore getting closer to the BoC’s $50–70 billion target range (chart 5) that was revised upward in Deputy Governor Gravelle’s speech at the start of the year (here). The BoC ended QT in the January 29th statement that surprised many relative to Gravelle’s more open 2025H1 guidance in his speech. The point is approaching when the BoC will have to communicate further intentions around its balance sheet management strategy. Recall that Gravelle’s speech indicated a desire to ramp up holdings of repos first in the aftermath of ending QT, then T-bills, while holding off on gross purchases of GoC bonds sometime thereafter but no earlier than late 2026 and in the normal course of monetary policy affairs (ie: not QE). Watch this space for further communications over 2026.

See my weekly for the case for a cut and the case for a hold in terms of the underlying arguments.

FOMC TO CUT, GUIDE MORE TO COME, END QT

The FOMC is universally expected to cut and probably announce the end of QT or at a minimum strongly intimate such a movement in the wake of Powell’s NBER speech and funding market developments since then. The statement lands at 2pmET and Chair Powell’s press conference begins at 2:30pmET for around 45 minutes.

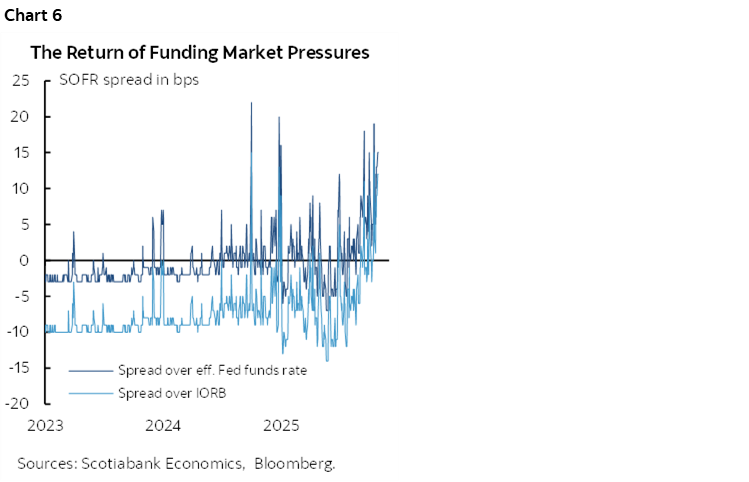

Funding market spreads increased from the 0–5bps range the day before Powell’s balance sheet speech to about 12–15bps now, applying more heat on the Fed to do something to address liquidity pressures (chart 6).

The next SEP with updated dot plot arrives in December. Key on any bias will be whether Powell repeats that not much has changed since the September dots in which case it is likely to remain game-on for another cut in December as per the median dot.

Between now and the next decision on December 10th it is possible that the backlog of data releases will be cleared. Trump has indicated that he wishes to sit down with the Dems next week after returning from his Asia sojourn.

See my weekly for a further preview of the Fed decision including the reasoning behind ending QT, the case for a cut and further cuts, but also the caution that long wave forces behind upward inflation risk require a great deal of patience and data to evaluate as the analog to the long wave of disinflationary pressures that came out of China in the 1990s onward. Obsessing over near-term fake inflation data—marred by proxy methods due to budget cuts and by distorted seasonality—misses the point and is overly myopic.

EARNINGS IN THE AFTER-MARKET

Big US tech updates earnings in the after-market today including Microsoft Q126 EPS US$3.68, Alphabet Q325 EPS US$2.26, eBay Q325 EPS US$1.34, and Meta Platforms Q325 US$6.74.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.