ON DECK FOR MONDAY, OCTOBER 27

KEY POINTS:

- Risk-on sentiment with mixed developments ahead of a big week

- Very limited US-China progress drives mild equity rally

- Why CAD, TSX and CGBs are ignoring Trump’s tantrum

- Why Trump’s ‘long time’ sentiment is likely mutual…

- …as Carney fights to sell his budget and avoid another election

- Argentina’s markets to rally on Milei’s veto-proof victory

- Data: resilient Chinese profits, 3½ year high for German business expectations

- US shutdown: lack of progress means no October payrolls next week

- Global Week Ahead — The Fed Faces Record US Policy Uncertainty (here)

Happy Monday. Risk assets are rallying on mixed developments and in anticipation of big developments this week. Very limited US-China agreements appear poised to be signed, US-Canada trade negotiations deteriorated but local markets are largely ignoring this, Argentina’s election is buoying local and EM sentiment, and we have very light data. The coming week is jam-packed with major central banks and Mag7 earnings. And my beloved Blue Jays are tied 1–1 against a team from Japan.

The results include higher US equity futures with gains around 1% on the S&P and Nasdaq, similar gains in China, and underperformance across Europe and Canada that are barely on the plus side. US Treasury yields are up by about 2bps across the curve. EGBs and gilts are flat. Aussie and Korean bonds are underperforming on spillover optimism from US-China developments. And the dollar is broadly weaker, although Cad is holding its own.

CAD, TSX IGNORE TRUMP’S TARIFF THREAT

CAD is largely shaking off the latest outburst by Trump. So are TSX futures. Canadian government bond yields are up about 1bp across the curve and therefore largely in sync with US Ts.

Why? Trump’s threat in a social media post on Saturday that he will impose an extra 10% tariff on Canada lacks important details and a formal order as usual, while local markets are probably more focused on the BoC’s pending decision, the coming budget and election risk. There is enough domestic content to noodle over without paying attention to Trump.

It’s unclear whether he is imposing an extra 10% on the 35% tariff on non-CUSMA compliant trade, or 10% on ALL trade whether compliant with CUSMA or not. I suspect it’s the former, which would equate to about a 1% effective tariff shock on the roughly 10% of exports to the US that are not CUSMA compliant. Other cautions include that we don’t know if the extra 10% would be layered on top of existing sectoral tariffs on metals and autos, or even if it will ever be implemented given Trump’s pattern of behaviour.

And as a reminder, all of these abused IEEPA tariffs might be swept away after the Supreme Court commences its review on November 5th. That too may limit a market response. A slew of high-profile economists including former Fed chairs Bernanke and Yellen plus N. Gregory Mankiw were among those signing submissions to the court against the tariffs by Friday’s deadline. The Court commences its review on Wednesday November 5th.

Regardless, Trump said this morning that he doesn’t wish to speak with PM Carney for “a long time” while Carney said the talks had progressed to be “very detailed, very specific” and that he is ready to resume negotiations when the US gets over it. Carney’s guidance suggests that whenever Trump calms down, the outlines of a trade and security agreement could be picked up where they left off. Carney advised that Canada is working toward a free trade deal with the Association of South-East Asian Nations by pitching Canada as a “reliable” trade partner in a shot at the US.

The “long time” feeling is likely to be mutual. Carney’s administration is hotly focused upon the budget next week on November 4th. The Liberal House leader Steven Mackinnon continues to advise that the minority government does not have enough votes at present to pass the coming budget. That could easily change, but trade negotiations are not issue #1 for Carney either at the moment.

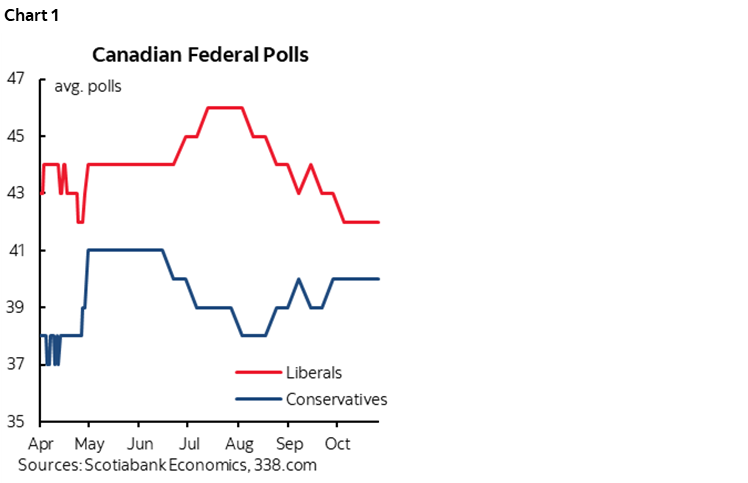

As for an election, it’s unclear whether it would reveal any different outcome than the one held on April 28th. Polls here and in chart 1 show the Libs barely have an edge over the Conservatives on average across the most recent polls and that not that much has changed since the April 28th election, although the latest one by Ekos may reflect voter sentiment toward some of the recent stumbles by the Conservatives. Anything can happen in an election, but my hunch is that Carney is better positioned to fight one.

VAGUE ‘DEAL’ TALK SPURS APPETITE FOR CHINESE EQUITIES

China’s main stock market benchmarks rallied by over 1% overnight on optimism toward limited trade progress with the US. Core issues appear to remain unresolved and there is no grand bargain coming out of a limited tee-up to a photo op when Trump and Xi Jinping meet. Agreements were announced on tariffs, export controls, possibly resuming Chinese purchases of US soybeans, shipping fees and fentanyl as Trump indicated the US would likely drop its investigation of China’s compliance with earlier agreements.

By now, most folks would fade a limited China-US deal given the pattern of escalation following limited reconciliation.

ARGENTINA’S MARKETS RALLY ON MILEI’S ELECTION RESULTS

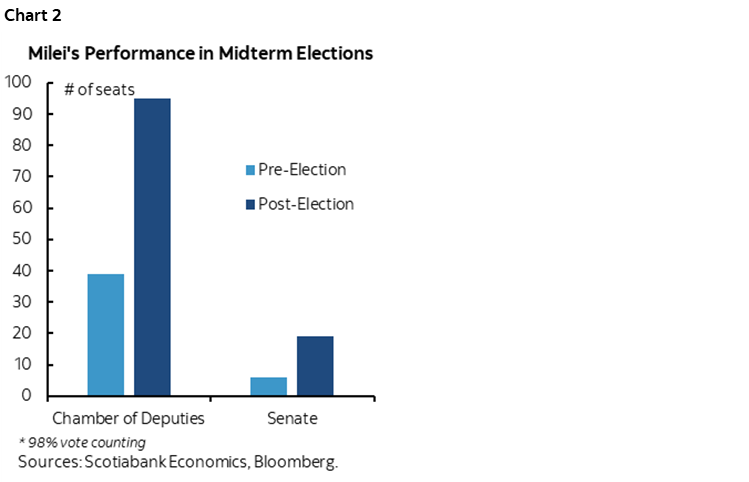

Argentina’s election results are likely to strongly buoy local risk assets today. President Milei’s party—La Libertad Avanza—won an estimated 41% of the vote versus about 32% for the Peronists and with most ballots counted, resulting in support from enough members to retain his veto power and advance reforms. It’s a major turnaround from the earlier defeat in September’s vote as Milei’s party marginally beat out the Peronists in Buenos Aires province this time. Chart 2 shows the magnitude of the victory.

LIGHT DATA

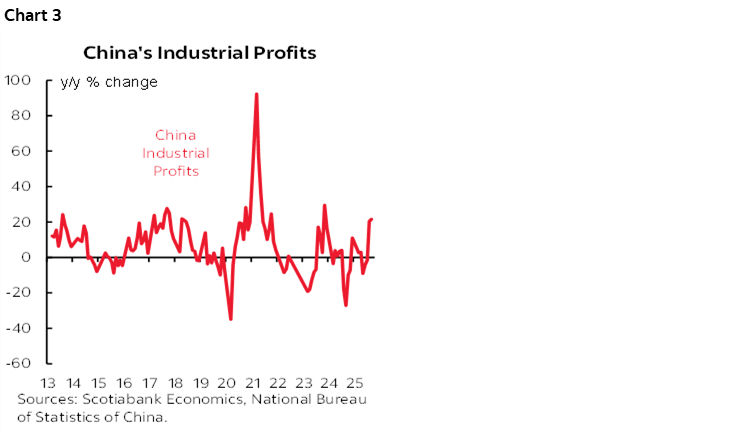

China’s industrial profits are hardly hurting from tariffs. They were up 21.6% y/y in September and 3.2% ytd. The y/y rate has been accelerating to the highest since late 2023 (chart 3).

German IFO business expectations climbed by 1.8 points to 91.6 in October. That’s the highest reading since early 2022.

We would have gotten US durable goods orders today if not for the ongoing shutdown. Given that Trump is away in Asia this week and weekend reports indicate no progress on talks, it seems likely that the October payrolls report that would have come out two Fridays from now is not going to be released until an undetermined time later.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.