ON DECK FOR TUESDAY, OCTOBER 21

KEY POINTS:

- USD gaining with bonds and equities little changed

- Canadian core CPI measures could make or break market pricing for the BoC

- BoC surveys and producer prices keep inflation risk alive in Canada

Forgive Canadian market participants if they’re looking a little bleary-eyed to tackle Canadian CPI this morning after the Blue Jays fabulous win.

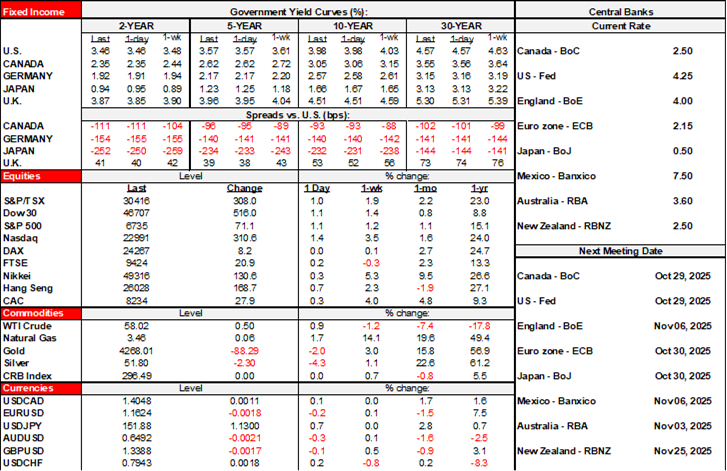

Global market movements are pretty small in the absence of significant new catalysts. Canadian equity futures are off by about ½% with US futures flat to slightly negative and Europe flat on balance. Sovereign yields are motionless across major benchmarks. The dollar is a bit firmer against most majors. Canadian CPI is the only notable calendar-based development after monthly UK public sector net borrowing largely met expectations, thereby avoiding a repeat of what happened to gilts and sterling the last time.

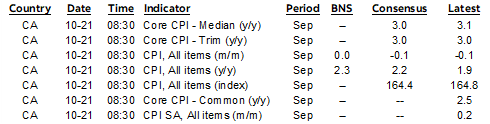

CANADIAN CPI COULD MAKE OR BREAK OCTOBER CUT PRICING

Canadian CPI arrives at 8:30amET. Governor Macklem emphasized the importance of the data to next week’s decision when he spoke at a media roundtable last Friday.

Estimates for headline CPI are all over the map from -0.3% m/m by the seasonally unadjusted polling convention to +0.1%. Scotia’s 0% is the consensus mode as it turns out. The median is -0.1% and the mean is similar. 0% m/m NSA would translate to a rise of about 0.4% m/m SA.

Base effects are likely to be the main driver behind pushing the year-over-year total inflation rate up to about 2.3% from 1.9% the prior month. It will remain weighed down by the elimination of the consumer portion of the carbon tax until next April.

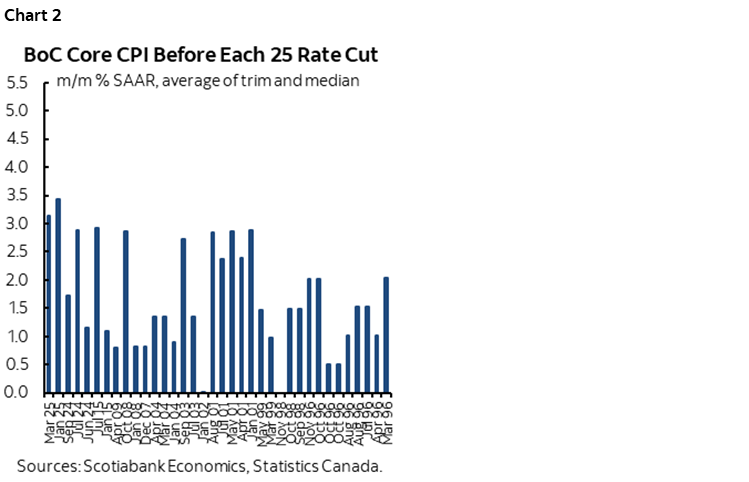

Key, however, will be the core measures. Something that extends the relatively soft recent pattern shown in chart 1 would keep the door open to a cut. A hot reading would dent October cut pricing. At the extreme, the BoC has never cut after trimmed mean and weighted median averaged 3½% m/m SAAR or higher and it’s uncommon for them to cut when those readings are in the 2¾% range (chart 2). A hot reading would present awkward optics for cutting.

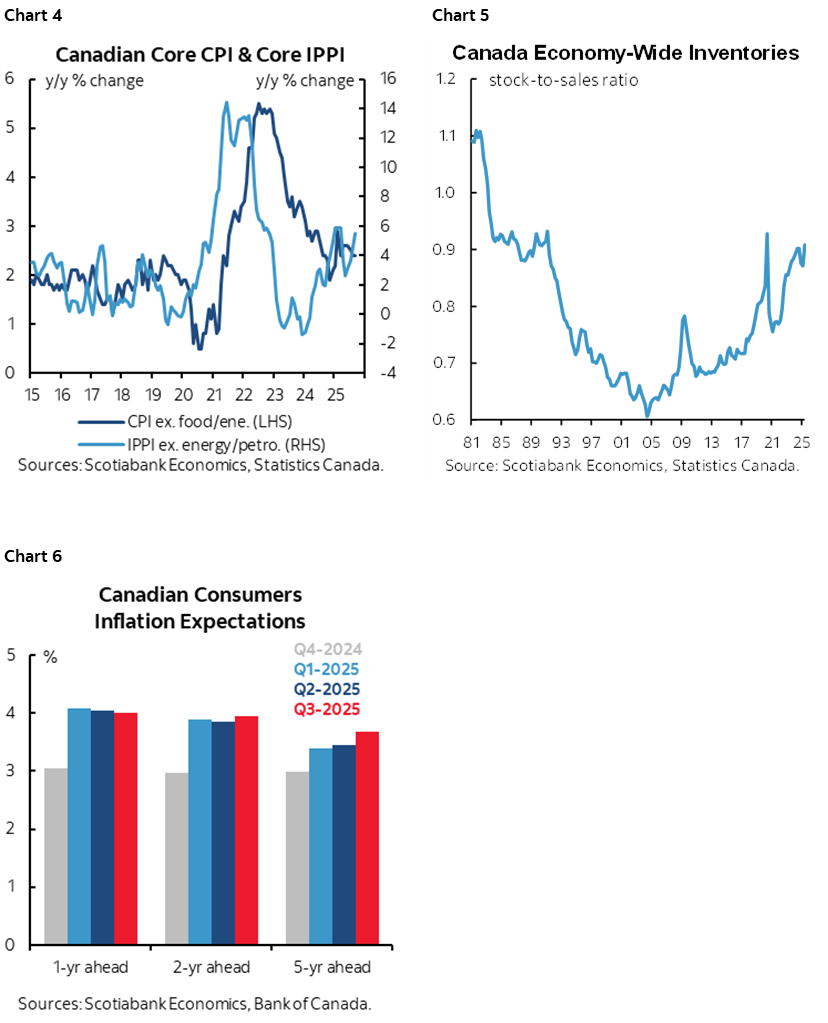

The dropping of Canadian retaliatory tariffs against the US on September 1st—except for autos and metals—should have little to no effect. For one thing, there wasn’t much of any discernible effect after they were applied, so there may not be much after their removal with one possible explanation being relatively high inventories at older prices (chart 3). For another, recall that measures of core inflation like trimmed mean and weighted median CPI exclude the direct effects of tariffs and other indirect taxes.

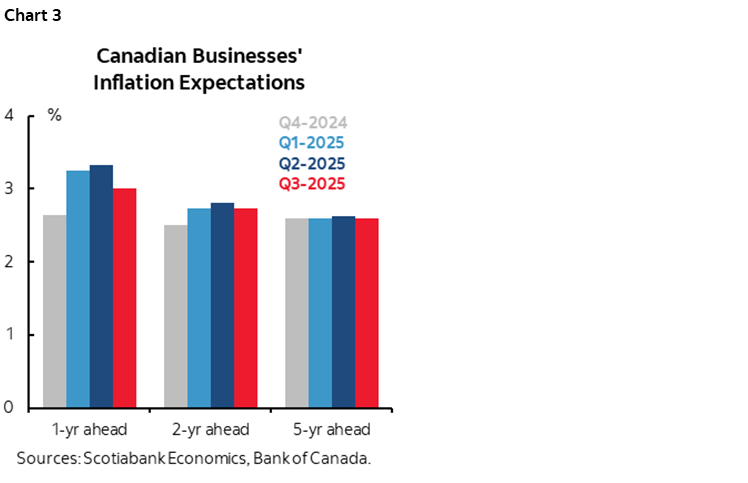

The other readings we obtained yesterday show that inflation risk is hardly benign in Canada. The strong gains in producer prices offer renewed pass through risk into CPI given historical connections (chart 4). Measures of consumer and business inflation expectations in the BoC’s quarterly surveys remain sticky (charts 5, 6). Business inflation expectations are higher in the short-run than the long run but even the long-run is in the upper half of the 1–3% inflation target range. Consumers’ inflation expectations are above the top end of the 1–3% inflation target range across all horizons. That said, I have little faith in any of these measures.

See my weekly for a fuller preview including discussion of other factors weighing on the BoC’s upcoming decision.

As for whether this reading should matter in the face of more complex and longer-run drivers of inflation, well, that’s another story. I’m still of the view that long wave upward pressures on costs and prices pose persistent upside risk to inflation in Canada.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.