ON DECK FOR THURSDAY, OCTOBER 2

KEY POINTS:

- Bad news is good news to equities—for now

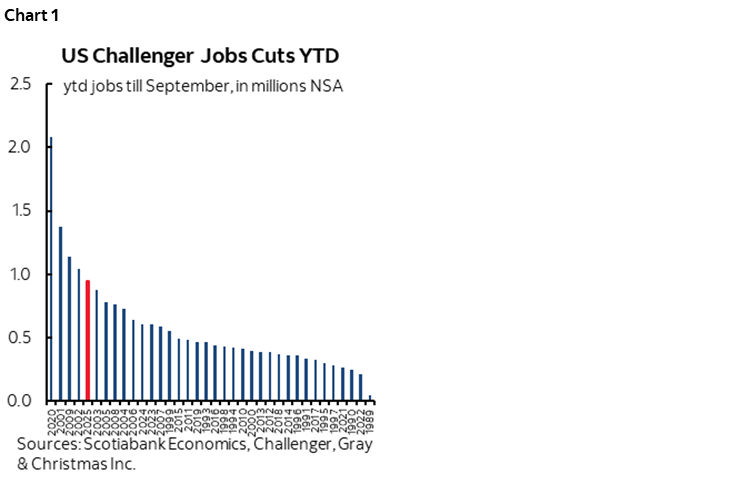

- US job cuts are at their highest since 2020, 5th highest in 36 years…

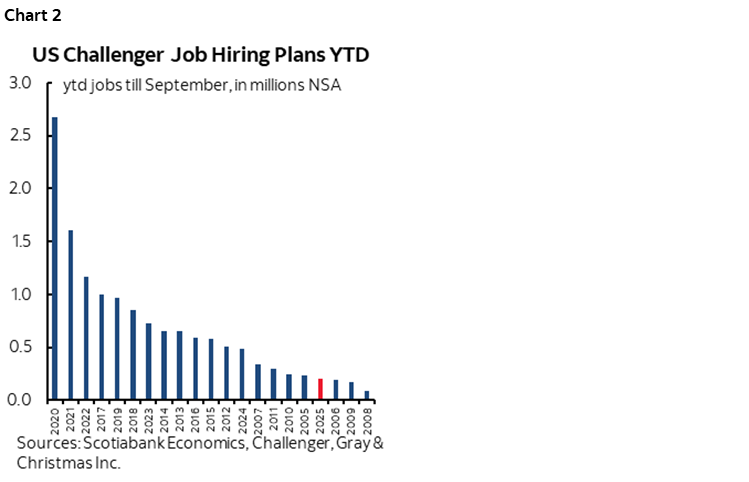

- …while US hiring plans are at their weakest since 2009…

- ...amid a combination of drivers affecting both figures

- What yesterday’s ADP says about nonfarm’s prospects

- Are Wall Street’s MAGA rhetoric and fear clouding its judgement over payrolls?

- How the shutdown could affect US payrolls and unemployment in October

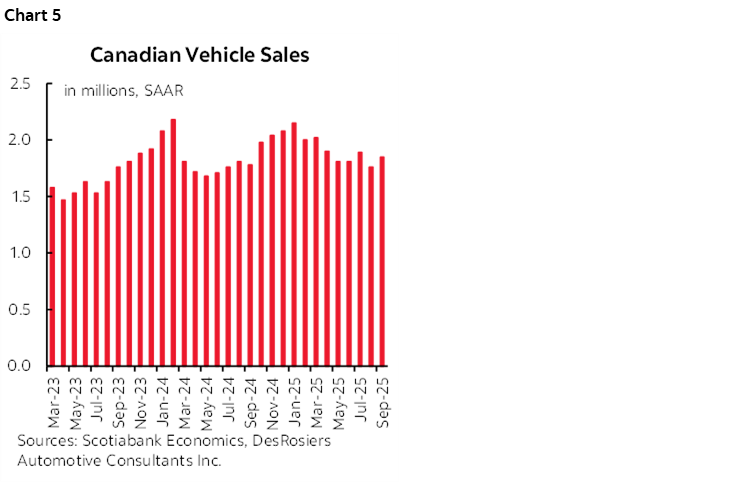

- Canadian vehicle sales jumped higher in September

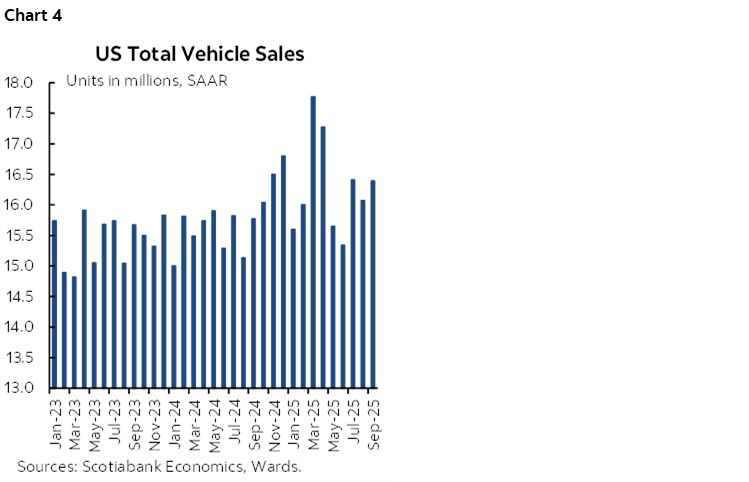

- US vehicle sales grew temporarily on expiring EV credits

- US claims and factory orders won’t be released today because of the shutdown

Equities are broadly bid and led by European exchanges this morning. US equity futures are gently higher, sovereign bonds are treading water and currencies are mixed to the dollar with the C$ and MXN among the weakest crosses. There are few fresh catalysts beyond equities becoming jubilant over a deteriorating US job market given yesterday’s ADP and this morning’s Challenger report. The figures may embolden Fed easing and hence equities for now, unless the economy stumbles.

US JOB CUTS SOARING, HIRING PLUMMETING

Challenger job cut announcements fell back to 54k in September from 86k in August. The figures are not seasonally adjusted but 54k is close to the ten-year average for like months of September. Job cuts tally about 946k so far this year, which is the highest year-to-date total since 2020, the fifth highest on record in the 36-year history of the data, and clearly on track for exceeding 1 million this year (chart 1).

Hiring plans are also way down this year and at their weakest since 2009 when the GFC was roiling markets and the economy (chart 2). Challenger reports that on a ytd basis, only 205k jobs were planned to be added this year, versus 484k last year, 726k in 2023 and 1.16 million in 2022.

Why is this happening? The answer has to be mixed given differential drivers of hiring and cuts. The cuts have nothing to do with tighter immigration policy and likely more to do with effects like federal government job cuts that account for a little under one-third of this year’s total cuts, concern over the outlook, the effects of AI on sectors like tech (108k cuts ytd) and the effects of tariffs that force cost cutting and emphasis upon higher productivity at least as the first-round responses before possibly raising prices.

As for hiring plans, I also doubt the role of immigration. ‘Plans’ connotes a wish to hire regardless of the ability to do so that would be impacted by immigration. Perhaps employers realize they’ll find it difficult to find labour and so hiring plans are adjusting lower. It’s likely that hiring is cooling for some of the same reasons as job cuts are rising.

WHAT ADP MAY BE INDICATING FOR NONFARM PAYROLLS

US ADP private payrolls fell by -32k (51k consensus) in yesterday's release for September. That’s the second drop after June's which was the first since July 2020.

Statistically speaking, there is around a one-in-five chance that ADP private payrolls would be this far beneath consensus for nonfarm private payrolls (presently 65k, total payrolls 52k, Scotia –20k) or even further below. That’s based on the spread between initial pre-revision estimates for ADP and initial pre-revision estimates for nonfarm payrolls, since it’s the initial prints we’re focused upon this week (chart 3).

If we eliminated the data from the wild pandemic years of 2020–21, then the probability that ADP comes in this far beneath consensus expectations for private nonfarm payrolls or by more drops to about a one-in-ten chance instead of about one-in-five.

Ergo, while ADP is wonky and often highly misleading as a guide to nonfarm partly because of different methodologies and samples, the unfiltered probabilities would indicate a high probability that nonfarm will come in lower than consensus. Who knows where nonfarm will actually land, but I’m surprised that I’m the only negative in consensus. Maybe that’s because the pitch on the American economy gets in the way on Wall Street.

According to ADP, it's small business that is taking it on the chin and there was high breadth to the losses by industry. Large employers with payrolls over 500 employees added 33k jobs, which is still soft. All categories of smaller employers lost between about 10–20k jobs last month. Small business would be expected to take the bigger hit from misguided US economic policies including tariffs and over-correcting on immigration policy while driving uncertainty through the roof.

HOW THE SHUTDOWN COULD AFFECT US PAYROLLS AND UNEMPLOYMENT

How will the US government shutdown affect October payrolls and the unemployment rate when they are released in November? That could be more uncertain this time.

Since the law changed in 2019, if workers are furloughed for the entire nonfarm reference period (the pay period including the 12th day of the month) and the entire household survey reference week (the calendar week including the 12th day of the month), then they are kept on payrolls because they expect to receive back pay but the household survey treats them as unemployed. So, payrolls wouldn’t adjust but the UR could spike.

Key, however, is the expectation that the workers would receive back pay. If instead a significant number of them are fired, then they’d be expected to drop off payrolls absent backpay. Using the Census Bureau’s estimate of the number of furloughed employees that would see a cap of about 750k as the hit to payrolls and the UR if they’re all fired. That’s hard to imagine imo, so treat according to what you think may be likely and to be informed by next steps. Seems entirely callous, vindictive and mean-spirited to me.

Slick Speaker Johnson’s interviews reinforced his support for mass firings. Vance also pivoted somewhat in this direction yesterday. OMB’s Vought did so as well and of course the always divisive President Trump is on board. There’s a whole lot of dirty pool being played. Making workers with bills to pay suffer from a purely political spat is callous, mean-spirited and a failure of leadership.

US VEHICLE SALES RISE TEMPORARILY

US vehicle sales in September landed at 16.4 million SAAR late yesterday (consensus 16.2, Scotia 16.4) for a 2% m/m SA rise (chart 4). That would contribute about ¼% to retail sales growth when we get September’s numbers on October 16th, assuming that the shutdown is over by then.

US vehicle sales are likely to plummet this month. That’s because a major driver in September and prior months was the rush to buy e-vehicles before the Trump administration’s cancellation of the federal EV tax credit. This effect clouded the possible effects of tariffs. Those EV sales are likely to fall sharply in October after a pulled-forward effect, in addition to whatever effect there may be from the net impact of tariffs on non-EV vehicles and incentives.

US weekly claims and factory orders won’t be available today because of the shutdown.

Washington is full of hotheads these days, so further escalatory shutdown tactics are possible including putting a number on how many federal workers to “imminently” fire as well as possible conditions and details.

CANADIAN VEHICLE SALES JUMPED IN SEPTEMBER

It's also looking like Canadian vehicle sales jumped by about 5% m/m SA in September according to Desrosiers (chart 5).

Despite tariffs, they've been trending at a relatively stable rate since May. One reason could be substitution toward vehicles made in Canada and imported from Europe and Asia that are not subject to the bilateral tariffs on vehicles between Canada and the US after the US started the global trade war. Perhaps Canada doesn’t need your vehicles, America.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.