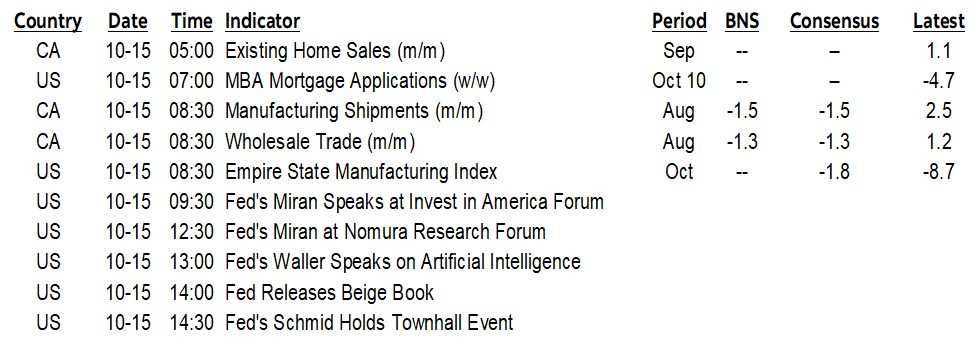

ON DECK FOR WEDNESDAY, OCTOBER 15

KEY POINTS:

- Stocks and bonds rally, USD falls

- Government debt is lifting Chinese financing…

- …as core domestic currency loan growth continues to ebb

- China is still not in generalized deflation

- US bank earnings continue to beat on Trump-driven volatility and fearful analysts

- Canada to refresh minor gauges

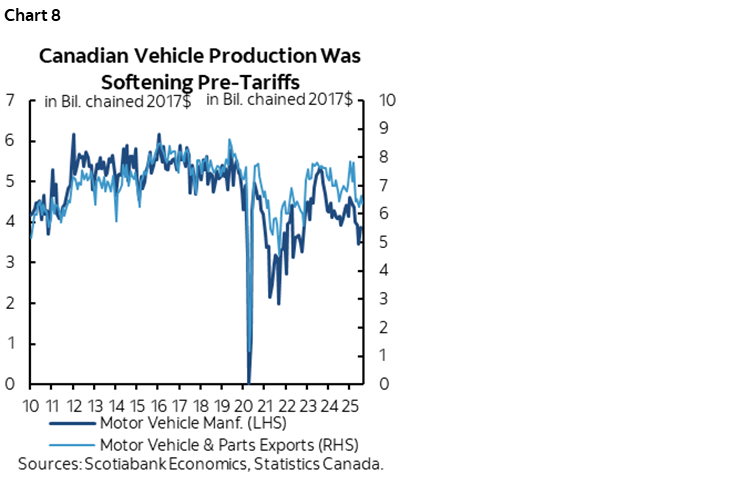

- Canada’s auto sector was in decline before Trump

- Light US data on tap

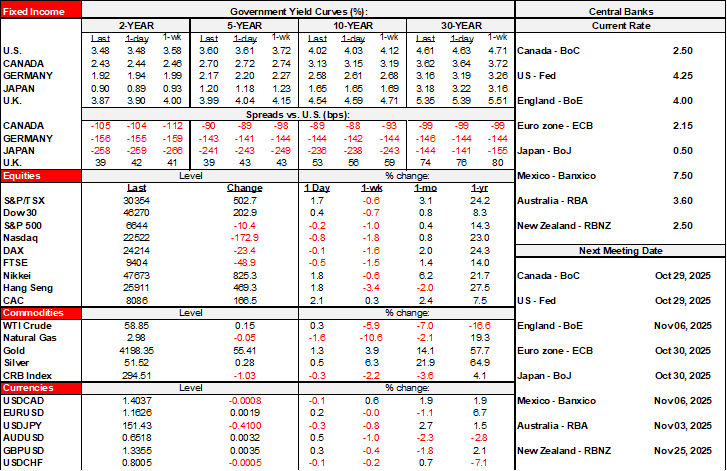

The focus will continue to be on pending US bank earnings (BofA, Morgan Stanley) and limited macro data primarily focused on China. Stocks are in the black with US and Canadian equity futures up by over ½% while France’s 2½% gain is leading on perceptions that political risk is subsiding as the second-time around for Macron’s choice of PM sailed through. Sovereign bonds are generally bid again with gilts outperforming. The dollar is broadly retreating.

US BANK EARNINGS CONTINUE

More US bank earnings beats arrived in the pre-market (chart 1). Bank of America beat expectations with Q3 EPS of US$1.06 (consensus $0.95). It also posted broad revenue beats. Morgan Stanley also beat expectations with Q3 EPS of US$2.80 (consensus US$2.11) and broad revenue beats.

Either US banks are resilient and have capitalized upon the market volatility driven by the Trump administration, and/or this is merely an extension of the serial pattern of low balled analyst estimates since SOX legislation and other developments.

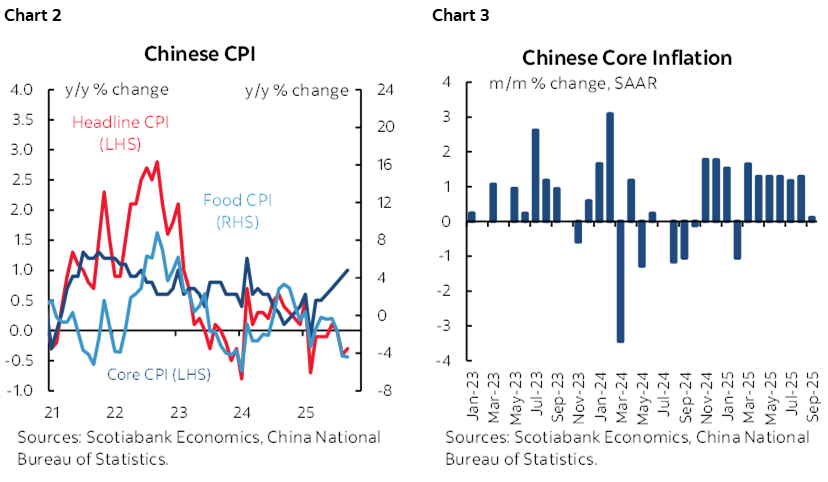

CHINA STILL FALLING SHORT OF BROAD-BASED DEFLATION

China’s CPI landed at -0.3% y/y in September and has been slightly below zero in six of the nine months to date. Core CPI was 1% y/y which is the highest since February 2024 (chart 2). Chart 3 shows month-over-month core CPI that ebbed in September after a string of six consecutive gains of around 1% m/m SAAR. In general, commodities are dragging down inflation led by a 4.4% y/y drop in food prices. China is primarily experiencing a relative price shock, not generalized deflation.

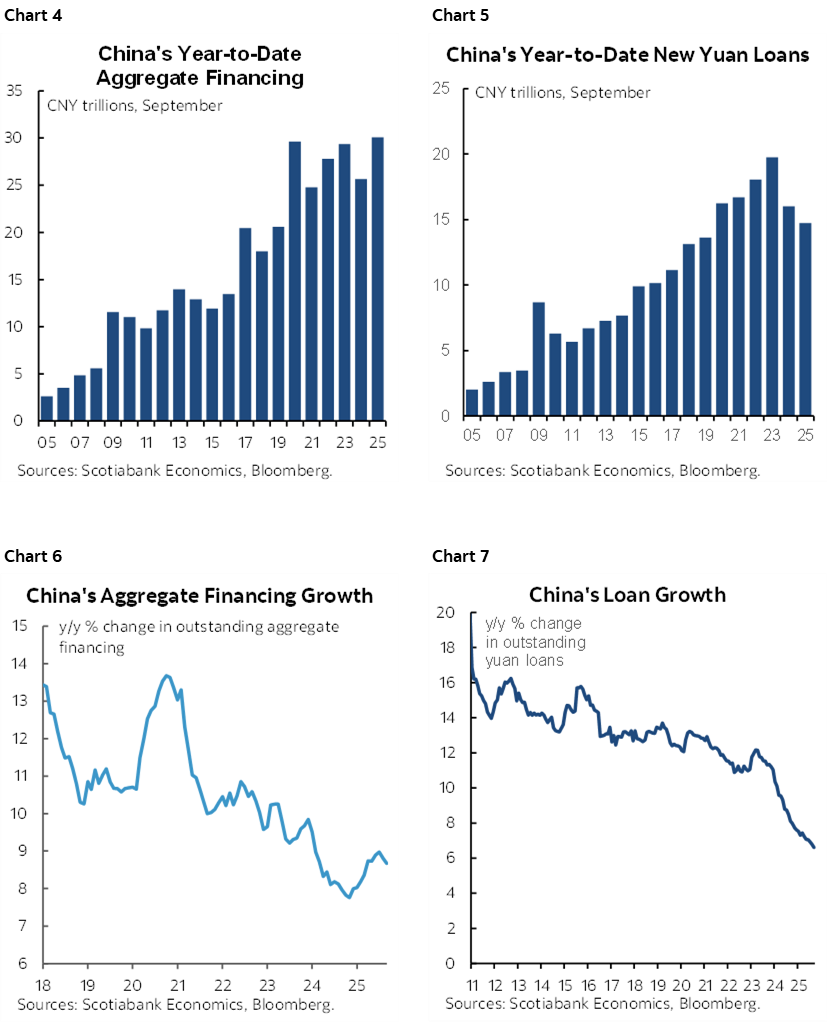

CHINESE FINANCING MASKS WEAKNESS

China’s financing figures for September were roughly in line with expectations. Aggregate financing originations ytd are at a new record high (chart 4), but core domestic currency loan origination is running at a six-year low in ytd terms (chart 5). Government bond issuance has surged to a record high this year. Outstanding aggregate financing is growing by 8.7% y/y (chart 6) while yuan-denominated loans are growing by 6.6% y/y which is the weakest since 2000 (chart 7).

MINOR GAUGES ON TAP

US data releases will be light. Mortgage applications slipped by –1.8% w/w last week. The NY Fed’s Empire manufacturing gauge for October kicks off the march of the regional measures toward the next ISM-manufacturing print (8:30amET). The Fed’s Beige Book of regional economic conditions and anecdotes will be released at 2pmET.

Canada updates some minor releases that are expected to be weak given advance guidance. Both manufacturing and wholesale sales were previously guided to have fallen by just over 1% m/m SA in nominal terms with revision risk and details like volumes and orders of interest (8:30amET).

The decision by Stellantis to pull up the tent stakes in Canada and relocate some of its production to the US highlights the impact of US auto tariffs, but let’s face it, the sector was already in decline before DJT bullied his way through. Difficult choices face Canada in providing support to a sector that is generally in decline. Chart 8 shows that the peak for manufacturing sales of autos and parts and exports of autos and parts. On its own this is a limited impact to the economy, but it has the potential to be larger. The US states have long siphoned off auto production from Canada with generous subsidies to locate there, and now the tariff wall may amplify this trend. The longer-run consequences may be higher costs, higher prices, less innovation, and less loyalty to US brands abroad. The potential response of Canadians could well be to shift demand to other US models that are still made in Canada, and to Asian and European cars and trucks.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.