ON DECK FOR WEDNESDAY, OCTOBER 1

KEY POINTS:

- US risk appetite softens as Washington’s ineptitude shuts government

- The US is clearly unserious about CUSMA negotiations

- US nonfarm payrolls are very likely to be suspended

- Today’s US private data is on track…

- …including ADP, ISM-mfrg and vehicle sales

- Eurozone core CPI lands on the soft side of history

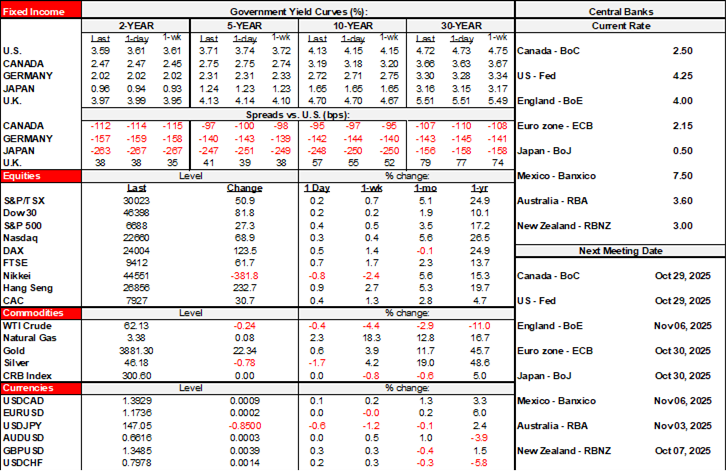

Washington’s bipartisan ineptitude has brought us yet another US government shutdown. US equity futures are underperforming with losses of about ½% compared to modest gains in Europe. US Ts are mildly outperforming at the front-end.

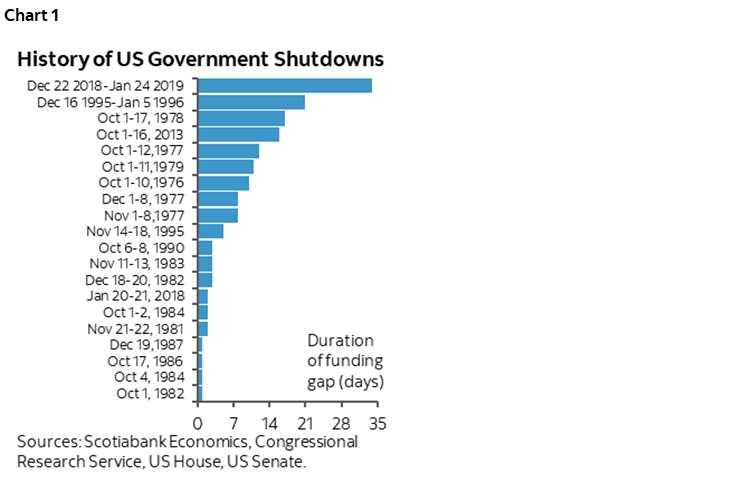

THE GOOD AND THE BAD OF THE US SHUTDOWN — SO FAR

Among the consequences to the shutdown is that US government data releases will be suspended and that’s likely to include Friday’s nonfarm payrolls given that neither side is likely to flex in time to strike a deal and reopen. The last time a shutdown was only two days long—which would be today and Thursday—was in 2018 and it’s a rarity to be so short (chart 1). In any event, time is needed to restore functions after a shutdown.

The Trump administration used the shutdown as cover to pull the nomination for BLS head by the thoroughly unqualified EJ Antoni, so I guess we can say that some good can come from shutdowns.

TODAY’S US DATA RELEASES WILL BE MOSTLY INTACT

On tap for today will be US ADP private payrolls (8:15amET, 50k expected), ISM-mfrg (10amET, 49.0 consensus, 48.5 Scotia) and US vehicle sales (e.o.d., 16.2 million consensus, 16.4 Scotia) since they are all released by private sources. Construction spending is released by the Census Bureau and so it’s suspended.

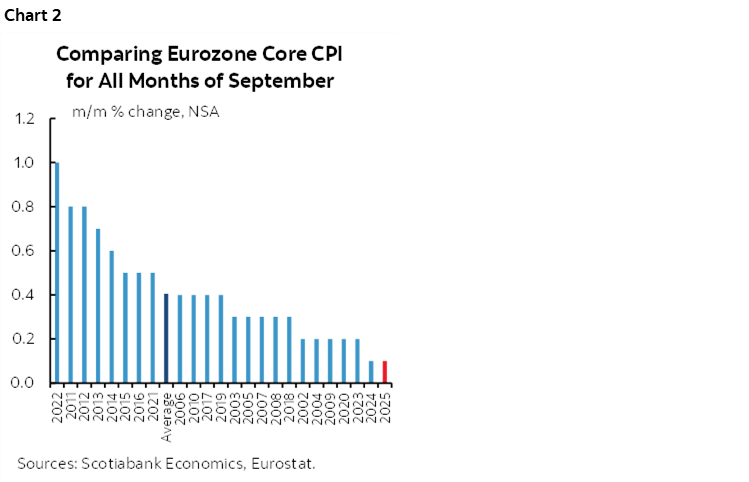

Markets paid little heed to overnight developments. Eurozone CPI offered little surprise given a) individual countries release in advance, and b) core CPI was in line with expectations at 2.3% y/y. Core CPI at 0.1% m/m NSA wasn’t much of a stand out compared to prior seasonally unadjusted figures for months of September.

Japan’s Tankan report was also in line with expectations.

WASHINGTON’S UNSERIOUS ABOUT CUSMA/USMCA NEGOTIATIONS

Canada updates the S&P manufacturing PMI for September this morning (9:30amET). More important are the signals from Washington that it isn’t approaching CUSMA/USMCA trade negotiations with any seriousness. Trump’s additional tariff announcements since last week including another levy on softwood lumber combined with his resurrection of 51st state insults to my nation continue to signal amateurish belligerence and American isolationism.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.