ON DECK FOR THURSDAY, NOVEMBER 6

KEY POINTS:

- Markets playing light defence

- US job layoffs soar...

- ...and ADP faces revision risk

- BoE, BCB, Negara and Norges all held...

- ...but Banxico is expected to cut

- Ontario's budget coming today

- Light overnight macro readings

Markets are playing light defence this morning. Sovereign yields have a slight downward bias across major benchmarks in the US, Canada and Europe. Key is further evidence that the US labour market's warning signs are flashing red.

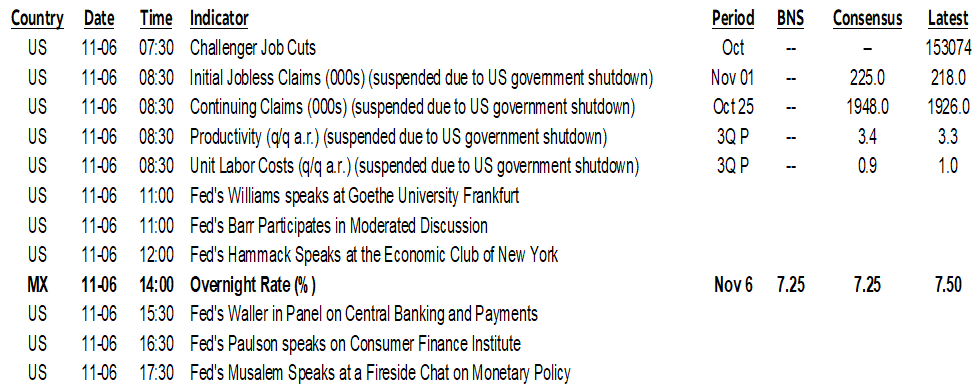

US JOB CUTS SOAR, ADP FACES REVISION RISK

US Challenger job cuts soared to 153k in October. That's even higher than I had expected above 100k given announcements toward the end of October from companies like Amazon, UPS and other tech firms. That raises the ytd tally to about 1.1 million which is only exceeded by crisis points like the dot-bomb, GFC and the pandemic. Hiring is also slow. Charts 1 and 2.

It also indicates that ADP's rise of 42k in October may be subject to downward revision. ADP's reference week is the week that includes the 12th of each month. Since the biggest layoffs were at month end this was not yet captured. It still may not be if the pink slips don't show up on payrolls that quickly in which case the next report is likely to be quite weak.

CENTRAL BANKS MOSTLY ON HOLD

The Bank of England held Bank Rate at 4% as widely expected but guided to expect a cut at the next meeting on December 18th. There were four dissenters who voted for a cut at this meeting while nevertheless cautioning that the MPC needs more evidence inflation is going their way.

Each of Bank Negara, Norges and Brazil held their policy rates unchanged as they expected at 2.75%, 4% and 15% respectively.

Round 2 of BoC parliamentary testimony occurs this morning (10:30amET). Round 1 was a yawner. They’re coming fresh off last week’s updated forecasts and clear guidance they are on an extended hold, but does the Budget affect their thinking at all? There will be repeated written testimony and then scintillating banter with parliamentarians.

Banxico is the only one that is expected to cut again this afternoon (2pmET). See my weekly for more.

LIGHT OVERNIGHT RELEASES

Japanese real wages are still falling by -1.4% y/y as at September.

German industrial output recorded a more tepid rebound than expected in September. The rise of 1.3% m/m fell well shy of the 3% consensus and followed a -3.7% m/m drop in August (revised from -4.3%).

Sweden's krona is a class leader after stronger than expected CPI. October's reading was 0.3% m/m, tripling consensus and landing at a still modest 0.9% y/y. Underlying inflation ex-energy was 2.8% y/y (2.6% consensus).

ONTARIO TO RELEASE BUDGET

Ontario releases its budget shortly after 1pmET today. Our two provincial economists will be covering and will send a note out by the evening. Here's what John Fanny and Mitch have to say about it.

The province’s 2024–2025 Public Accounts show a much smaller deficit of -$1.1 bn in FY25 (-0.1% of nominal GDP) compared to what was expected in the spring budget (-$6 bn, -0.5%), providing a stronger hand-off to the current fiscal year. In Ontario’s Q1 fiscal update, the deficit for FY26 was unchanged from Budget 2025 at -$14.6 bn (-1.2% of nominal GDP) but could change in the fall fiscal update. Ontario has already announced that it will include in its mid-year update an expansion of its GST rebate on new homes, to fully refund the 8% provincial portion of the HST for first-time homebuyers. This is a fairly narrowly scoped measure, which should be able to be absorbed with Ontario’s considerable forecast buffers that included $5 bn allocated for contingencies and reserves (2.3% of revenue) in FY26. Meanwhile, the economic backdrop for this year is proving more resilient than feared at the beginning of this year. The 2025 nominal GDP growth forecast in the Q1 fiscal update was 3.2%, marginally higher than 3.1% in the spring budget but below our September outlook of 3.5%.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.