ON DECK FOR TUESDAY, NOVEMBER 4

KEY POINTS:

- Risk-off sentiment greets Canadian Budget Day

- Canadian Budget Preview—Prepare for Fairy Tales

- Trump’s government shutdown is now the longest ever

- US Challenger layoffs could hit the highest since dot-bomb, GFC and pandemic eras

- The dip in US vehicle sales will weigh on retail sales whenever we get them

- Canadian vehicle sales rise to highest since before Liberation Day

- Takeaways from Macklem’s pre-Budget appearance

- RBA holds with neutral-hawkish bias

- NYC’s mayoral election results today, additional votes in N,J., Virginia, California

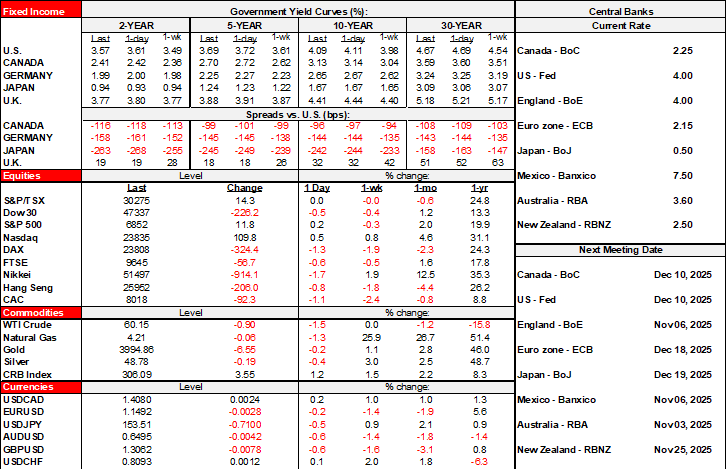

Markets are shedding risk appetite this morning. US equity futures are down by about 1% and European cash markets are performing similarly after Asian equities sold off. Sovereign bond yields are slightly lower across major global benchmarks, except underperformance in Australia post-RBA. The dollar and yen are broadly firmer. Gold is not benefiting.

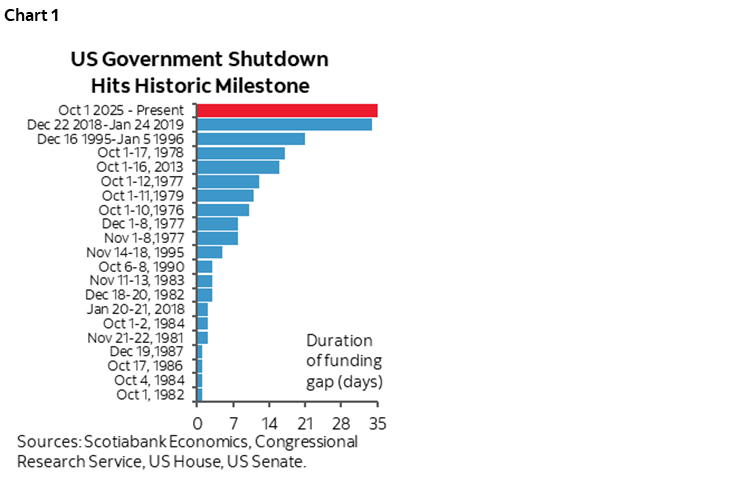

Why? It started with the FOMC’s stance last Wednesday that cast doubt upon further easing in December. Earnings from an AI star—Palantir Technologies—disappointed markets. Some Wall Street CEOs are emphasizing a need for caution. Only now? Valuations have been super rich for a long while. Flying blind on US macro data isn’t helping things as the swamp sets a fresh record for the longest government shutdown on record (chart 1).

All of which sets an appropriately negative market tone for Canada to present a Budget narrative that posits the world has changed for the worse.

BUDGET DAY IN CANADA

The main event for many of us will be Canada’s federal budget that gets released after today’s market close (>4pmET). Everyone’s got a preview including several from Scotia that were all signed off and that judge outcomes, risks and alternatives through a variety of lenses. Read them all in apolitical fashion as there are nuggets in each of them. Mine’s here as a large feature in the Global Week Ahead and it combines high caution around anyone’s views with doubt over the likely chosen approach with emphasis upon market risks over time.

I’ve consistently argued all year long that the street’s estimates of the current year’s budget deficit and issuance needs have been grossly understated by tens of billions. As those estimates crept higher to present readings they may still be understated, but so what, the issue isn’t this year. So not this year. And it’s not just the on-book deficits that matter.

It’s the overall plan for the next five years and more importantly the likelihood that any numbers for deficits and issuance that are put down on paper will be a fairy tale. Apply even wider than normal brackets around this year’s projections. And supplement with strong attention paid to off-budget items like loans, guarantees and equity positions that add to financing requirements.

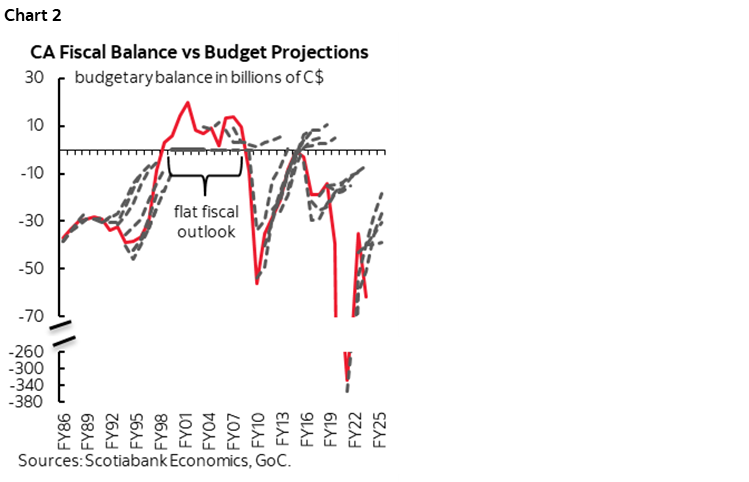

Nobody can forecast deficits as evidenced by Ottawa’s own track record that is routinely off by large amounts and misses inflection points. The only chart you need to pay attention to as the Budget looms is chart 2. They always show a path back to balance and understate deficits. Relying on those numbers for issuance estimates is pure folly, by now the street should know better, and that’s especially so now. We’re in uncharted waters now for reasons given in my weekly.

Why are budget projections so bad? Perhaps for several reasons:

- the underlying macroeconomic projections turn out to be wrong;

- the assumed fiscal sensitivities to the macroeconomic projections were incorrect;

- plans change along the way for political and expedient purposes;

- there is a political bias to show a path toward better fiscal stewardship;

- there is no accountability for wrong forecasts produced by governments like there is if a company routinely misleads investors;

- the desire to sell debt to investors overwhelms forecast objectivity.

RBA HELD WITH NEUTRAL-HAWKISH BIAS

Australian rates crept slightly higher overnight, led by a 2-3bps rise in the two-year yield while most other global benchmark yields are slightly lower this morning. The catalyst was a mildly hawkish sounding RBA (here and here). The RBA left its cash rate unchanged at 3.6%as all but one out of thirty-four forecasters anticipated and that was priced going in.

Guidance through the overall suite of communications indicated that a cut was not even discussed and that the policy rate may or may not be reduced in future. The statement said there is a “little more” core inflation than expected. The RBA’s forecasts downgraded future implied easing to one more cut in 2026H1 instead of two in its last forecast.

DATA SUSPENSIONS IN US, CANADA

Unfortunately the US government shutdown means we won’t get any US or Canadian trade data for September that was otherwise scheduled for release today. Ditto for US JOLTS job vacancies etc, and US factory orders.

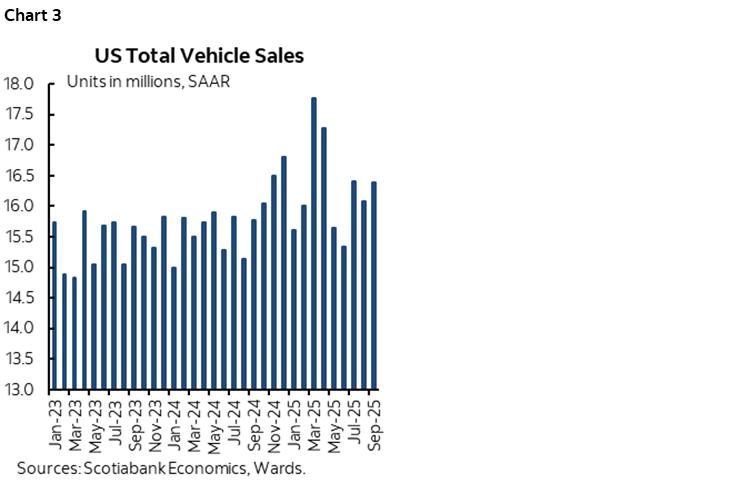

US VEHICLE SALES POINT TO SOFT RETAIL SALES

October US retail sales are tracking softly whenever we get them along with backed up September figures. That’s partly because US vehicle sales landed at 15.3 million SAAR in October (chart 3). Consensus expected 15.5, Scotia’s estimate was 15.0, and the prior month was 16.39. That's a drop of -6.5% m/m SA. The expiration of EV tax credits on September 30th was the main culprit as sales were brought forward.

Combined with tracking of higher new vehicle prices in October, the result is that new vehicle sales should subtract about -0.7% from m/m US retail sales during October whenever we get them. Gasoline prices will shave about -0.1 to -0.2% off monthly retail sales. Combined, new vehicle sales in dollars plus gas prices will knock an estimated -0.8 to -0.9% off m/m retail sales which means that even if core sales post a modest gain, the headline is likely to fall.

CANADIAN VEHICLE SALES HIT A SEVEN-MONTH HIGH

Canadian new vehicle sales hit the highest level since March last month according to Desrosiers. They landed at about 1.94 million SAAR, up by just under 5% m/m SA (chart 4). Take that, tariffs! It could be that inventories and incentives are helping to offset tariffs. Or it could be evidence that tariffs divert trade toward imports without tariffs. Either way, that's not an option in the US that applies tariffs against everyone's auto imports but especially from Asia and Europe.

US CHALLENGER JOB CUTS COULD BE HIGHEST SINCE CRISIS POINTS

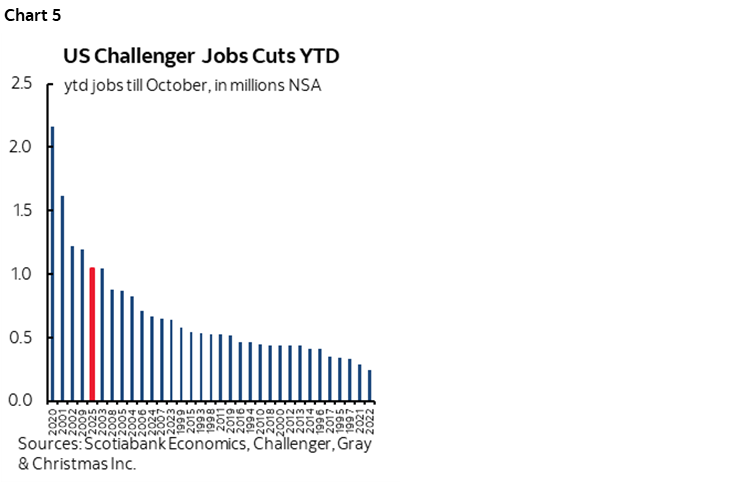

Thursday's US Challenger layoffs could land around 100k for October, maybe even higher. That’s based on a reasonable average for what’s seasonally normal since it’s seasonally unadjusted data, plus major layoffs at select companies (Amazon, UPS, Target etc) and a rough tally of layoffs at smaller tech companies.

That would push the ytd tally to about 1.05 million. The only years higher than that would be 2020 (pandemic), 2001–02 (dot bomb), and 2009 (GFC). See chart 5.

Hiring is more likely to be affected by no population growth via tighter immigration but that’s not really the case for layoffs except indirectly and which are more likely reflecting underlying challenges adapting to uncertainty, tariffs, pressure to offset higher costs via productivity, and tech change. But don't worry, everything's a.o.k. in the economy.....ignore the lagging effects....it’s only GDP and its various distortions that matters…

BOC GOVERNOR MACKLEM’S PRE-BUDGET TAKEAWAYS

BoC Governor Macklem’s fireside chat—sans fire—offered no materially new insights yesterday compared to his communications last week.

One question he was asked is why is everything still so resilient in the US economy after Liberation Day? Macklem emphasized the longer-term adjustments and the saving-investment imbalance in the US that will persist and pose long-term risks. imo, the answer could have also been a) not everything is (eg. jobs), b) there are lagging effects and distortions along the way as the overall balance of payments adjusts over time, c) trade diversion is going on, and d) the AI boom is masking other incompetencies. The ones saying everything is so resilient are highly myopic in their outlooks imo as the adjustments to protectionism and other policies will take years to unfold.

Asked why he's saying they're done, Macklem said:

- it's not a normal business cycle where growth goes down and back up

- this time it goes down and the level is lower

- productive capacity is being destroyed

- there are also additional costs, looking for new markets, developing new products, reconfiguring supply chains, and this all costs money.

- We've reduced the productive capacity and added costs which limits the powers of monetary policy while keeping inflation at the target.

In other words, Macklem is reinforcing the point about how potential GDP is lower. They revise their estimated PGDP growth rates once a year in the April MPR. As I've argued, today’s circumstances are both a demand and a supply shock as a more limited version of the pandemic shock. The BoC ignored the supply side the first time around. Once bitten, twice shy this time around.

Macklem did not comment on the role of fiscal policy in the decision to end cuts. He might on Wednesday and Thursday when he delivers post-Budget parliamentary testimony.

The curve has mostly heard him with nothing material priced until 50–50 bets by late Winter or early Spring. That’s still a touch rich, with no hike pricing further out (2+ years in OIS) which would be compatible with our projected future hikes over 2026H2. Canada 5s are rich.

NEW YORKERS VOTE TODAY

We should get the results of New York City’s mayoral election sometime after 9pmET tonight. Zohran Mamdani is heavily favoured in the polls. He has rolled out support from the Dems’ left wing factions including voices like Bernie Sanders and A.O.C.

Most economists would say that while Mr. Mamdani’s heart and intentions may be in the right place, his policies are not. He supports rent controls, minimum wage hikes, free transit that harkens back to the days after the Russian Revolution, and vague ideas to lower grocery prices. The voter base risks being fooled on the wisdom of such policies without even getting into the fears of the relatively well heeled who may turn further away from NY in favour of other parts of the US.

Key will be whether New York’s politics resonate nationally or push more voters away from the Democrats. We’ll see if the pundits look back in retrospect and wish the Dems had merely sailed up the middle. My hunch is that they missed the memo on voter frustration toward Biden and Harris.

A further test of this will come in elections to choose state governors in New Jersey and Virginia today and in California’s vote over whether to allow redistricting that could benefit the Dems in the midterms and 2028 as a counter to what Republicans have done elsewhere such as Texas.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.