ON DECK FOR MONDAY, NOVEMBER 3

KEY POINTS:

- A fresh week kicks off with risk-on sentiment

- US ISM-mfrg may remain in contraction…

- …as vehicle sales fall post-EV credits

- BoC’s Macklem unlikely to say anything new today…

- …but he might in his post-Budget parliamentary testimony

- CHF slips on weak Swiss CPI, but markets still lean against SNB going negative

- Why the world needs more Blue Jays

- Global Week Ahead — Everyone’s Doing It (reminder here)

A new trading week is off to a risk-on start. Equities are broadly higher across N.A. futures and European cash markets. Sovereign bonds are little changed. Most currency movements are small with the only slight stand out being a weaker Swiss franc after CPI landed weaker than expected (chart 1). Markets are still not pricing material odds that the SNB turns to negative rates in December or afterward perhaps because the franc’s appreciation until June has largely given way to a sideways trend since then. Other overnight developments were very thin with only minor releases ahead of light US data.

COOLER US DATA ON TAP

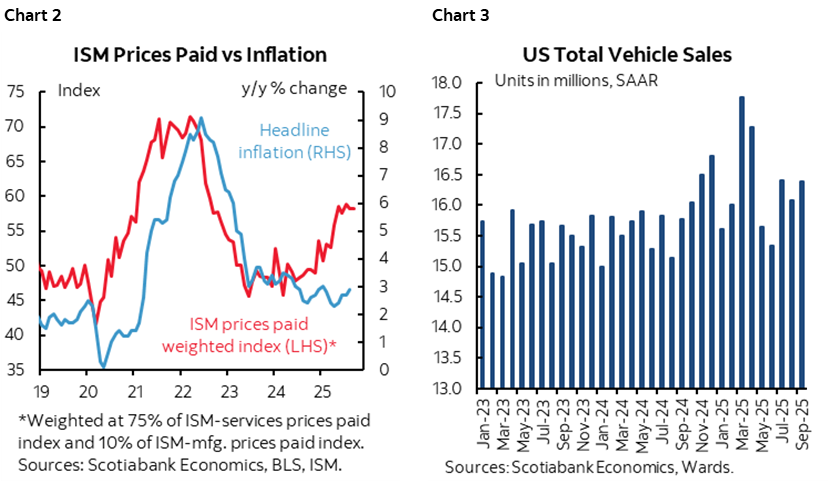

A pair of second and third tier US macro releases is on tap. ISM-manufacturing has been in contraction for seven months judging by the headline reading and October could add an eighth (10amET). Watch the prices gauge that when combined with the coming ISM-services-prices measure serves as a leading indicator of future inflation (chart 2). We won’t get construction spending because of the government shutdown. US vehicle sales are expected to sharply fall in the first full month after the expiration of EV credits (e.o.d.). Chart 3.

BoC’S MACKLEM MAY NOT SAY ANYTHING NEW—UNTIL POST-BUDGET PARLIAMENTARY TESTIMONY

Canada updates S&P’s manufacturing PMI that rarely gets much attention (9:30amET).

Then BoC Governor Macklem participates in a fireside chat (1:30pmET) but it’s hard to imagine him saying anything materially different from last Wednesday’s communications. On GDP, he’s likely to say their forecasts are on track as argued here.

That difference might arise when he delivers two rounds of Parliamentary testimony on Wednesday and Thursday after Tuesday’s federal Budget. He is sure to be grilled by MPs about what the BoC thinks will be the Budget’s impact. He might simply say they’ll wait until it’s passed and fully incorporate its effects in the next forecasts in January and perhaps offer limited views beforehand. Nevertheless, the clear message from the BoC’s communications last week was that they are done for the foreseeable future.

Canada might also update vehicle sales during October sometime today.

THE WORLD NEEDS MORE BLUE JAYS

Congrats to the Dodgers, you played well all season and won the World Series, though it was tight and could’ve easily gone the other way. Both teams gave us a fantastic series full of ups and downs in a close contest. Enjoy your parade and visit to the torn down White House.

But in my books, the Blue Jays were the true winners in terms of character and the leadership examples they set. I’ll tell you what they won beyond the hearts of Canadians—the class contest, and for that, they and their supporters should be super proud.

Honouring a Dodgers pitcher who couldn’t be there due to a family emergency was top notch sportsmanship and pure class. Class and commitment were on full display by playing through obvious injuries and being there for the team (Springer, Bichette); what a great example for the kids to always try their best. Class was not having a manager who claimed he was being held up at the border for nefarious reasons, only to retract the claim when he realized the delay was due to US immigration. Not having at least a pair of headhunting pitchers out to injure opposing batters is what one should expect but sadly it was only the Jays who held to such standards. It wasn’t a Blue Jay stepping off the mound and gallingly mouthing disgusting profanities at the batter after one such occasion. Not being the ones to trigger a bench-clearing brawl with impressionable kids watching was class.

Class was getting to the World Series without lobbying the league to create the rigged Ohtani Rule which sets a double standard. Class was not jeopardizing the league’s future by abusing deferrals to spend billions and buy two championships that some think could be the path to a lockout and lost season by 2027’s negotiations as other teams cry foul. Talk about abusing the intent of the league’s competitiveness framework while sacrificing the common good which is an all-too-common trait these days.

It’s all the type of class that is all too often missing these days among groups of lesser men including in leadership roles. The world needs more Blue Jays—they’d make it a better place during our divisive, spiteful, petty, excuse-riddled and corrupt times.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.