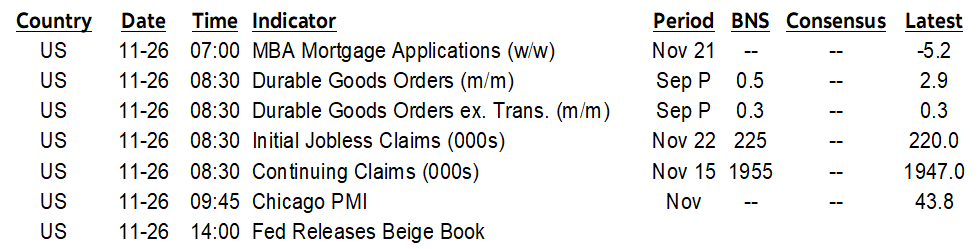

ON DECK FOR WEDNESDAY, NOVEMBER 26

KEY POINTS:

- Antipodean, UK markets in focus

- UK budget delivers major tax hikes, downgrades growth forecast

- Antipodean rates sell off, currencies gain…

- …after hawkish RBNZ guidance…

- …and higher than expected Aussie CPI

- US claims, durables, Beige Book on tap, then markets largely shut

- America’s love of subsidies extends to data centres

US market participants are about to head for the exits with an unofficial early close for many of them today ahead of tomorrow’s market closure for Thanksgiving and Friday’s early NYSE (1pmET) and bond (2pmET) closes. Basically kiss goodbye US liquidity for the rest of the week.

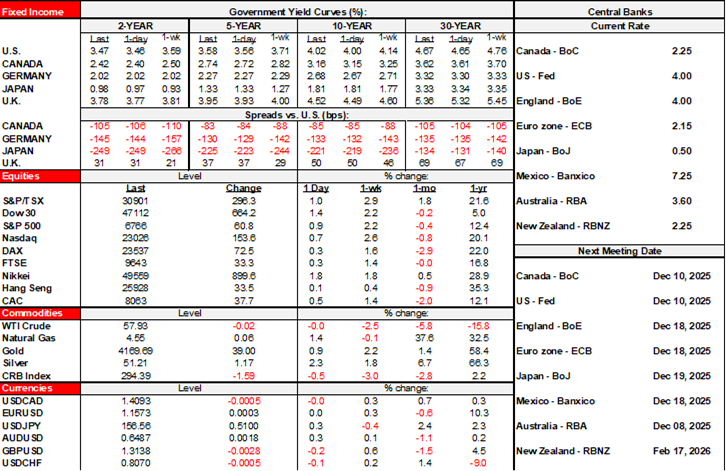

There is plenty else to consider. Antipodean rates sold off sharply overnight on a one-two punch from Australian inflation and hawkish RBNZ guidance. We’ll get some relatively minor US data today before eating and shopping take over.

Gilts and sterling have a close eye on what PM Starmer and Chancellor of the Exchequer Reeves will deliver in the Autumn Budget shortly.

UK Budget—Tax Hikes in Focus

The Starmer administration delivers its second budget shortly (7:30amET). The Chancellor of the Exchequer—Rachel Reeves—will deliver it. The first Budget was hardly a smashing success. The 10-year gilt yield jumped by 15bps on delivery. Sterling depreciated by about 1%. The FTSE100 fell by over 1%. The lack of a credible roadmap for the fiscal deficit, an additional £70 billion of annual spending, inflation concerns and a broken pledge that raised taxes on wealthier individuals and businesses wasn’t well received.

Perhaps much has been learned. Perhaps not.

The fiscal deficit to GDP ratio is well over 5% which is slightly wider than this time last year. No progress has been made to date toward reining in the deficit ratio. Debt-to-GDP has risen to about 94%.

Some headlines were already hitting as this note was being wrapped up. For one, the government will freeze tax brackets until 2030–31 such that pay hikes driven by inflation will bump more people into higher brackets and raise more money. Other tax hikes total an estimated 26 billion by £2029–30 according to the OBR including higher dividend taxes, and higher taxes on properties worth over £2 million. Gilts liked the headlines at first given implications for finances and debt issuance. Taxpayers and voters likely won’t.

Fervent speculation points to other possible ways of raising tax revenues such as adjusting the personal allowance, possibly freezing tax brackets such that income growth over time moves more earners into higher brackets and hence paying more taxes, and possibly raising taxes on investment income. Possible changes to pension rules are in the cards as well. Will Reeves implement a so-called ‘mansion tax’ on home sales above £1½ million? If so, then we share rather different definitions of ‘mansion’—especially in the London real estate market.

The market balance to be struck must lie between deficit restraint, expenditure restraint with a line-up of open hands outside of Reeves’ door, limited ‘soak the rich’ taxes that may harm growth and drive more of London’s wealthier individuals away after April’s changes that abolished non-domiciles, and not rocking the pension world given its status as large holders of gilts with memories of 2022.

If policies materially harm growth, then the gilts front-end may quickly look to how the Bank of England responds not only insofar as December’s expected cut is concerned but also beyond.

Updated Canadian GDP Tracking

Ahead of Friday’s numbers we have a bit more information to help with GDP tracking including preliminary readings for some indicators in October. September GDP was guided to grow by 0.1% which I bumped up a tick to 0.2%. October is looking weak and likely to post a drop. My best guess is that Q3 GDP overall is likely to barely grow by around ½% q/q SAAR and with hardly anything baked into Q4. October guidance has been quite soft across a range of readings.

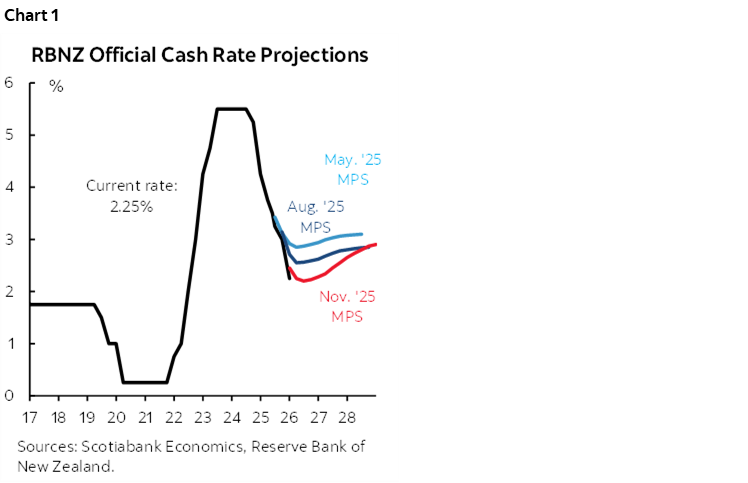

RBNZ’s Hawkish Guidance Drives Higher Rates

New Zealand’s central bank cut its policy rate by 25bps to 2.25% in a 5–1 vote as widely expected and priced. Guidance, however, crushed market pricing for any further easing and drove the NZD sharply higher. The updated explicit forward policy rate guidance showed no further changes to the policy rate over 2026 (chart 1). New Zealand’s curve bear flattened with the 2s yield up by about 8bps overnight while the NZ$ gained just shy of 1% to the dollar.

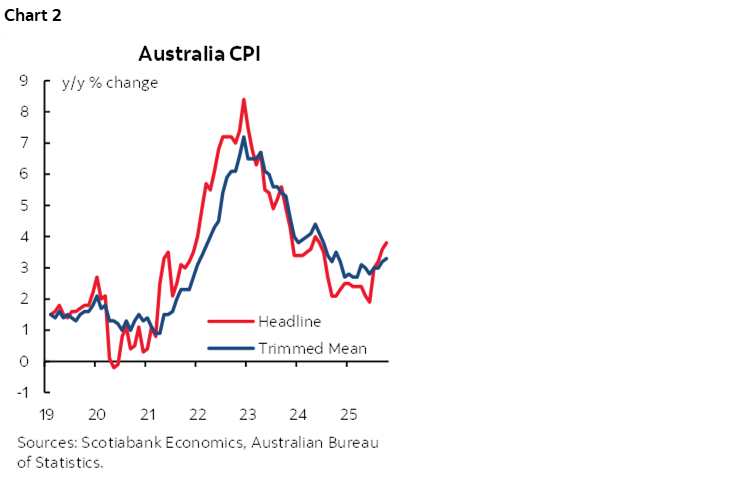

Aussie CPI Contributed to the Antipodean Rates Sell Off

Australian rates also sold off at first because of stronger than expected inflation during October. CPI was up by 3.8% y/y (3.6% consensus and prior) with the core trimmed mean measure also accelerating (3.3%, 3.0% consensus, 3.2% prior). The curve continued to bear flatten well after the data and after the RBNZ’s hawkish sounding guidance. Markets largely view the RBA as done while the debate pivots toward monitoring accelerating inflation (chart 2).

Light US Data on Tap

Three releases are on tap for the diehards as the biggest ones won’t arrive for weeks to come.

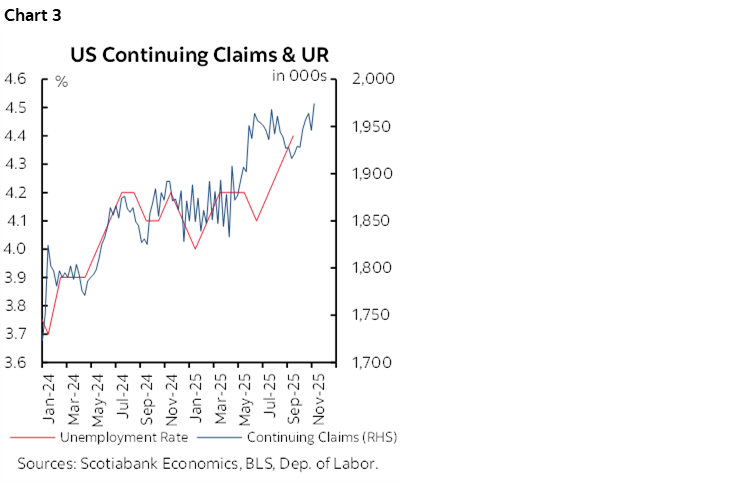

Watch continuing claims to see if they continue to rise which would be a bad omen for the unemployment rate (chart 3).

Durable goods orders are expected to jump higher on airplane orders with Trump flogging Boeing in exchange for favours the world over. Core orders ex-defence and air have been performing decently largely on AI-related investment. It’s September data, however, as we await fresher readings that were held back by the Trump administration’s government shutdown.

The Fed’s Beige Book of regional economic conditions will include further anecdotes that may be useful as input into regional growth and price pressures, but by that time few will care ahead of the holiday.

America’s Love of Subsidies Extends to Data Centres

Speaking of AI, US taxpayers are footing a substantial bill for the ongoing investment in data centers. This database (choose data centres under ‘specialized industry’) estimates that about US$16 billion in subsidies have been granted to about 60% of the over 470 data centre investments they track that disclose the subsidies. It's likely considerably higher than that given missing data. At the top of the list is Amazon's centre in Indiana that has received $8.28B. Amazon is on the list 26 times. Apple 10 times. Meta 7 times. A chief complaint of America’s trading partners is the pervasive nature of subsidies across so many US industries alongside the frequent bailouts that are granted to failed enterprises. As part of the AI boom, these data centres are buoying the US economy and serendipitously masking pernicious effects of other policies (tariffs, immigration etc) and elevated uncertainty. They are not without their shortcomings, however, including subsidies, effects on local power demand and rates, and effects on the local communities.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.