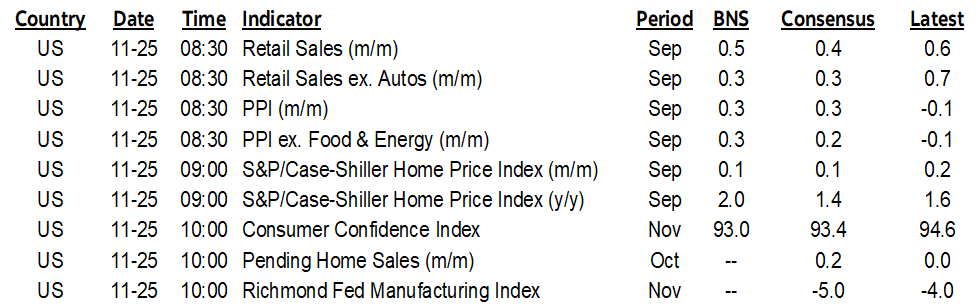

ON DECK FOR TUESDAY, NOVEMBER 25

KEY POINTS:

- Global markets lie in wait for US releases

- US data dump to feature seven releases, some fresher than others…

- …but the key reports won’t arrive for weeks to come

- RBNZ expected to cut tonight

Global markets lie in wait for a string of second and third tier US macro reports this morning. Risk appetite is little changed with most equity benchmarks looking flat so far. Ditto for little movement across global sovereign bonds. Extra ditto for the dollar.

A wave of US releases will dominate calendar-based risk today. None of them are top tier as we’ll have to wait a while to get those. Some of the key ones (retail, PPI) will be stale on arrival as September readings won’t settle much of anything. What may give a fresher sense of consumer attitudes into US Thanksgiving and the surrounding holiday sales will be consumer confidence. Most expect confidence to continue slipping, but then again, actions speak louder than words and so we need to track high frequency readings to get a sense of how the holiday season is tracking.

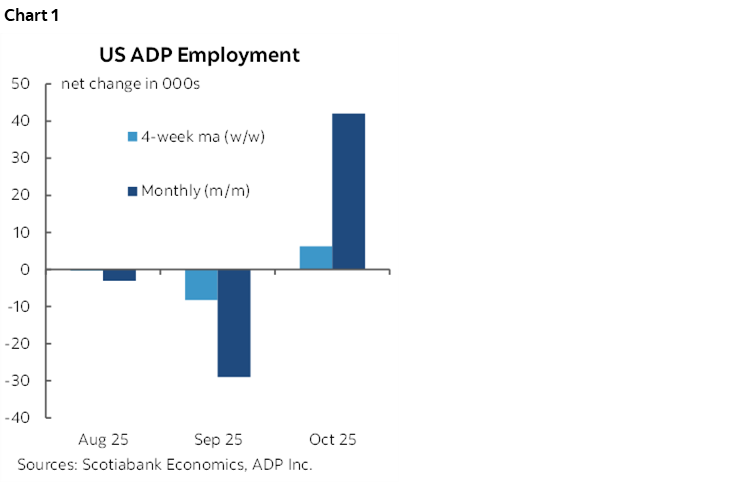

- US ADP weekly estimate (8:15amET): The four-week moving average of ADP private payrolls will extend to the week ending November 7th. That’s not yet in the nonfarm reference period for November but it’s knocking on the door, and it’s not in the reference week for the companion household survey. The weekly measure doesn’t track ADP’s monthly measure very well (chart 1).

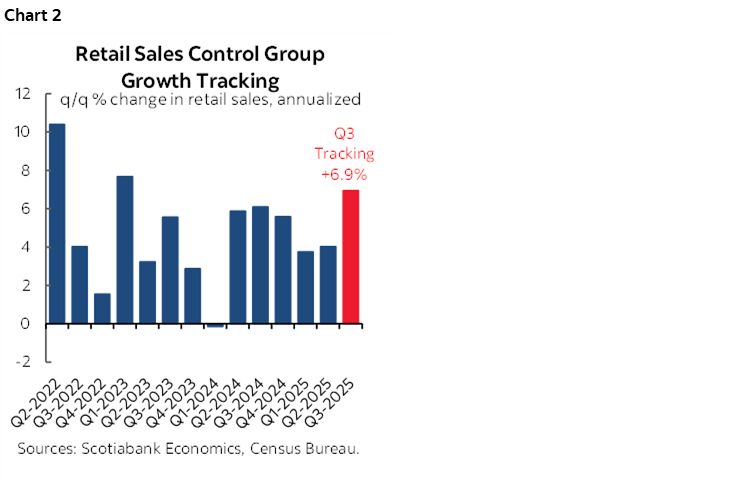

- US retail sales Sept 0.4% m/m (8:30amET): Total sales are roughly estimated to rise by about ½% m/m SA. Among the drivers are expected to be the 2% m/m SA rise in new vehicle sales and higher gasoline prices. Another decent gain in nominal core sales is also anticipated. Key, however, will be converting to inflation-adjusted sales that may be little changed net of price effects. Chart 2 shows tracking of the important ‘control group’ that serves as input into consumption within GDP accounts. The third quarter is tracking quite strongly pending this morning’s update.

- US PPI Sept 0.3% m/m / Scotia 0.3% (8:30amET): The producer price index will be the final piece of the puzzle to firm up expectations for the Fed’s preferred inflation gauges—PCE and core PCE. Several of its components flow through to PCE along with the weighted contributions from core CPI that equalled 0.22% m/m SA in September. Total PPI is expected to rise 0.3% m/m (Scotia 0.3%) and core PPI is expected to gain 0.2% m/m (Scotia 0.3%). Core PPI may be more likely to swing the core PCE estimate up to 0.3% than down to 0.1%.

- US S&P repeat sale home prices Sept (9amET): House price inflation is clearly cooling. Today’s updates of repeat-home sales prices in September and the FHFA house price index are likely to extend the pattern. The S&P repeat measure is only up by about 1½% y/y from a recent peak of about 7½% in early 2024 and this is way down from the low rate-fuelled boom when prices were up by about 21% y/y in early 2022. Calling disinflation in housing is hardly a brave call at this point.

- US consumer confidence November (10amET): Another dip is expected. This measure is more influenced by labour market conditions than the UofM sentiment gauge. Confidence has been running at the lowest readings since ‘Liberation Day’ in April.

- US Richmond Fed mfrg index Nov (10amET): This release has been unaffected by the federal government shutdown. It will serve as input to ISM-manufacturing expectations. Other regional surveys have been mixed such as the surge by the Empire gauge, the small gain by the KC measure, the small improvement in the Philly Fed’s measure, and the drop in the Dallas Fed’s gauge.

- Pending home sales October (10amET): Will softness continue? Pending home sales are up by only 1.5% y/y and have only had one good months in the past four. They serve as a leading indicator for completed existing home sales once the paperwork has settled.

As for the delayed releases, here is the refreshed release schedule for key data. Note that the most important ones like GDP, inflation and nonfarm will arrive well after the December 9th–10th FOMC meeting. As argued in my weekly, I continue to expect the Fed to cut at that meeting partly as a risk management move given the long gap before the next meeting in late January and the risk that markets may be in turmoil after seeing major releases into potential dollar funding pressures.

- PCE for September: December 5th. This also includes related releases like spending and incomes.

- Employment Cost Index for Q3: December 10th.

- Nonfarm payrolls for October: December 16th.

- Nonfarm payrolls for November: December 16th. Yes, same date as October’s release in a doubly whammy.

- CPI for November: This will arrive on December 18th.

- Q3 GDP: December 23rd. The Atlanta Fed’s ‘nowcast’ is tracking 4¼% q/q SAAR GDP growth. The New York Fed’s nowcast is tracking 2.3%. The Bloomberg consensus sits at 2.9% which is the same as Scotia’s.

- PCE for October: We still don’t have a release date for the Fed’s preferred inflation reading for the month of October, nor for the related releases like spending and incomes. It was to have been released on November 26th.

- PCE for November: This was to have been released on December 19th but a new date is pending and may be sometime after Christmas.

- Cancelled releases: And now for the ones we’ll never get because the collection period was fundamentally missed due to the Trump administration’s government shutdown. They include JOLTS job vacancies and related figures for September, the household “Employment Situation” jobs survey for October that provides figures like the unemployment rate, and CPI for October.

NON-US STUFF

There was nothing material out overnight. There is nothing material expected this morning.

The RBNZ is on the docket for a 25bps rate cut tonight (8pmET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.