ON DECK FOR MONDAY, NOVEMBER 24

KEY POINTS:

- Markets continue to be buoyed by Fed-speak

- Trump’s Fed Chair decision pushed out again

- A very light calendar to kick off the week

- On Mr. Vance’s linkage between diversity and living standards

- Global Week Ahead—A Playbook for a Nimble FOMC (reminder here)

Global markets are picking up where they left off on Friday when NY Fed President lent support for a rate cut in the near-term. December’s probability of a cut stands at about 70% now with about 17bps priced in. Our call remains unchanged in favour of a 25bps cut. Stocks are rallying pretty much everywhere this morning.

Fed-Speak Update

A couple of Fed speakers are weighing in with updated comments. Governor Waller is consistent with support for a cut next month. Boston Fed President Collins reaffirmed her relatively hawkish stance on Saturday when she said “it doesn’t suggest an urgency to be more accommodative in monetary policy” but that she hasn’t made a decision on how she will vote at the December 9th–10th FOMC meeting. This is nothing new; I already had her down as a ‘hold’ in the survey of voting FOMC members provided in my weekly.

Delayed Fed Chair Announcement

White House Director of the National Economic Council Kevin Hassett commented about the search for a new Federal Reserve Chair yesterday. He said “we” may decide around new year, that Trump may interview them in the next couple of months and that potentially new fed leadership could cut rates. Funny, Trump keeps saying he’s already made up his mind. Online betting still has Hassett viewed as the most likely Chair.

Canadian PM Carney Tries to be Coy About Trade Talks

Canadian PM Carney said “who cares” in response to a question about when he will next speak with Trump but that he’s ready to return to talks when the US is ready. Canadian markets are taking it in stride.

Light Data

Mexican bi-weekly core CPI remained at 4.3% y/y for the week ending November 15th.

The only N.A. data on tap will be the Dallas Fed’s manufacturing reading for November (10:30amET) and the Federal Reserve’s annual revisions to industrial production (12pmET).

Statcan offered preliminary guidance that October’s manufacturing sales slipped by 1.1% m/m in nominal terms. That’s not terribly surprising after a 3.3% surge in September.

Rebuttal to Vance’s Assault on Canadian Diversity

Over the weekend, US Veep J.D. Vance tied the surge of immigration and its diverse population to falling Canadian living standards.

For starters, let’s get the cause and effect right by pointing to the US evidence. Economists generally argue that US immigration policy will cost the country’s prosperity. Mass deportations are estimated to curtail GDP growth with one such study being here. I figure that turning off the immigration taps will cost the US between ½% and 1% on GDP growth into next year which may be serendipitously masked by surging AI investment if it continues. No immigration means lost business opportunities for small businesses that can’t find workers, dented demand for housing and consumer spending, slower business start ups etc. Most economists would argue that immigration and diversity were massive contributors to US fortunes including bouts of new arrivals at key points in its history like the late 1800s and post-war era.

Second, yes Canada overshot on poorly managed immigration policy coming out of the pandemic and immigration policy tightening over the past year is the response. I have more confidence Canada will return to its welcoming stance in favour of immigration over coming years than the US. Immigration has long been a strength of Canada’s economy. While there are some haters in Canada—just check social media feeds—in my opinion it’s not the same toxic debate that it is in the US. Canadian immigration policy is more about a temporary course correction now than what I judge to be a much more isolationist and xenophobic stance in the US. Most Canadians are welcoming.

Third, Canada has its challenges for sure, but they date back long before the surge of immigration after the pandemic and its diversity is a strength, not a liability. Weak Canadian labour productivity, underinvestment, low rates of technology adoption, low spending on R&D, and a frustrating stance on developing resources over the past decade are definite challenges—and nothing new. The Carney administration is trying to fix some of that.

To blame diversity for the challenges facing Canada’s economy is a) without evidence, b) against what most economists would say is a strength, and c) the kind of toxic nonsense designed to divide people and pit them against each other.

It’s also the latest example of senior US administration officials inserting themselves into domestic Canadian politics throughout Trump 1.0 and Trump 2.0. Governor. 51st state. Assimilation. The US administration has made it perfectly fair game for many other countries to poke their noses into American politics on the path to the midterms and the 2028 Presidential election in a you started it sense.

All that said, here’s an updated Canada-US comparison that shows we’re not all bad at everything we do north of the border Mr. Vance.

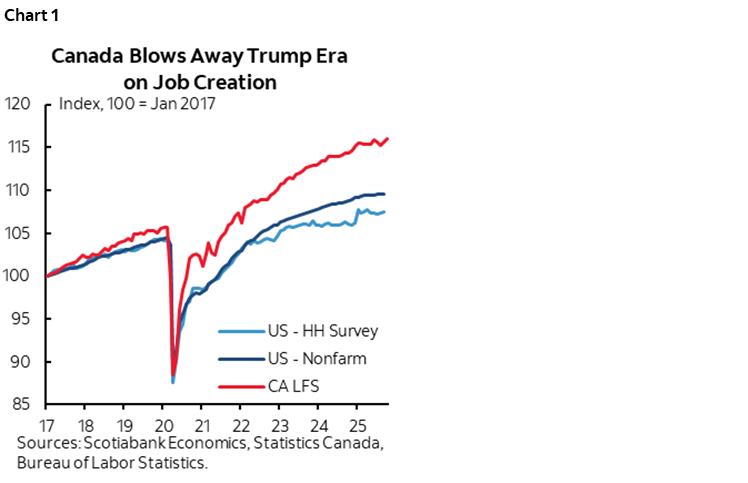

1. Canada has a better track record at generating jobs than the US under both Trump 2.0 and since Trump 1.0 (chart 1). Since inauguration 2025, Canadian employment is up by +0.4% which slightly edges out US nonfarm payrolls at +0.36% and significantly exceeds the more complete US household survey’s measure of employment at -0.15%. Since inauguration day in 2017, there is simply no comparison. Canadian employment has been up by 15.6% versus a 9.6% gain in nonfarm payrolls and a 7.6% rise in the US household survey’s measure.

Furthermore, Canada ranks higher than the US across many socioeconomic readings. Among them are political stability, civil rights, and health care. Canada’s government doesn’t shut down all the time in keeping with the nation’s ‘peace, order and good government’ motto.

2. There is little question that US incomes on average are higher than Canada’s and that Canada’s GDP per capita has been falling at least temporarily, although reducing the population of temporary residents is likely to improve this measure. But much of that comparison reflects a skewness toward the very well off.

3. As evidence, on income inequality there is no comparison. Canada’s Gini coefficient is much lower than the US (here).

4. World Bank Human Capital Index: Canada ranks above the United States in every single category including overall human capital index, the index for men and the index for women, expected years of school, harmonized test scores, years of school and survival rates. Get the data here although it is dated as the latest available data is for 2020 yet they say it isn’t cancelled.

5. Canada ranks just above the US on the UN’s Human Development Index. Go here, click on download dataset.

6. The Economist’s Global Liveability Index includes one Canadian city (Vancouver) in the top 10 and four in the top 20 worldwide and no US cities in the top 20. Toronto is 12th, Calgary 18th, and Montreal is right behind at #19. The highest-ranked US city in the world is Honolulu—at #23. Washington is #38, New York 69th. Here.

7. Canada ranks higher than the US on harmonized test scores (here and here).

8. Canada ranks far safer than the US on overall crime rates. These folks rank Canada as a category 3 country on a 1–11 scale and rank the US at 7 on the same scale. The US murder rate is far higher than Canada’s.

9. US fiscal policy is mismanaged by a massively wide margin to Canada. The US Federal government’s deficit to GDP ratio is almost 6%. Canada’s is about 2½%.

10. Canada has longer life expectancy than the US by several years on average according to both the UN and World Bank measures (here).

11. Both countries have shameful stats on drug use, but the US drug use rate per 100,000 is estimated to be more than 75% higher than Canada’s (here).

In short, if you’re going to blame diversity and immigration policy for all that ails Canada, then this list offers a compelling rebuttal in a rounded defence of our society. The key is to leverage diversity’s advantages by getting more of the others stuff right while retaining the things that make Canada a great place to live.

Last, if you want to see diversity in action in Canada, then come to Toronto or Vancouver when the World Cup starts next July. They’re among the best cities in the world to observe and participate in the Cup as evidenced by the rich array of different flags and shirts being worn across the cities during the contest. #diversity.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.