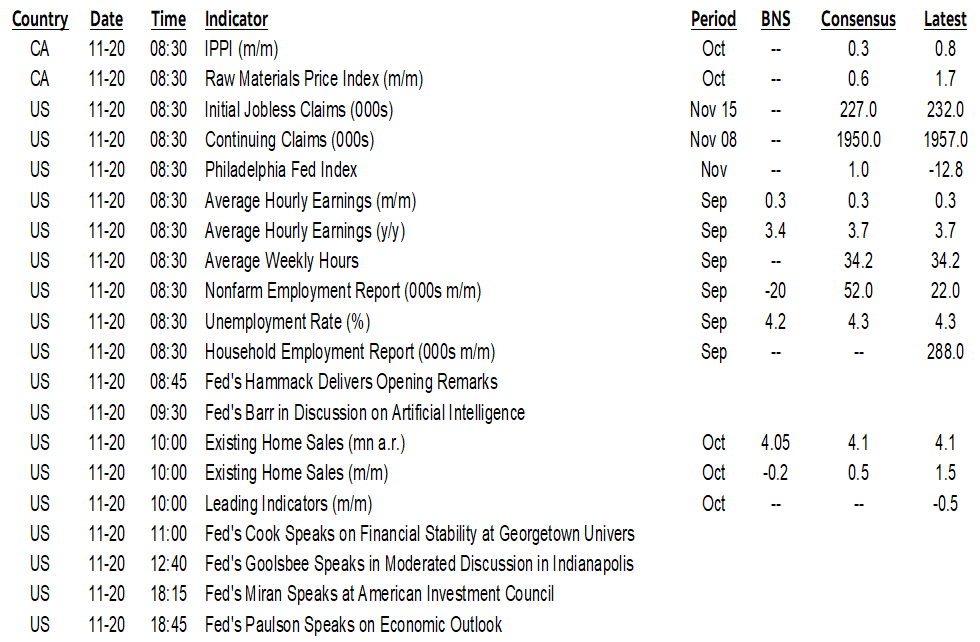

ON DECK FOR THURSDAY, NOVEMBER 20

KEY POINTS:

- Tech earnings buoy equities ahead of nonfarm

- Nonfarm payrolls due today, December’s FOMC decision could depend on it...

- ...given the Fed’s ridiculously extreme data dependence

- FOMC reactions will follow payrolls

- Why markets largely ignored the FOMC minutes

- JGB selling pressure driven by BoJ comments, fiscal stimulus plans

- US jobless claims will be lost behind payrolls

- US home sales likely to be flat

- SARB likely to cut

Stocks are broadly higher as Nvidia’s earnings blew threw expectations across all key measures from earnings to revenues to guidance. US equity futures are up by over 1% with European cash markets performing similarly. Sovereign bonds are a touch cheaper across most major benchmarks and the dollar is mixed. All of this could spin on a dime at 8:30amET.

NONFARM PAYROLLS COULD BE QUICKLY FADED

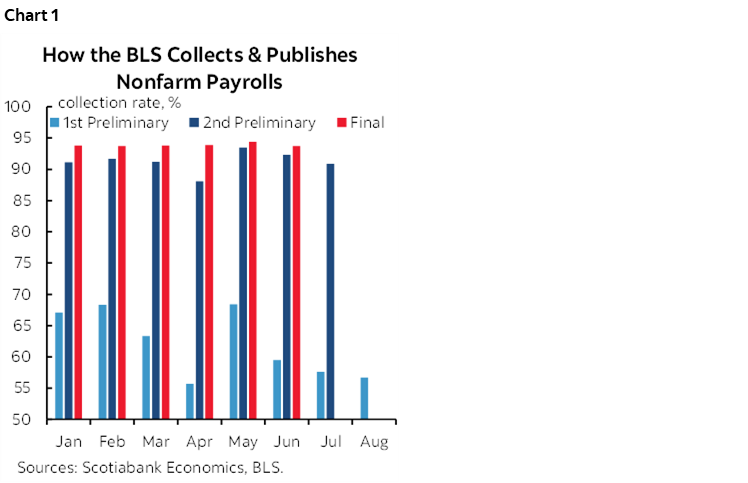

I’m so sick of writing about expectations for September’s nonfarm payrolls. Let’s just get it over with and onto others. Yesterday morning’s note summarized several notes since September regarding expectations for nonfarm payrolls (8:30amET). The massive +/-136k 90% confidence band is not done justice by the tight range within a boring consensus that is under-sampled this time, but I have nothing further to add to expectations. Let’s just see the numbers and move on. One issue is whether having had much more time for this report could raise the initial data collection rate relative to the final collection rate and hence lower subsequent revision risk (chart 1).

In any event, the payrolls reports that may matter much more will be the November and December ones that the BLS guides will not be simultaneously available until December 19th—and hence nine days after the next scheduled FOMC decision.

WHY MARKETS IGNORED FOMC MINUTES

Screaming across terminals yesterday afternoon was the headline that “many” FOMC participants did not support a rate cut in December. Here’s the main quote:

"Many participants suggested that, under their economic outlooks, it would likely be appropriate to keep the target range unchanged for the rest of the year. "

And markets yawned. Why?

- one caution is that the minutes are not vote-weighted and therefore the ‘many’—not a majority—who are opposed to easing overstates the opposition to easing. By my reading, the members who will vote in December are mostly on board with cutting with the main exceptions being a pair of regional Presidents (Boston’s Collins, KC’s Schmid) and with Chicago’s Goolsbee on the fence. Whatever happens, there is likely to be a number of dissenting voices once again.

- Markets likely realized how extremely data dependent the FOMC is. Conditions could turn on a dime here. This is the problem with such ridiculous near-term data dependency. The Fed is paid to forecast. Mandated to forecast. Required to have a view about the future. Employs zillions of people and massive resources precisely to be able to forecast. But shut the government for a month or so and they stick their collective heads in the sand because they want the latest data for what happened to last month or the month before. In my view, this is a sign of weakness at the top.

And you can bet your bottom dollar that the White House read the minutes too. Trump's pledge to likely announce a nomination for Fed Chair before Christmas just got an added boost. Maybe he does so before the December 9th–10th meeting. Then it would matter less whatever Powell says in his presser if the shadow chair is basically saying to stop listening to Powell. Given Trump’s behaviour, he could put out a TS post on his choice at any moment especially since he already says he has made up his mind.

My weekly will provide novel suggestions for how the FOMC can handle data uncertainty into year-end.

FOMC REACTIONS TO FOLLOW PAYROLLS

Cleveland’s Hammack (8:45amET), Governor Barr (9:30amET), Governor Cook (11amET), Chicago’s Goolsbee (12:40pmET) and Governor Miran (6:15pmET) are all scheduled to speak in nonfarm’s wake. Watch for their immediate reactions. There may be others chiming in.

OTHER US DATA

Weekly initial and continuing jobless claims will be refreshed at the same time as nonfarm payrolls which likely means they’ll take a distant back seat. Watch initial claims for guidance on job market pressures at the margin. Watch continuing for guidance on difficulties around reabsorbing laid off workers back into the workforce as the average duration of unemployment continues to rise. A caution is that I think we’ll get all weeks of data since the shutdown began when the 8:30amET numbers come out, but a) the DoL had said this might not be until the e.o.d. today, and b) there won’t be full individual news releases for each of the intervening weeks.

Existing home sales for October are likely to be flat based on little movement in pending home sales for an extended period (10amET).

OTHER INTERNATIONAL

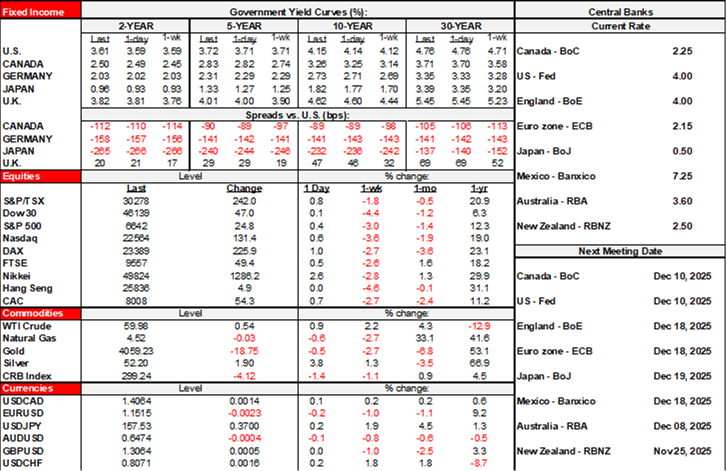

JGBs cheapened overnight on two main developments. One was that a BoJ Board member—Junko Koeda—expressed openness to a rate hike next month. That’s not priced amid wider expectations for a hike in January. Next week’s Tokyo inflation gauge may further inform expectations. Two was a Bloomberg article about new PM Sanae Takaichi’s plans to apply about ¥18 trillion (about $110B) of fiscal stimulus which exceeds prior plans under the previous administration. The curve bear steepened with the 2s yield up 3bps, the belly up 6–7bps and the long end up 3bps. In addition to JGB selling, the yen is among this morning’s weakest performers to the dollar. Should fiscal stimulus pick up, the BoJ’s confidence to hike may rise commensurately.

SARB is expected to cut by 25bps this morning (8amET) particularly after yesterday’s softer than expected South African CPI in m/m terms.

China left its 1- and 5-year Loan Prime Rates unchanged as universally expected.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.