ON DECK FOR WEDNESDAY, NOVEMBER 19

KEY POINTS:

- Markets brace for key data, Mag7 earnings

- Nvidia earnings will get the ball rolling tonight…

- …ahead of global PMIs and nonfarm

- Reminder: Nonfarm preview

- UK CPI wasn’t light, but good enough to reinforce BoE expectations

- Bank Indonesia holds with dovish bias

- Soft core CPI reinforced SARB expectations

- Aussie wage growth remains firm and above the RBA’s inflation target

It’s roughly T-1 until all heck possibly breaks out with Nvidia’s earnings in today’s after-market, tonight’s round of global purchasing managers’ indices, and then the grandaddy of all global macro reports with tomorrow’s nonfarm payrolls in sight. This morning’s tepid and mixed market moves really don’t matter until we start this parade,

US MAINLY FOCUSED ON NVIDIA

Nvidia releases Q3 earnings in the after-market (4:20pmET). Consensus expects US$1.26 for EPS but there is a lot packed into one of their releases for analysts to evaluate by way of how markets react.

FOMC minutes arrive at 2pmET. They’ve been largely superseded by the plethora of mixed FOMC speak since the October 28th–29th meeting and may quickly fade behind tomorrow’s nonfarm release.

We also get trade figures for August this morning (8:30amET).

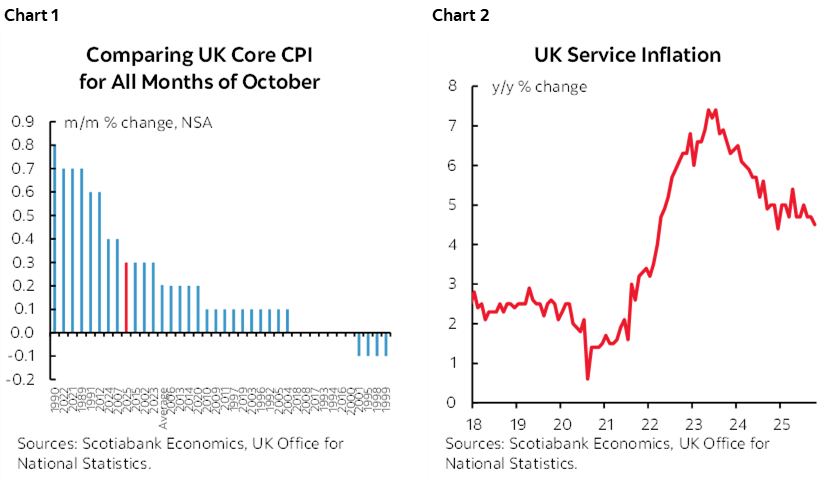

UK INFLATION WASN’T LIGHT, BUT GOOD ENOUGH

Gilts and sterling were little affected by UK inflation figures for the month of October. The 2s yield slipped by a couple of basis points upon release and sterling is a middle of the pack performer among major crosses to the USD. Pricing for the December 18th BoE meeting added 1–2bps with about 22bps of a quarter point cut baked in.

I wouldn’t say the figures were terribly light by any means.

UK core CPI landed at 0.3% m/m NSA and 3.4% y/y (3.5% prior) as the m/m measure was a tick above the long-run average for like months of October (chart 1). Services CPI pulled back to 4.5% y/y (4.7% prior) and 0.2% m/m NSA. Chart 2. The m/m services reading was among the lowest on record for like months of October while the y/y rate remains high.

BANK INDONESIA—NO SURPRISES THIS TIME

Bank Indonesia held its policy rate unchanged at 4.75% as widely expected. The hold was partly explained as being driven by a desire to stabilize the rupiah, given high import propensities and hence inflation risk, and it worked as the currency slightly appreciated overnight. Guidance continues to point to a dovish bias open to further easing in data dependent fashion.

SARB TEED UP FOR A CUT

South African inflation was the last piece of evidence needed to firm up expectations for SARB to cut tomorrow. CPI was up by only 0.1% m/m NSA with core matching that. Core slipped a tenth to 3.1% y/y and the m/m reading was relatively light compared to like months of October in history.

AUSSIE WAGE GROWTH REMAINS FIRM

Q3 Australian wage growth was 0.8% q/q SA. The annualized rate is shown in chart 3 and it remains above pre-pandemic rates and just above the top end of the RBA’s 2–3% inflation target range.

NONFARM COMMENT

This is the most prolonged explanation of a nonfarm payrolls call in the history of nonfarm payrolls call thanks to the longest government shutdown on record! It’s like a lingering bad smell that just won’t go away. Two months of explanations for the call on a wonky report that’s full of quirks and upon which too much rests by way of potential Fed implications. My guesstimate is still at –20k.

But on the day before the numbers here are reminders of my thinking around the -20k estimate for nonfarm payrolls in September. Yes, September.

Here are supporting pieces:

- Weekly from September 26th included a pre-shutdown preview for the -20k payrolls estimate.

- There was a little more in my morning note from Monday.

- Last week's weekly included a full sweep of the US labour market with various metrics.

I won’t repeat all of that, but here are some key summary points of the arguments behind -20k:

1. Seasonal hiring is expected to continue cooling toward lower than average rates for September.

2. SA factors have been getting re-estimated in a way that I think will dampen SA payrolls. The recency bias behind their calculations is beginning to be applied to outside of the immediate pandemic years that distorted the factors.

3. A blend of other readings points to broadly based evidence of softness, none of which are individually reliable but mostly point in the same direction. They include measures like ADP’s drop, the surge of Challenger job cuts, rising continuing claims that indicate rising difficulty getting back into the workforce after being let go, ISM-employment that continues to shrink, confidence jobs plentiful that signals weak job availability, etc.

4. Noise should have you more open minded than consensus. The 90% confidence band on estimated payroll changes is +/-136k. There is a high noise factor which is not reflected within an overly tight consensus and even my estimate could well be within the realm of statistical noise. So should nonfarm’s quirks, like counting multiple job holders, birth-death model adjustments, falling data reliability of job market surveys in general, distorted SA factors etc etc. We also can’t get some data like updated ICE arrests and the possible direct and indirect impact on the job market because that data was conveniently suspended by the government shutdown.

And by the way, only about half of the usual nonfarm consensus is included in Bloomberg's survey so far. Somehow they misplaced pre-shutdown estimates, like in a dog ate the homework kind of way. Or shops didn't resubmit (we deliberately resubmitted). Or other shops have shifted to the sidelines unwilling to submit. I’m not sure, but treat consensus carefully as it is a much smaller sample this time.

And in any event, who cares about September!! That's soooo last year by now. It'll be the October reading and subsequent ones that matter and yet we'll only get October payrolls (not the UR, not hours, not wages etc). Who knows if that arrives in time for the December 10th FOMC but I strongly suspect so.

As for the path thereafter, I hope consumers are dead wrong. The first chart in last week's weekly shows they're the best forecasters of unemployment a year out from now. They're better at it than economists and markets. Against a tendency to dismiss soft data are points like a) look at the strong but hardly bulletproof correlations in the chart except for the onset of the pandemic that could not have been anticipated, and b) consumers hear plans within their companies and it bubbles up into something that may be useful at an aggregated level. We're on the outside trying to evaluate changes in the job market and forecast them. They're hearing management.

BoC SPEECH ON TAP

The BoC’s external DepGov Vincent speaks on productivity and very efficiently so at that since there is no media around it. Just text at 12:30pmET. Not much is expected by way of any market considerations amid the strong signalling that the BoC is sidelined for an extended period.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.