ON DECK FOR TUESDAY, NOVEMBER 18

KEY POINTS:

- Risk off sentiment continues

- Why? Take your pick from many overlapping narratives

- Canadian Budget drama finally ends

- US mass layoffs are tracking high again into November

- US continuing jobless claims point to rising unemployment for longer

- US weekly ADP payrolls merely add more unhelpful noise

- Chile's economy contracted in Q3 due to mining and utilities

- ...with Colombian GDP up next

Global markets are in risk-off mode this morning. Sovereign bonds are rallying—mainly US Ts—and equity benchmarks are broadly lower. Gilts are underperforming because of the coming UK budget mess next week. The dollar is a touch firmer against most major crosses except CAD (post budget vote, see below) and the Antipodean crosses. Gold is flat. So are oil prices. Crypto is feeling the love like an economist at a White House press briefing.

Why? Pick your narrative or take them all together as they’re not mutually exclusive. It’s because of sudden realization that crypto is wildly expensive and stocks may be too; you don’t say! It's because of uncertainty ahead of tomorrow's Nvidia earnings given it’s the biggest stock on the s&p. It’s because of fears of a year-end dollar funding and liquidity challenge even though SOFR is currently better behaved relative to fed funds than it was a couple of weeks ago or so. It's because of uncertainty over lagging US data releases with Thursday's nonfarm payrolls for September in sight. It’s because of mounting concerns about the health of the US job market and how that could drag the economy down (see below). It's because of divisions at the Fed on the appropriate forward rate path and the ambiguity around how each member weights concerns about the job market versus inflation risk. Or maybe it's uncertainty over who will get the Fed's top job and how dovish (not hawkish…) they may be; enter Warsh's slavish WSJ op-ed as the latest entry by the various candidates seeking Trump’s affections and that have numbed my gag reflex.

Canada’s Budget Drama is Finally Over

The Carney administration survived last night’s confidence vote and the Budget will proceed toward implementation with no election in sight at least for now. Several abstentions and the Green Party’s Elizabeth May’s yay pushed the vote over the top. Like it was ever seriously in doubt with polls indicating an election would have yielded the same outcome as in April and no party in good enough standing to fight another campaign. Thank heavens. Now the cottage industry can move on from the budget to perhaps more gainful activities, or not.

US Job Markets Souring

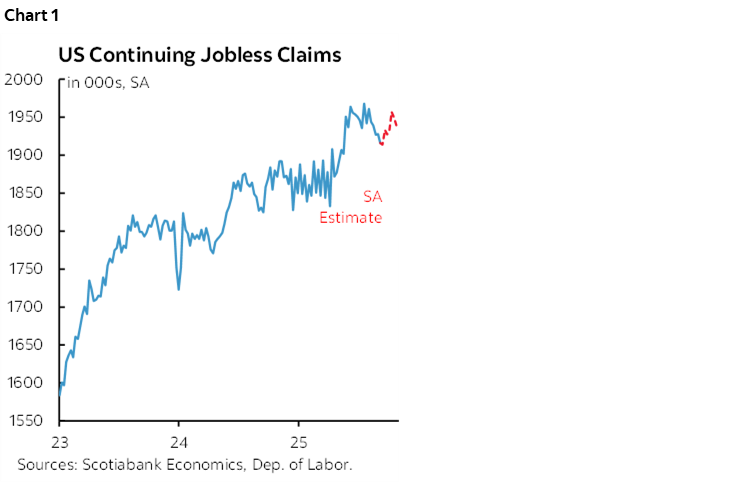

US jobless claims were sort of updated early this morning for the week ending October 18th. They were quietly updated on the Department of Labor's website but not for the three prior weeks. How can you update one week in the middle of the gap and not the prior ones? Very good of you to ask; treat with caution. If the data is sound, then there are two keys.

One is that continuing claims moved higher again and are floating around post-pandemic highs (chart 1). This matters because of the correlations with the unemployment rate; folks are finding it harder to get work after filing initial claims as the US labour market is losing its ability to reabsorb people who have lost their jobs. Witness that the duration of unemployment had climbed to 24.5 weeks back in August as we await Thursday’s September update but will never get October’s reading; that’s the highest reading since early 2022. Folks are remaining unemployed for longer and longer.

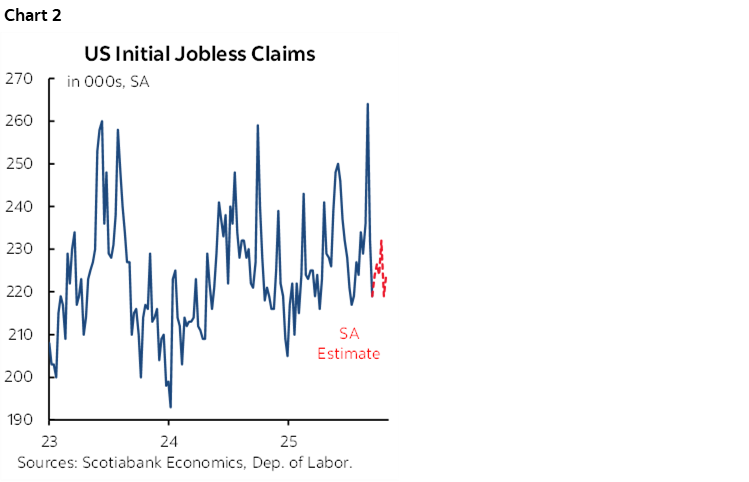

Second is that initial claims came in at 232k that same mid-October week which remains fairly tame. Our seasonally adjusted sum of states reading for initial claims right up to the freshest week also remains tame (chart 2) but it may be too soon for the suddenness of mass layoffs to show up in initial claims. Enter the next points.

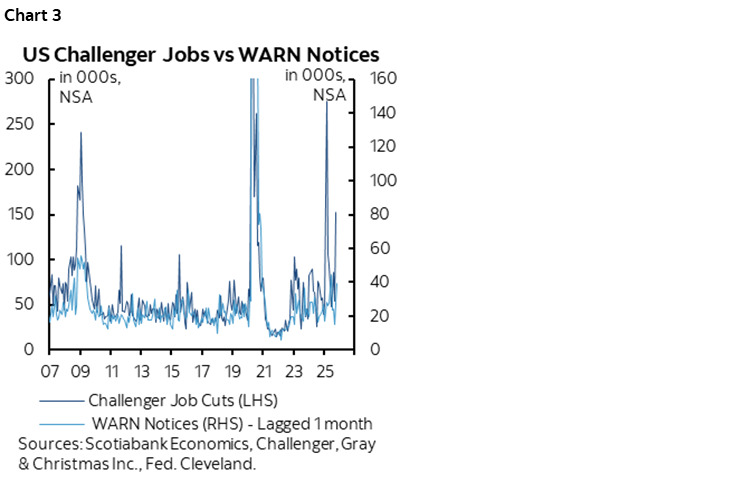

US mass layoffs are tracking at high levels again in November. We can point to a few indications. One is updated data behind this piece by KC Fed economists. 39,000 advance notices of coming layoffs were filed in October which means more pink slips are coming over November. The measure tracks impending mass layoff notices under the WARN Act. The tally usually undershoots Challenger layoffs but is an advance indicator of such although an overstated guide (chart 3). Still, the number of advance notices filed in October is likely to spill over into Challenger layoffs and jobless claims and the unemployment rate with a lag. We can also point to tech layoff tracking sites and individual announcements such as Verizon's this month.

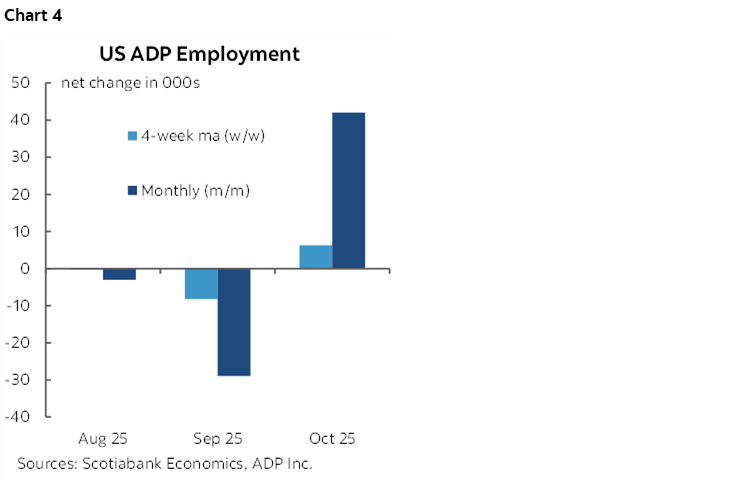

US ADP weekly payrolls are on tap for the week ending November 1st (8:15amET) and so we’re not yet into either the ADP or nonfarm monthly reference periods. Still, the drop at the end of October points to the initial monthly ADP reading for October being revised downward. Chart 4 shows that the weekly ADP private payrolls gauge doesn’t actually track the monthly measure terribly well. Bolt that onto the fact ADP’s monthly measure throws off many head fakes when forecasting nonfarm and it makes one wonder why anyone still pays attention to it.

Other Developments

RBA minutes to the November meeting emphasized that they could “afford to be patient” which merely reinforces the general sentiment.

Chile’s economy stumbled in Q3. GDP slipped by -0.1% q/q SA nonannualized (+0.1% consensus, 0.4% prior). Mining (-4.6% q/q SA) and utilities (-4.5%) were the weakest areas of the economy. Mining has contracted in three of the past four quarters and led by copper.

Q3 GDP Colombia is due out later this morning (11amET).

Canada updates housing starts for October shortly (8:15amET). A modest pullback is guesstimated based on permits.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.