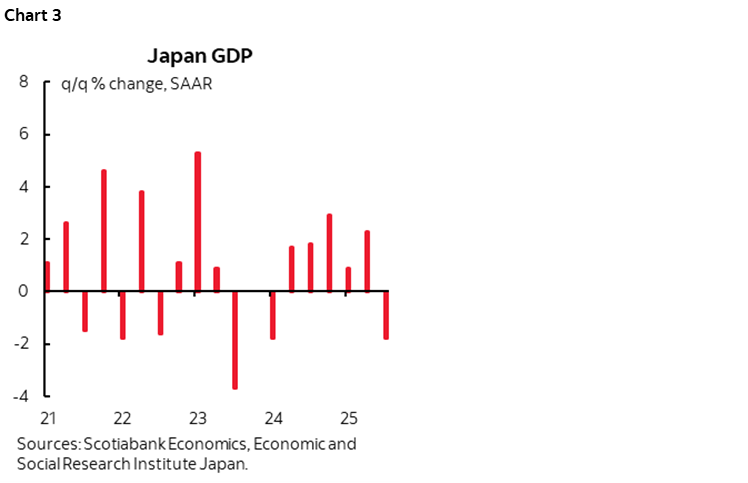

ON DECK FOR MONDAY, NOVEMBER 17

KEY POINTS:

- Global markets extend cautious tone

- CDN CPI will be mere ecotainment

- Key Canadian Budget vote today

- Canadian home sales trending higher, housing starts up next

- Chile’s election run off will likely yield a right leaning government

- Japanese, Thai economies stumbled in Q3

- Global Week Ahead highlights

- Comment on the San Fran Fed’s iconoclastic tariff piece

Regular publishing resumes today after I was out last week. Markets are starting off in generally risk-off mode, but not evenly so. US and Canadian equity futures are slightly positive so far while European cash markets are declining after weak sessions in Japan and China. Sovereign yields are gently lower across major markets. The dollar is mixed but a smidge firmer against the Euro and yen. All of this is highly tentative ahead of the week’s major developments that are summarized later in this note in lieu of my usual Global Week Ahead.

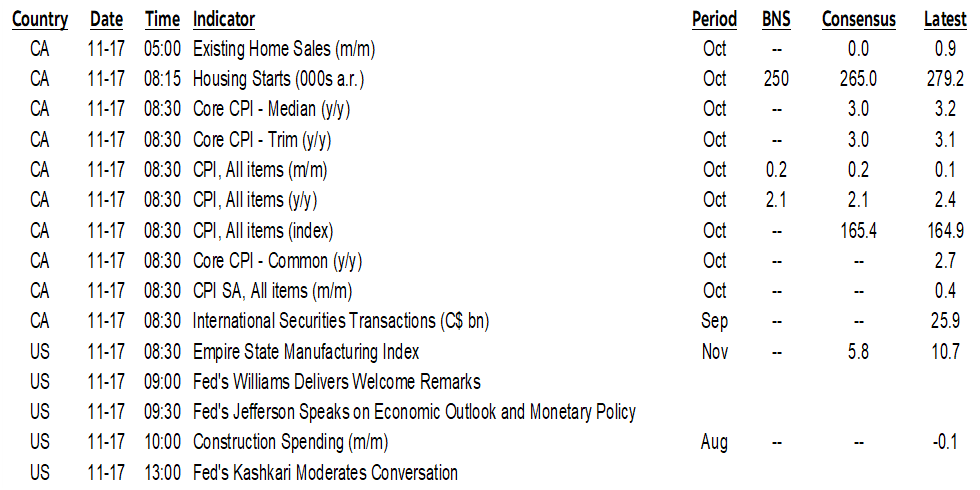

CANADIAN INFLATION—ECOTAINMENT

Canada updates CPI for the month of October today (8:30amET). No shutdown here, just “Peace, order, and good government” as per section 91 of the Constitution Act of 1867!

And it doesn’t matter. It’s the last inflation report before the BoC’s next decision on December 10th, but they’ve made it clear that they are sidelined at least for the next several meetings.

I’ve estimated headline CPI at 0.2% m/m NSA and 2.1% y/y. October often brings substantially positive seasonal effects on prices, but lower gas prices should offset some of that. Consensus is shouldered around 0.2% +/- 0.1%.

Core inflation measures are what will matter more, except the BoC doesn’t know what core measure(s) it wishes to track closer than others and has signalled that next year’s 5-year review of its policy framework may add a couple more. The trends in two of them are shown in chart 1.

Being this close to meaningless data let’s just see what it shows and move onto more important matters.

CANADIAN BUDGET VOTE WILL PROBABLY END ELECTION RISK FOR NOW

The final confidence vote on the proposed federal Budget will be held this afternoon (time TBD). The Liberals have 170 seats and need two more members of some combination of the Conservatives, NDP, BQ and Green Party to support the Budget. The Conservatives and BQ have said they’re out. Most NDP members seem to be indicating opposition but could easily cough up two votes or abstain which would also pass the vote in feigned opposition. The sole seat held by Green Party leader Elizabeth May is on the fence and trying to secure concessions for her vote.

I highly doubt that the final vote will fail given that the opposition is in tatters for various reasons.

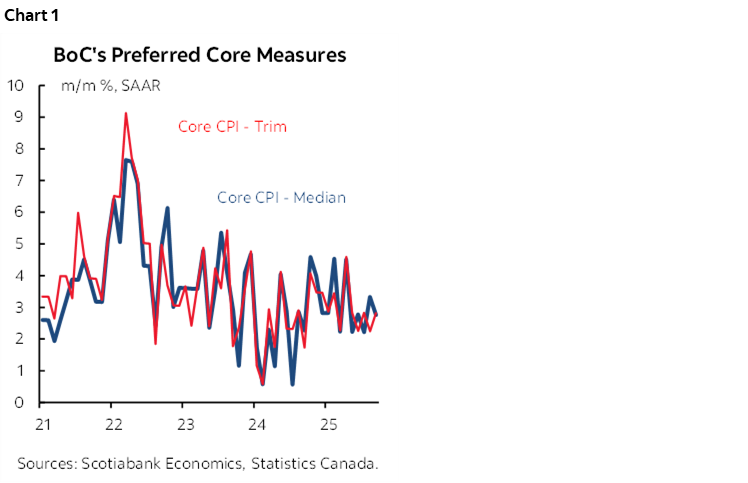

CANADIAN HOME SALES TRENDING HIGHER

Canada also updates a pair of housing indicators today.

October’s existing home sales are already out this morning and posted a gain of 0.9% m/m SA. That’s the fifth gain in the past six months with the only dip being in September (-1.7%). Chart 2. New listings climbed by 1.4% m/m SA, pushing the sales-to-new listings ratio up 1.2 points to 52.2% which remains in balanced territory. Total listings are up 7.2% y/y. Months’ supply remains at 4.4 months and is a little tighter than the long-run average of 5.0. Repeat sale home prices were up 0.2% m/m SA by down 3% y/y.

Housing starts for October could slip back from 279k in September toward 250k or so given factors like dwelling permits (8:15amET).

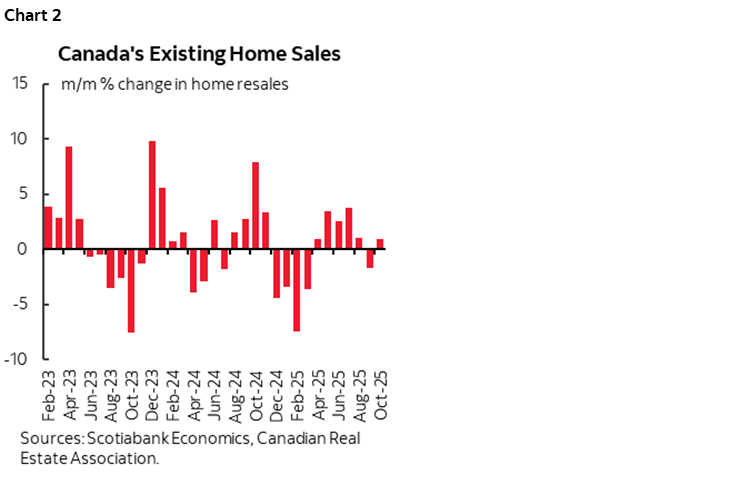

JAPANESE, THAI ECONOMIES STUMBLED

Japan’s economy shrank by -1.8% q/q SAAR in Q3 (chart 3). That’s a tad less than expected (-2.4%) partly due to an upward revision to Q2 (2.3% from 2.3%). Consumption grew by only 0.1% q/q SA nonannualized. Business spending was the biggest surprise (+1.0% q/q SA, -0.1% consensus). Net exports shrank by 0.2% q/q SA.

Thailand, however, disappointed expectations. Q3 GDP shrank by -0.6% q/q SA nonannualized which was double the rate of contraction that was expected by consensus. The prior quarter’s expansion was revised down a tick to 0.5% q/q SA.

CHILE’S MARKET-FRIENDLY ELECTION

The first round of Chile’s Presidential election was held yesterday and the Chilean peso is loving it so far this morning. The election seems to be a set up for a market-friendlier right of center government to emerge in the final runoff on December 4th after years of a leftist administration. The far-left Communist candidate (Jeanette Jara) and the conservative candidate José Antonio Kast candidates both advanced. Other center-right candidates are expected to throw their support behind Kast and have already begun to do so.

GLOBAL WEEK AHEAD HIGHLIGHTS

What follows are highlights of what is on tap this week In lieu of a Global Week Ahead publication since I was out last week. The marquee development is clearly going to be Thursday’s nonfarm payrolls report for September except it’s really the next one that matters instead.

Multiple major markets will refresh S&P purchasing manager indices for November. Australia and Japan kick it off on Thursday evening (ET) followed by India into Friday and then the Eurozone, UK and US.

UNITED STATES—Nonfarm to Dominate

We’ll finally get September’s nonfarm payrolls and related job market readings like the unemployment rate, hours, and wages on Thursday. Though data was collected before the shutdown, more may have been received since then which could mean future revision risk will be more modest than normal.

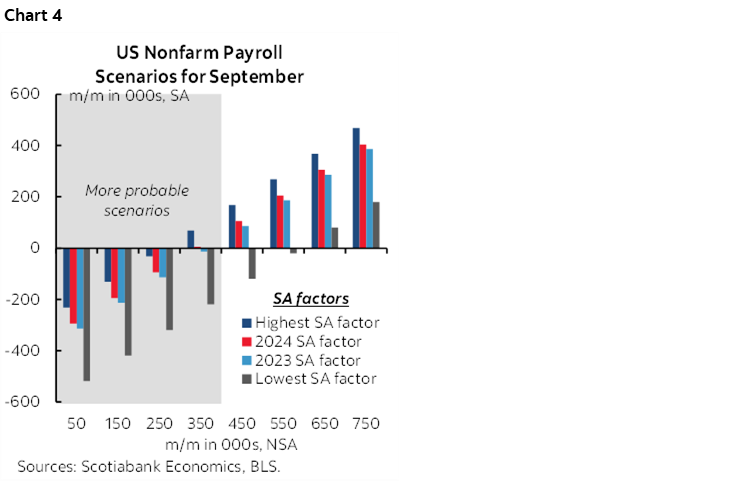

My estimate remains -20k as originally provided ages ago but with a downtick for the unemployment rate to 4.2% on assumptions specific to the household survey. Drivers were explained back here except the order of chart references was a bit messed up in that report. Chart 4 shows the range of scenarios for nonfarm changes at different SA factors and seasonally unadjusted payroll changes and my leaning toward the downside scenarios.

Since that article was written the tone of US job market data for September has soured in support of my estimate. ADP private payrolls fell by -32k in September and the weekly data leans toward October’s initial estimate being revised downward, though in fairness it is often a misleading signal for nonfarm. Consumer confidence jobs plentiful fell which indicates consumers saw fewer job opportunities. ISM employment gauges continued to signal contractions.

Minutes to the October 28th–29th FOMC meeting arrive on Wednesday (recap here). The minutes are likely to be stale on arrival given the abundance of divided Fed-speak since then.

Readings we’re sure to get this week will also include the Empire manufacturing gauge for November (today), ADP’s weekly measure (Tuesday), the NAHB homebuilder confidence reading including model home foot traffic (Tuesday), and existing home sales during October (Thursday).

Other backlogged readings may be released by the BLS, BEA, DoL and Census Bureau pending updated released schedules (here and here).

CANADA—Only One Thing Left

Most of what is of relevance is already covered as it’s due out today. Only retail sales remain (Friday) and we’ll get both an expected dip in September and preliminary guidance for October when independent auto sales estimates conflicted with one another in terms of the direction of change.

ASIA-PACIFIC—Japan CPI, BI Decision

Other than the aforementioned PMIs, there is a smattering of additional regional developments.

- Japan: After already issuing Q3 GDP, up next are trade figures for October (Tuesday), and CPI for October that may rise to 3% y/y for both headline and core (Thursday).

- Bank Indonesia: Wednesday’s decision is likely to be a hold at 4.75% but with a small minority expecting a cut. Recall that this central bank has a very high surprise factor.

- Other developments will include RBA minutes tonight, expected unchanged Loan Prime Ratios from China (Wednesday), and Malaysian CPI for October (Thursday).

EUROPE—UK CPI and Retail Sales

Other than PMIs, BoE watchers will have an eye on UK CPI for October that most forecasters anticipate will see a downtick of the core rate to 3.4% y/y (Wednesday) and retail sales (Friday).

LATIN AMERICA—GDP IN FOCUS AFTER CHILE’S ELECTION

With Chile’s first-round election out of the way the next focus is that several countries will issue updated GDP figures. Q3 estimates arrive from Chile (Tuesday), Colombia (Tuesday) and Peru (Friday) plus monthly economic activity readings for September from Brazil (Monday) and Mexico (Friday).

Outside of all of these regions the only other thing of note is SARB’s decision on Thursday with an expected -25bps cut.

TARIFFS, INFLATION AND UNEMPLOYMENT

A research piece from the San Francisco Federal Reserve was doing the rounds last week when I was off. It posited that tariffs are disinflationary shocks and raise unemployment. It’s a worthwhile contribution to the literature but its stance on inflation is weak. Most would agree about the unemployment part, but this paper settles little to nothing on the inflation debate in my opinion and here are reasons why.

First, the main tariff shocks in the 150 years the paper examined were the era of President McKinley up to his assassination (1897–1901) and the 1930 Smoot-Hawley tariff Act. Most of the rest of the 150 years do not really provide material evidence worth examining in terms of sudden, discrete jumps in US protectionism and it implicitly assumes that the effects of tariff hikes may be symmetrical to the effects of tariff cuts. The paper therefore overstates the sample richness of periods with significant spikes in protectionism.

Second, those eras had much lower US import propensities to today’s. In both the McKinley era and the Smoot-Hawley period, merchandise imports were about 3–4% of GDP versus 3–4 times that today. Further, import shares only capture a portion of how much more integrated the global economy became over the post-war era. Exports, imports, import content to exported products and import contestability are vastly greater today than back in those periods. Broad measures of trade openness show that today compared to 1900 roughly doubled the degree of openness. In short, the tariff sensitivities might be far greater today given much high trade propensities which can invalidate efforts to glean insights from those periods.

Third, the paper doesn’t really make an effort to control for other considerations during those prior two main eras for surging protectionism. One is that it doesn’t control for the supply shock represented by the surge of population growth into the McKinley era when droves of people arrived from Europe, or the expansion of the agricultural and resource sectors that had nothing to do with tariffs. Second is that it doesn’t control for myriad drivers of the Great Depression. Differences in the composition of today’s tariffs to tariffs back then were also not considered nor in the context of today’s difference consumption patterns.

Fourth, for all intents and purposes Asia didn’t really exist in economic terms back then and yet today it is the source of many of America’s cheap goods against which tariffs are being applied.

Fifth, in those two prior episodes, the US and world economies didn’t really face serial shocks to supply chains like today’s including Brexit in 2016, the pandemic, geopolitical conflicts like the Red Sea, Ukraine, Middle East, and possibly Taiwan, Trump 1.0, and Trump 2.0. The massive wave of outsourcing to low-cost countries over the past few decades is without precedence and yet the rise of border frictions over roughly the past ten years could give rise to complicated additive effects on supply chains that suggest the Fed should be vastly more careful about the effects on inflation. In short, tariffs are a subset of complicated serial shocks to global supply chains that may have highly uncertainty additive effects. One possibility is that the one-way outsourcing to low cost jurisdictions now has more to worry about in terms of border frictions to supply chains that may reverse the outsourcing pattern into higher cost markets.

Sixth, not included in the paper—likely due to measurement challenges—are the high compliance and management costs that represent deadweight drains on productivity.

Now for those who would like to use the paper to justify Fed easing, a major risk could be fatally ignoring moral hazard. The more you ease, the more you will perversely encourage thoroughly misguided US trade policies. The FOMC under Chair Powell risks having history judge them as enablers of protectionism which may point out a shortcoming of the dual mandate and the time horizon over which it is interpreted. A further risk could be not treating tariff policy as part of broader policy measures like highly restrictive immigration policy—a combination that did not exist under McKinley.

As for drawing inferences for fiscal policy, recall that tariffs were a dominant source of revenues for the US administration in McKinley’s time before income taxes. The case for relying on tariff revenue today—independent of its pernicious effects—is weaker given a well-established infrastructure for applying and collecting other more efficient taxes. Americans simply just don’t want to pay higher taxes or have benefits cut and are being manipulated into believing a victim narrative on the world stage that seeks to alternatively raise revenues through tariffs that they’ll pay anyway.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.