ON DECK FOR FRIDAY, MAY 9

KEY POINTS:

- Markets continue to price cautious optimism on trade signals

- US-China trade headlines reflect growing US recognition they went too far…

- ...but there remain very high cautions around developments…

- ...not least of which Trump’s conflicting stance

- Canadian jobs are likely to be distorted by temporary election hiring

- Chinese trade is already slowing

- Peru’s central bank surprised with a rate cut

- Colombian, Norwegian CPI surprises higher

- Japanese real wages are falling faster

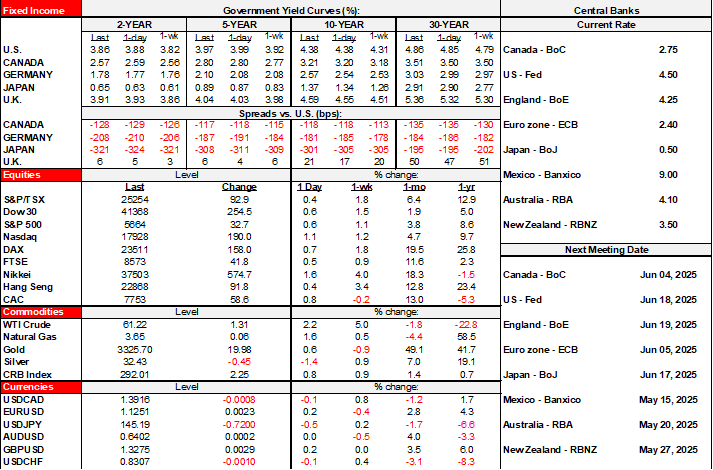

The week may be ending on a fragile but mildly positive note for risk appetite. The catalyst appears to be wishful thinking around trade negotiations as Canada braces for another job market update. US equity futures are up by less than ¼% with the TSX performing similarly and European cash markets slightly outpacing. European sovereign yield curves are mildly bear steepening with US Ts slightly bull steepening and hence slightly outperforming. The dollar is broadly weaker and hence oil prices are up a buck and gold is up by about $20.

SLOW DE-ESCALATION OR FALSE HOPE?

The US administration is reportedly leaning toward cutting its absurdly high tariffs on China in an attempt to coax China back to the negotiating table. Anonymous officials have indicated that the US tariffs could be slashed in half to under 60% with the hope that China matches.

A first caution is that it’s not Trump saying this and his advisers constantly overreach. Enter Trump’s social media post this morning that stated “80% Tariff on China seems right! Up to Scott B.” Which is it, 60, double that, 80?? And Bessent sets trade policy?? Maybe they’re playing bad cop and slightly less bad cop, or maybe it just remains an administration in total disarray.

A second caution is that China has said it won’t negotiate at all until the US drops all tariffs which may or may not be public face-saving. A third caution is that the rumoured tariff cut remains well into territory that crushes commerce by making it unprofitable to supply the market. All of this is setting the stage for talks in Geneva starting tomorrow between delegations led by US Treasury Secretary Bessent and Chinese Vice Premier He Lifeng.

My bias remains that we’re ages away from any possible trade deal and that de-escalation steps to date are immaterial. That includes yesterday’s UK-US trade deal. I’ll write more about this in my weekly in addition to daily notes and chat room posts.

LIGHT OVERNIGHT DEVELOPMENTS

China’s trade figures for April already began to show weakening growth. Exports were up 8.1% y/y in dollar terms (12.4% prior) and 9.3% in local currency terms (13.5% prior). Imports were little changed at 0.8% y/y in dollar terms (-3.5% prior) and -9.2% y/y in yuan terms (-4.3% prior). The country level details show large declines in trade with the US that were partially offset by gains in trade elsewhere such as Europe, elsewhere in Asia, and Canada, thereby raising dumping concerns in those markets.

Peru’s central bank surprised consensus with a 25bps cut last evening. BCRP’s new reference rate is 4.5%. The cut wasn’t totally unexpected as 5 out of 13 in Bloomberg’s consensus called it right. Guidance repeated that the rate “is approaching the level estimated as neutral” and that “Future reference rate adjustments will be conditional on new information about inflation and its determinants.”

Colombia’s CPI reading was a bit higher than expected at 0.66% m/m (0.5% consensus) and with core at 0.56% m/m (0.4% consensus). BanRep’s next decision is ages away on June 27th so more data and developments will factor into its assessments.

Japanese real wages are still falling and at a somewhat quicker pace (-2.1% y/y, -1.5% prior). This is despite strong gains in the annual Shunto union negotiations that only affect less than one-in-five workers.

NOK is outperforming this morning on an upside surprise to Norway’s April inflation reading (0.7% m/m, 0.6% consensus) and warmer underlying CPI (0.5% m/m , 0.2% prior) but that fell a tick shy of consensus.

CANADIAN JOBS PREVIEW

Canada updates the state of its job market in April at 8:30amET. The normally high uncertainty marked by an enormous confidence interval on the household survey is higher yet this time because of how election hiring and early tariff effects may net out.

Change in jobs, 000s:

Scotia: +25

Consensus: +5

Range: -40 to +51, most within -25 to +25 or so

Whisper: n/a

Std dev: 23.77

95% confidence interval: +/-57k

UR: 6.8 / Scotia 6.7

Drivers:

The election is sure to distort this report which may require looking past the headline.

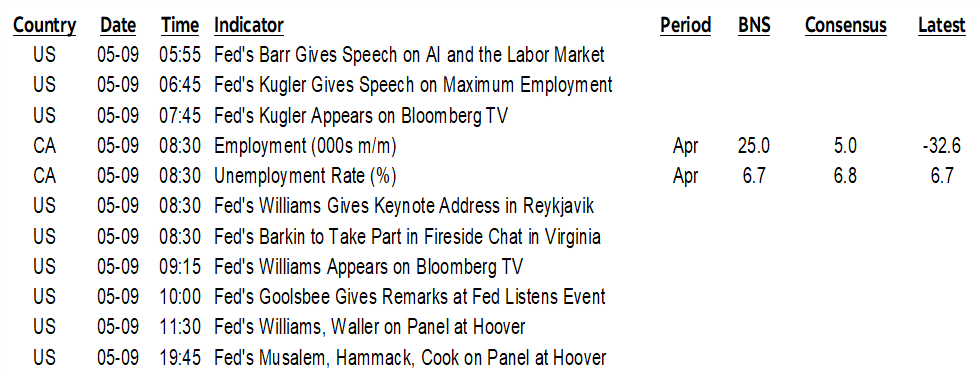

A quarter million folks were hired to run the election which was more than any other election (chart 1). Key is how many of these workers show up in the reference week of April 13th–19th. That week included two of the four days of advance polling that set a new record share of one-in-four eligible voters. Most workers would be hiring temporarily much closer to and on the day of the April 28th election and therefore wouldn’t show up in the Labour Force Survey.

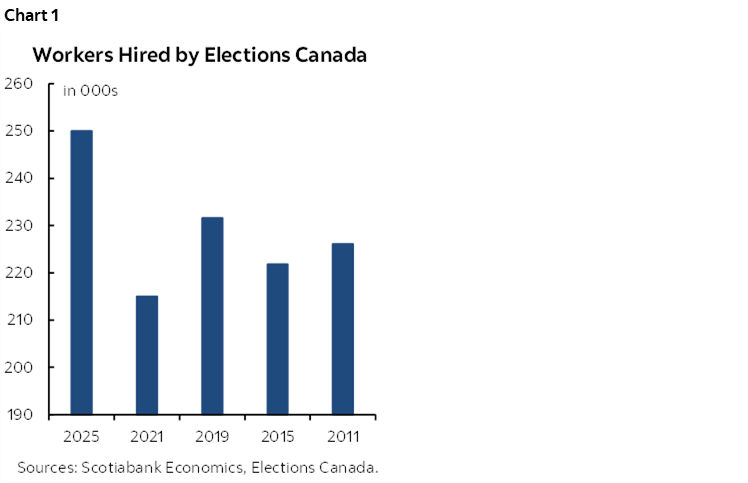

In recent elections, tens of thousands of jobs have been temporarily created to run the election when the reference week included at least two of the advance polling days as it did this year (chart 2).

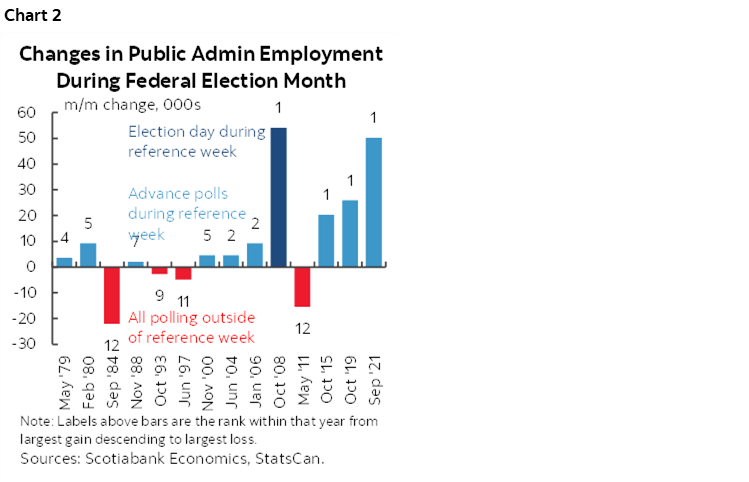

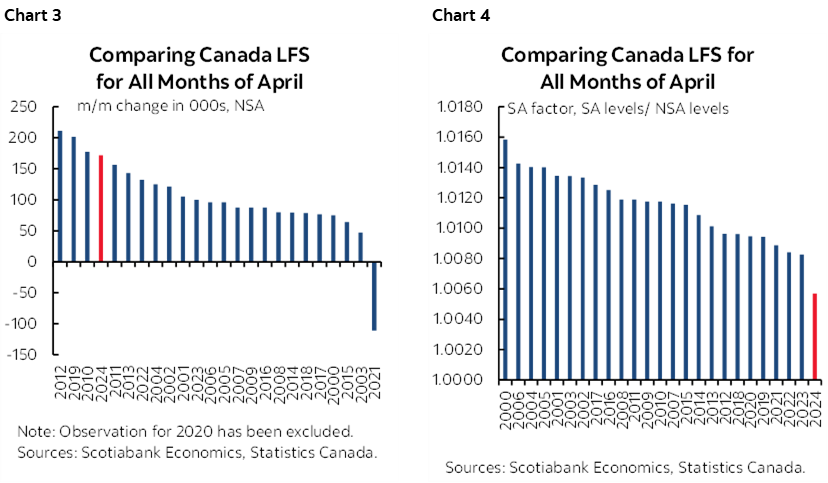

To the downside on this report are two factors plus one uncertainty. One is that while April is normally a seasonal up-month for hiring (chart 3), seasonal adjustment factors could artificially tamp down jobs given the recency bias to how they are calculated. The weakest SA factors for like months of April have all been since 2018 and particularly last year’s weakest on record (chart 4).

Two is that other job market readings have been souring and may points toward weakness outside of election effects and government. Layoff anecdotes have been rising, CFIB small business hiring attitudes have soured, and job postings have been softening a bit.

The uncertainty factor is clearly tariffs. They hit Canada in April. It’s unclear whether tariffs will hit job growth just yet. Tariffs have hit hiring confidence for natural reasons, but a rush to get product out before they are fully binding could support jobs temporarily and the capital:labour ratio to meeting production needs could swing in favour of labour relative to more investment that is tougher to unwind as the toll on the economy mounts.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.