ON DECK FOR THURSDAY, MAY 8

KEY POINTS:

- Risk-on sentiment driven by excess exuberance toward possible US-UK trade deal…

- ...that someone forgot to whisper to UK markets

- Why a possible US-UK deal shouldn’t be viewed as broader trade progress

- China repeats demand for US to drop all tariffs before negotiating

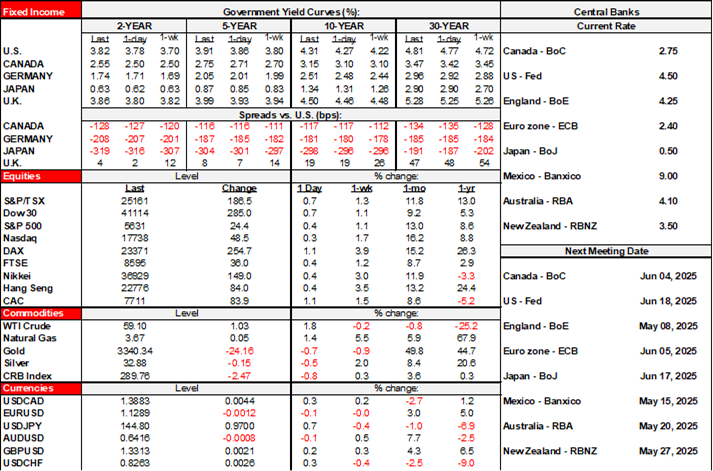

- BoE cuts 25bps, markets didn’t like guidance and split vote

- Three central banks held as expected

- BCRP is also expected to hold

- Q1 US productivity likely sank, while unit labour costs soared

- BoC’s Financial Stability Report due today

Markets are in risk-on mode this morning. Stocks are broadly higher and led by US futures that are up by about 1%+, plus Germany and France gaining by similar magnitudes. Curiously, the FTSE100 is a laggard with a gain of just over +¼% despite being the source of the optimism. Sovereign yields are up by about 5bps across much of the curve in the US and a little less across EGBs, but again, gilts were outperforming the rest before yields spiked after the BoE. The dollar is slightly firmer but sterling’s initial rally overnight as trade headlines hit was then unwound before gaining some ground again post-BoE.

UK-US TRADE ‘DEAL’ SHOULDN’T BE VIEWED AS INDICATIVE OF BROADER PROGRESS

Trump announced that a press conference will be held at 10amET that is widely believed to be some sort of announcement on a trade deal with the UK. If the possible striking of a trade deal between the US and UK is so wonderful, then someone forgot to tell UK markets. One might think that a wonderful deal with the US would buoy outperformance by UK equities. Either that, or it’s really not such a wonderful development. Some believe it’s not a surprise deal struck in clandestine fashion despite Trump’s billing and it’s just the start of deeper trade negotiations.

In any event, in my view, a deal between the US and UK shouldn’t be treated by markets as indicative of a turning of the tide on US protectionism in favour of material deals. For one thing, a deal with the UK is a bit of an exception in that the UK has been seeking a deal with the US since Brexit and has failed to get one ever since.

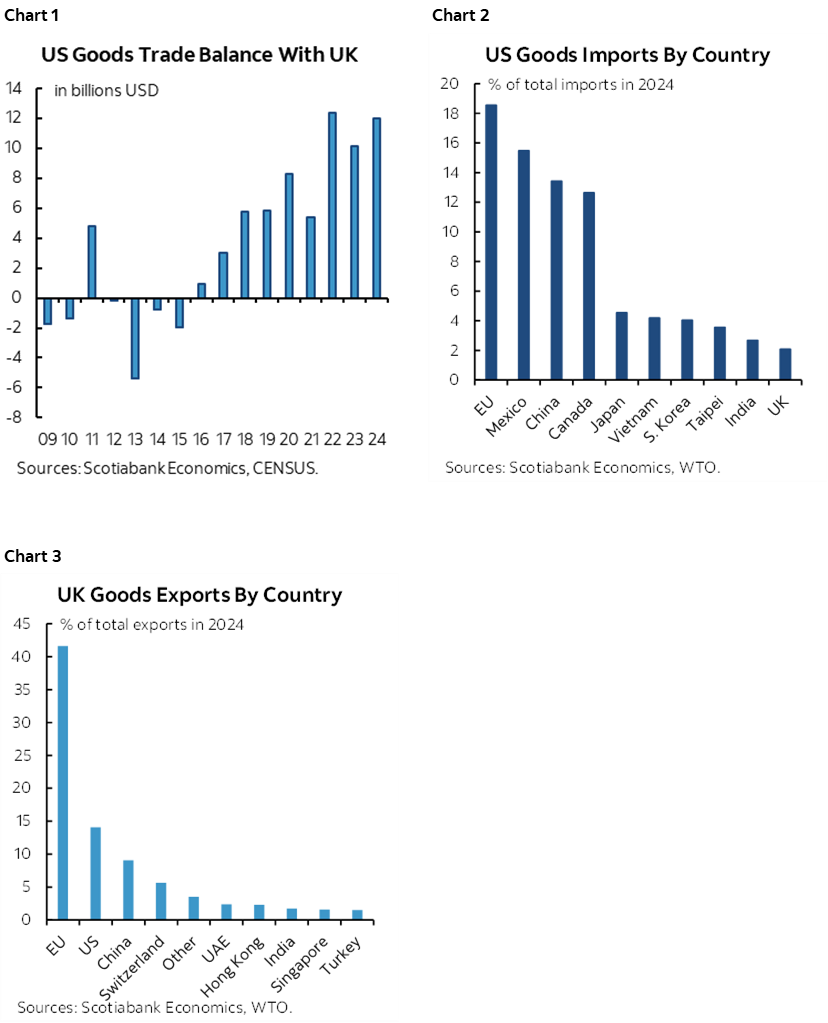

Further, the US runs a trade surplus with the UK using 2024 data (chart 1) and hence it hasn’t been in the same crosshairs of the Trump administration as other countries. Also note that the UK is a relatively tiny player in the US imports market (chart 2) but the US matters more to the UK (chart 3).

Those points mean that a possible US-UK deal shouldn’t be treated as indicative of trade deals with others in the current context. As one example, we have China repeating this morning that it won’t negotiate unless the US first drops all tariffs.

Furthermore, tentative reporting across several services suggests this will be a limited trade deal, not a fully comprehensive one despite what Trump says. We need to see details.

THE BOE STILL CUT AS EXPECTED

Any possible deal did not affect the BoE’s decision one bit this morning. The oscillating cut-hold-cut path was retained by a 25bps cut (statement here). Governor Bailey repeated the ‘gradual and careful’ guidance that indicates a hold may be likely at the next meeting. It was a split decision, however, with 5 voting for –25bps, 2 for –50bps, and 20 for a hold. Markets didn’t like the hold, guidance and split so gilts sold off sharply in the wake of the announcements.

OTHER OVERNIGHT DEVELOPMENTS

German macro releases were constructive, but stale amid forward-looking concerns. Industrial output was up 3% m/m (1.0% consensus). Exports were up 1.1% (1.0% consensus) and revised slightly higher (1.9% instead of 1.8%).

Three other central bank met expectations for holds including Bank Negara (3%), Sweden’s Riksbank (2.25%) and Norges Bank (4.5%). BCRP decides tonight and most expect a hold (4.75%).

US MACRO RELEASES ON TAP

US labour productivity probably slipped while productivity-adjusted labour costs surged in Q1 (8:30amET). Weekly initial jobless claims are also due out at the same time.

BOC’S FINANCIAL STABILITY REPORT

The BoC will release its annual Financial Stability Report at 10amET followed by a press conference at 11amET. This is unlikely to be market moving and the Governor’s practice is to separate its release from discussions on monetary policy considerations.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.