ON DECK FOR WEDNESDAY, MAY 7

KEY POINTS:

- Markets weigh FOMC expectations and China headlines

- PBOC cuts policy rate, reduces reserve requirements

- Bessent’s blindingly obvious realization sets low expectations for China talks

- FOMC to keep policy unchanged today…

- ...as Powell continues to emphasize patience…

- ...that will likely lean against rate cut pricing

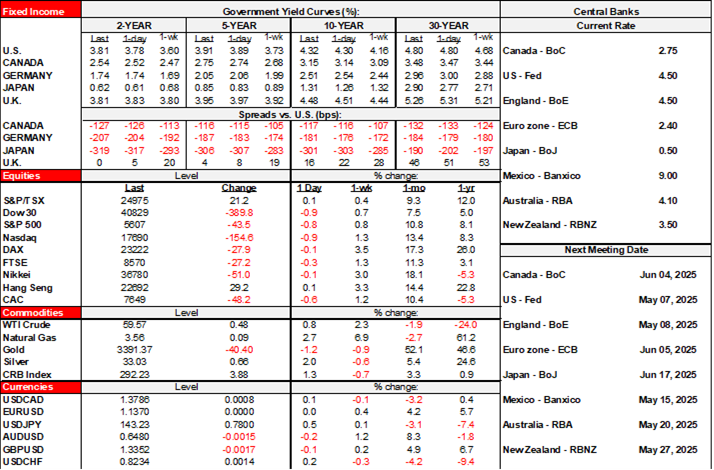

Developments out of China and expectations into this afternoon’s FOMC communications are the main focal points in markets. Risk appetite is mixed with US and Canadian equity futures rallying by over ½% but European benchmarks down by up to ¾%. Chinese equities rallied in response to the PBOC’s moves last evening and trade headlines, but quickly pared some of that initial gain. India’s Sensex was little changed after a further escalation of India-Pakistan tensions. The dollar is slightly firmer. Sovereign bonds are also mixed with mild cheapening of US Ts but mild rallies across European curves. Brazil’s central bank is expected to downshift the pace of hikes to +50bps (5:30pmET).

PBOC EASES MONETARY POLICY

China’s central bank unexpectedly cut the 7-day reverse repo rate by 10bps to 1.4% effective tomorrow and reduced the reserve requirement ratio for large banks by 50bps to 9% effective one week from tomorrow. Both measures have been on sharply downward trajectories for years (charts 1, 2).

Key is the question of signalling. Are the moves toward trade talks (next, below) combined with monetary policy easing relatively positive signals, or, conversely, do they signal that China is easing in order to brace for difficult and lengthy talks that might merely cease escalating tensions?

EXCESS OPTIMISM ON US-CHINA TRADE TALKS

US Treasury Secretary Bessent and US Trade Representative Greer will meet with Chinese Vice Premier He Lifeng in Switzerland in coming days. Bessent set expectations low when he said that the talks will focus upon de-escalation but not a deal. He stated the blindingly obvious when he noted that current tariff rates are unsustainable and that they amount to a trade embargo that halts trade outright. That was obvious from day one. The US administration has seriously mismanaged its trade relationships with all trading partners and massively overplayed its hand.

POWELL TO PUSH BACK AGAINST RATE CUT EXPECTATIONS

Today’s communications only include the statement at 2pmET and press conference 30 minutes later. The next Summary of Economic Projections including a fresh dot plot will be delivered at the June 17th–18th meeting.

I expect the overall tone to continue to reflect patience on the Committee and for Powell to probably indicate that the next meeting would likely be too soon to have enough information to decide upon next policy steps.

No policy changes are expected. Little change is expected in the statement’s wording other than to refresh guidance on roll-off plans after they reduced the monthly redemption cap by $20B to $5B per month and implemented it last month.

As for the presser, I’m expecting Chair Powell to repeat some variant of “we’re not going to be in any hurry to move. We’re well positioned to wait for further clarity.” That’s what he said at the April meeting about this meeting, and he has a case to basically rule out a June cut with similar language. Markets once had about 40bps of a cut priced by June and have backed off to less than 10bps now. That still sounds like too much. Why? Because of data, and there is no reason to alter his stance on forward risks to the dual mandate.

On data, he can point to a still-resilient job market as the unemployment rate remains low at 4.2% after 177k nonfarm payroll positions were created in April.

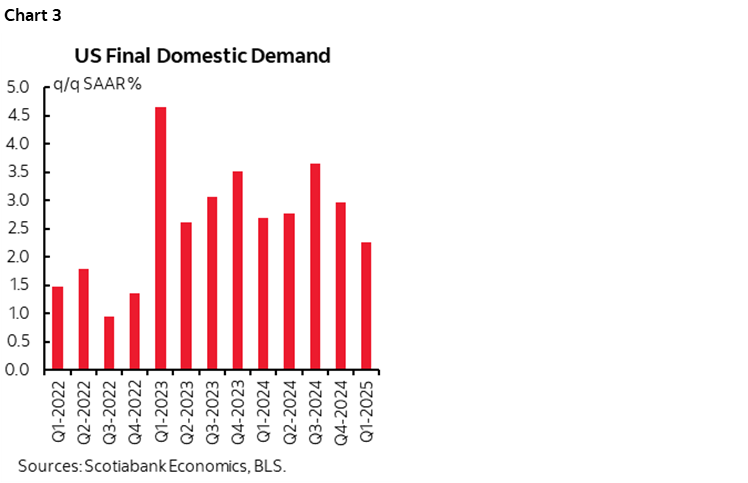

He’s also likely to discount Q1 GDP softness of -0.3% q/q SAAR by correctly noting that it was distorted by tariff front-running with a massive import leakage effect from GDP accounts that knocked about five percentage points off of GDP growth. Instead, he’s likely to point to Final Domestic Demand that remains resilient (chart 3). In essence, final domestic demand continues to grow in excess of potential GDP.

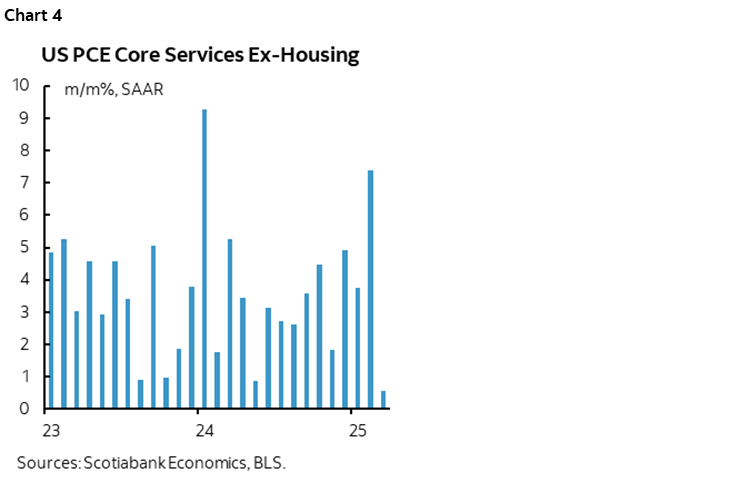

Inflation was soft in March at 0% m/m SA for the preferred core PCE reading, but that’s fresh off readings of 0.5% in February and 0.3% in January and the Committee is likely to smooth through volatile data. The Fed has a particularly close eye on PCE core services inflation ex-housing that has been trending hot before a one-month soft patch (chart 4) while goods inflation is likely to begin taking off effective with the May reading in June.

On forward risks to the dual mandate, I still think arguments laid out a few weeks ago remain valid (here). Powell reinforced them at his April 16th appearance in Chicago.

Tariffs will negatively impact employment while raising inflation. Where the balance between the two lies is highly uncertain. As Chair Powell has noted, the FOMC would respond to a shock that poses conflicting influences on its dual mandate of price stability and full employment by being adherent to what it said in its Statement on Longer-Run Goals and Monetary Policy Strategy (here). Paragraph six spells out how they would act in such an instance:

“The Committee’s employment and inflation objectives are generally complementary. However, under circumstances in which the Committee judges that the objectives are not complementary, it takes into account the employment shortfalls and inflation deviations and the potentially different time horizons over which employment and inflation are projected to return to levels judged consistent with its mandate.”

As Powell put it, “You think about how far each variable is from its goal and how long it would take to get back. Then ask what do you need to do. If one of them is further away, then you would focus on that one.” In plain English, they would dovishly pivot toward easing if job market conditions deviate from their estimated longer-run 4% neutral unemployment rate and broader assessment of labour market conditions more than inflation deviates from their 2% target. By contrast, they would pivot hawkishly if the opposite were to happen. Should the two be in equal opposition to one another, then the FOMC may be forced into a position that does nothing for some time.

Which narrative comes to dominate is an empirical and data dependent matter with significant uncertainty. That’s why Chair Powell recently stated “It’s just too soon to say what would be the appropriate monetary policy response. We’re waiting for greater clarity before considering further adjustments.”

It’s still too soon. It will remain too soon next month. Expect that message to resonate loud and clear once more. Even the relatively dovish Governor Waller does not have a leg to stand on in terms of his bias toward easing should job markets begin to crater as there is no real evidence that’s happening thus far. Waller dissented at the last meeting because the Committee tapered the pace at which maturing Treasury holdings were allowed to run-off but may be regretting that now. He has a habit of mistiming things like when he guided rate cuts by March 2023. No dissenters are expected this time.

Also see the Global Week Ahead’s section on the FOMC here.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.