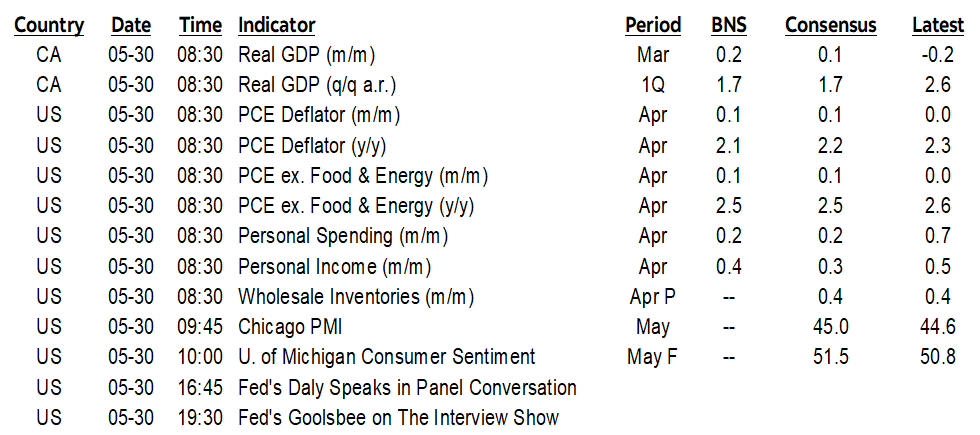

ON DECK FOR FRIDAY, MAY 30

KEY POINTS:

- Mixed markets face data, USTR action, month-end

- USTR could make trade policy announcements today

- Unelected advisors versus unelected judges

- Canadian GDP may be a last chance to finalize next week’s BoC call

- US core PCE inflation expected to be soft

- Another hot Tokyo core CPI reading…

- …versus another probably soft Eurozone inflation reading

A heavy line-up of data releases will combine with possible announcements from the US Trade Representative and Trump on next steps in tariff wars plus month-end effects to make for a potentially lively end to the week. Peter Navarro—the unelected, troublemaking trade advisor to Trump who complains about the power of unelected judges—had advised that USTR announcements may be forthcoming today or into the weekend. There is also a scheduled press conference between Trump and another unelected former advisor, Elon Musk at 1:30pmET, and then another Trump press conference at 5pmET about the US steel deal. All we need are comments from the other unelected, influential advisors, Stephan Miller and Stephen Miller to complete the richness of criticizing unelected judges! This administration is run by folks who never threw their hats in the ring.

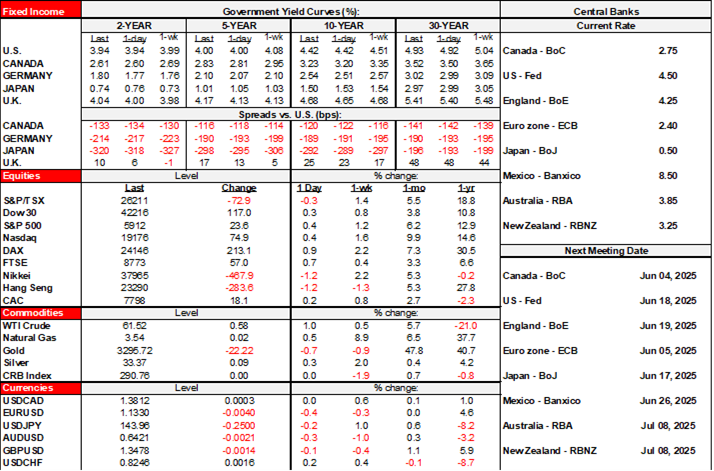

So far, the tentative market action is highly mixed across asset classes. US equity futures are a smidge lower with European cash markets generally higher after a weak session for Asian equities partly due to Bessent’s guidance that trade talks with China have stalled. US Ts are flat while European yields are broadly but gently higher. The dollar is firmer but with some exceptions like the yen on trade concerns and overnight data, and both MXN and CAD that are holding their own ahead of Canadian GDP and maybe on trade hopes.

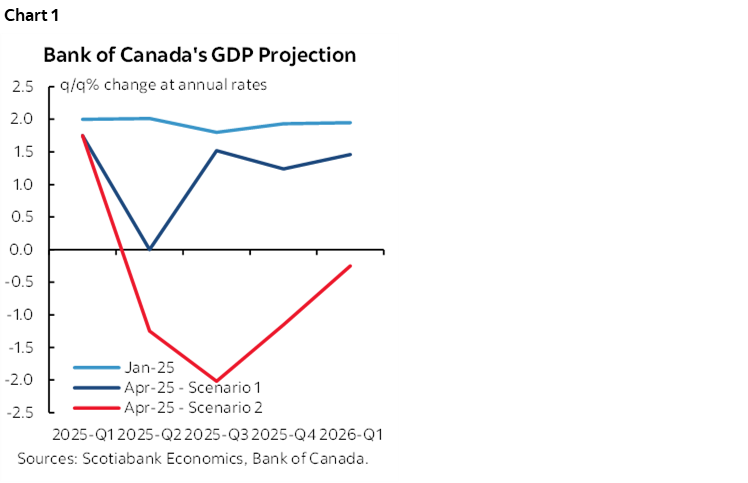

CANADIAN GDP THE LAST BIT OF THE BOC PUZZLE

Canada refreshes a batch of GDP figures that may be the last chance for markets and consensus to reassess expectations for next week’s BoC meeting (8:30amET). Most expect Q1 growth in the 1½% to 1¾% q/q SAAR range.

Hours worked were up 2% q/q SAAR but several activity readings skewed to the goods side of the economy were soft and it will partly come down to services, plus inventory and import swings that will merit a close eye on final domestic demand. Statcan had previously guided March GDP was looking like 0.1% m/m SA and this will be firmed up. April’s tentative ‘flash’ could be decent with a big gain in hours worked and housing starts plus a small election effect among the reasons.

Key, however, will be two things ahead of the BoC next week. One is whether their expectations for Q1 are in the general ballpark of reality and second will be how data informs which of their two scenarios unfolds going forward (chart 1). Recall the BoC skipped a base case forecast in the April MPR in favour of competing scenarios.

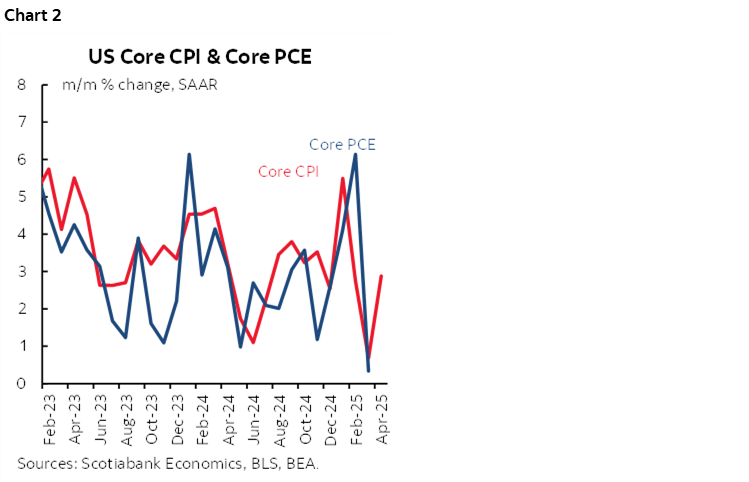

US CORE PCE EXPECTED TO BE WEAK

Today brings out the FOMC’s preferred inflation readings—the price deflators for total consumption and core spending excluding food and energy (8:30amET).

Headline and core PCE prices are expected to be up by 0.1% m/m SA. That would land them both a tick below CPI and core CPI as both core readings have been rather volatile (chart 2). One reason is that a little will be shaved off the CPI estimates by virtue of the different weights used on components in PCE versus CPI. Another reason is that the components from the producer price index that are included in PCE but not CPI will also shave a little off the CPI readings upon translation into PCE.

The year-over-year rates would therefore land at 2.1% for total PCE (from 2.3%) and 2.5% for core PCE (from 2.6%).

A bit of a wrench was thrown into the works by yesterday’s Q1 core PCE revisions. Most had expected the 3.5% q/q SAAR figure to be left flat or revised up a tenth or two but it was surprisingly revised down a tick. We don’t know whether that reflects a downward revision to the way the quarter ended or to an earlier period. This uncertainty could impact the hand-off effect to this morning’s April reading.

Also watch for what are expected to be soft spending figures for April and resilient income growth that month.

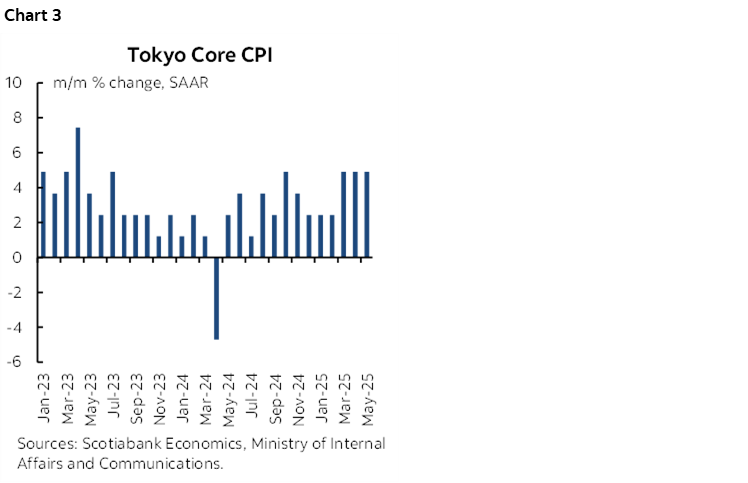

ANOTHER HOT TOKYO CORE CPI READING

The yen ignored another hot Tokyo core CPI reading because of its appeal given volatile US trade policy. Tokyo core CPI was up by just shy of 5% m/m SAAR for a third straight month (chart 3). Other readings mixed including industrial output (-0.9% m/m, -1.4% consensus) and retail sales that met expectations at +0.5% m/m while housing starts fell by more than expected.

SOFT EUROZONE CPI REAFFIRMS ECB CUT PRICING

It’s shaping up to be another soft month for Eurozone CPI that merely reaffirmed expectations for another ECB cut next Thursday. The pan-eurozone figures will be released on Tuesday, but here are the figures for the individual countries:

- Italian CPI was up 0.1% m/m and on consensus.

- Spanish CPI was weaker than expected (-0.1% m/m, 0% consensus) with core dipping by more than forecast (2.1% y/y, 2.4% prior, 2.2% consensus).

- German CPI inflation will probably land weaker than the expected 0.1% m/m rise when the national numbers come out a little later this morning (8amET). That’s because the individual states reported soft readings; three were at 0% m/m, one was at 0.1%, one fell by -0.1% and another was up 0.2%.

- We also learned a few days ago that French CPI was weaker than expected at -0.2% m/m (+0.1% consensus).

OTHER OVERNIGHT READINGS

Adding to the dovish Eurozone implications was a soft reading for German retail sales volumes (-1.1% m/m, +0.2% consensus) but much of the miss was explained by revisions to the prior month that was revised up by 1.1% to +0.9%.

The won is among the weakest performers to the USD this morning in the wake of trade uncertainties and a weaker than expected print for industrial production in April (-0.9% m/m, +0.5% consensus).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.