ON DECK FOR THURSDAY, MAY 29

KEY POINTS:

- Moderate risk-on sentiment driven by trade ruling, tech earnings

- US federal court strikes down use of IEEA tariffs…

- …but a lengthy appeal process lies ahead…

- …and so does a possible game of Tariff Whack-a-Mole

- The effective average tariff rates just plummeted

- End game: Other countries’ retaliatory tariffs could go down, but why negotiate now?

- If tariff de-escalation sticks, Canada is at risk of overdoing it on fiscal policy…

- ...as an added reason for a neutral/hawkish policy bias at the BoC

- Nvidia’s earnings are helping 6% of the S&P

- Canada’s big bank earnings season wraps up

- BoK cut, SARB may be next

- US core PCE inflation may be revised up within GDP revisions

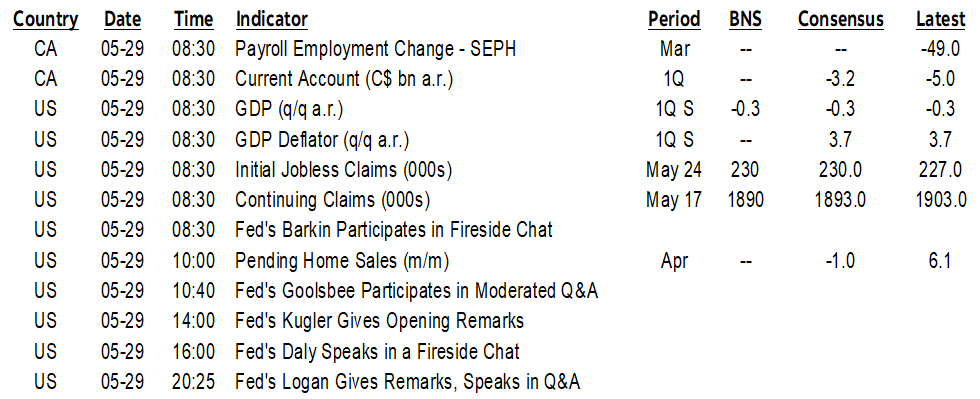

- US pending home sales, Canada’s stale payrolls survey on tap

- US to auction 7s this afternoon

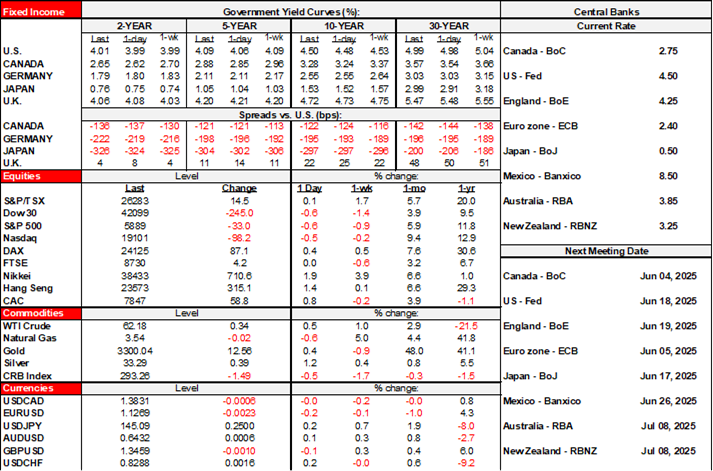

Yesterday was a nasty day for Taco man and markets are liking it, but not exactly loving it. A positive step against Trump’s insane tariffs was undertaken but raises further questions and uncertainties as well as a potentially complicated set of knock-on effects that I’ll explain. US equity futures are up by about 1% or a little more for the Nasdaq and benefiting from last evening’s trade ruling but also from Nvidia’s earnings after the close given its 6.3% weight in the S&P500. TSX futures are up by ¼% and European cash markets are mostly rallying by ¼% to ¾% except for London that is flat. Sovereign bond yields are under mild upward pressure across maturities in the US and Canada but are little change across EGBs and the UK except for a small decline in the gilts front-end. The dollar is mixed but currency moves are generally small. Gold is little changed and oil is up a few dimes.

TARIFF WHACK-A-MOLE MAY BE ABOUT TO BEGIN

I’ll reiterate key points made during last evening’s coverage of the US trade court ruling for staff and clients.

What happened is that the US Court of International Trade—a federal court—ruled that Trump’s use of International Emergency Economic Powers Act provisions to impose tariffs under fabricated emergency conditions while bypassing Congress exceeded his legal authority and ordered them to be “vacated,” meaning there is an injunction against using the Act to impose tariffs again. The full ruling is available here. This ruling strikes down the ‘Liberation Day’ tariffs against countries all over the world and also strikes down Trump’s ‘fentanyl tariffs’ against Canada, Mexico and China. An accompanying order stipulates that the US administration has ten days to stop collecting tariffs, unless the appeal process lengthens this period.

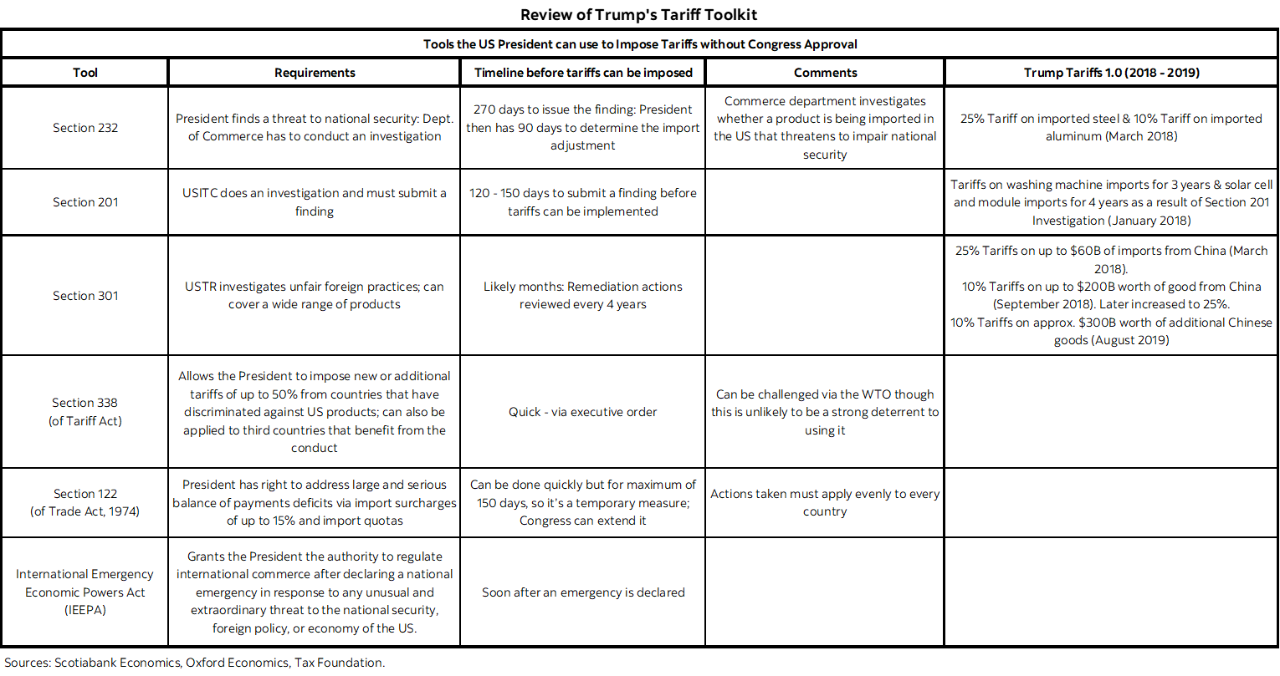

A first point of caution that I immediately flagged last evening is that the IEEPA is only one tool that Trump can use to impose tariffs while bypassing Congress. He has used other measures and that means some key tariffs will stick. He used a different tool, Section 232 of the Trade Expansion Act, to impose his tariffs on autos and steel and aluminum and they stick for now. He has used Section 201 provisions in the past to impose tariffs on washing machines and solar panels. Section 301 provisions have been used to impose tariffs on China and tariffs on China have also used IEEPA and Section 232 provisions.

A second point of caution is that the US administration has already said it will appeal the federal court ruling. That could take quite a while given how slow the US courts operate which means uncertainty remains high. That could mean that cancelling collection of the tariffs may be suspended as the appeal is considered.

A third point is that if the appeal fails, then this is probably going all the way to the Supreme Court. Who knows along what timeline this may occur, but given the importance of the issue and the money being collected (ultimately from US businesses and consumers) it may be expedited. I'm not familiar with the process around how that could be done. The Court is done with its normal process of hearing oral arguments in cases (April), goes into recess by late June and returns in October. Ergo, if it goes this route, then it could be several months before the Supreme Court weighs in.

Fourth, we could be embarking upon a game of Tariff Whack-a-Mole in which Trump shifts around the tariff tools he is using. Can’t use IEEPA? Fine, I’ll use the other tools summarized in chart 2. There are, however, seven other lawsuits plus other forms of opposition such that it’s possible further court rulings limit or rule against use of those other tools as well. We could be chasing a lot of executive orders that would be conversion announcements that shift tactics as the administration and the courts engage in this dance. The problem with this approach is that it could turn into a game of tariff whack-a-mole; as soon as they convert from IEEPA tariffs to use some other tool, another court could issue another ruling against that other tool and so on.

Chart 2

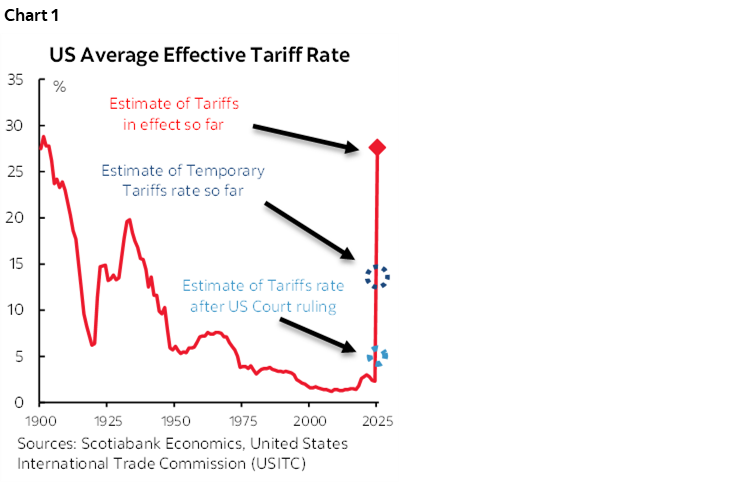

Fifth, what effect could this have on the effective average tariff rate on all US imports and specifically Canada and Mexico? John McNally in our group has some tentative calculations to consider. He figures the tariff rate on Canadian total exports now drops by 1.2 ppts to 2.6%, while the tariff rate on Mexico’s exports drops by 2.3 ppts to 2.0%. The tariff rate on all US imports drops by 7 ppts (8.6% if just goods) to 4.2% (5% if just goods). As chart 1 shows, this would be a massive de-escalation from the peak tariff rates that Trump’s earlier actions had imposed that had hit 27% for the highest rate since 1904 but is now potentially a fraction of that. Any hike in tariffs is unhelpful and without justification in my opinion, but we’re now looking at relatively minor effects.

Sixth, it’s a heck of a time to be a forecaster, but if this ruling sticks and depending upon the course of actions from here, then the risk of recession in the US and Canada has been sharply reduced.

Seventh, if this is a real de-escalation of tariff wars that is being triggered by the US courts and it sticks, then it could be impactful to other policy debates. For instance, the Carney administration in Canada may be at risk of overdoing it on fiscal policy. If so, then it’s added reason for the Bank of Canada to sit on its hands for now and merely observe.

Eighth, while it’s likely to take time for this next point to unfold as other countries wait out the process unfolding in the US courts, there could be two knock-on effects. One is that other countries could ultimately lower their own retaliatory tariffs which mainly means China given it has had the most aggressive counter-punch to date. Two is that other countries might be less motivated to negotiate trade deals with the US administration and therefore they could drag their heels.

EARNINGS—NVIDIA AND CANADIAN BANKS

Nvidia’s results after yesterday’s close are helping to buoy market sentiment. EPS was US$0.96 (consensus 93) and the general impression is that its results and guidance were more resilient than expected in light of US-China tensions.

Canada’s quarterly bank earnings season is also wrapping up with CIBC beating (EPS $2.05, consensus $1.88). RBC missed expectations (EPS $3.12, consensus $3.18) yet increased its divided by 4% and introduced a buyback plan for 35 million shares.

REGIONAL CENTRAL BANKS WEIGHING IN

The first of a pair of regional central banks cut 25bps last evening (Bank of Korea) and the other may join with its own 25bps cut this morning (SARB, 9amET)).

US CORE PCE MAY BE REVISED HIGHER

US Q1 GDP revisions may be more about what happens to core PCE revisions (8:30amET). Based on monthly revisions, I think core PCE could get bumped up a tick or two from 3.5% q/q SAAR. No conviction around possible revisions to the initial estimate of -0.3% GDP; nor does it matter in the face of forward-looking developments.

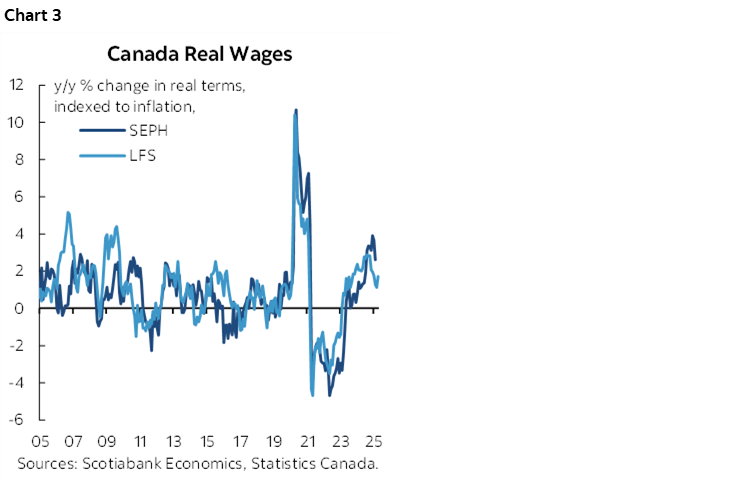

The US auctions 7s this afternoon (1pmET). We’ll also have US pending home sales in April (10amET), weekly initial jobless claims (8:30amET) and Canada’s lagging SEPH payrolls report for way back in March (8:30amET) to consider but next Friday’s Labour Force Survey for May will be the thing to watch after the BoC. Watch the wage figures from both measures as Canada continues to register real wage gains (chart 3) despite poor trend labour productivity.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.