ON DECK FOR TUESDAY, MAY 27

KEY POINTS:

- Global long-ends buoyed by Japan’s MoF…

- …as BoJ’s Ueda digs in on the front-end

- US equities return from holiday to rally in lagged reaction to tariff delay

- Gilts front-end cheapens on sign of issuance shift

- BNS announces share buyback, dividend hike

- Canada’s Speech from the Throne

- US durables, consumer confidence on tap

- French CPI lands weaker than expected

- Global Week Ahead reminder here

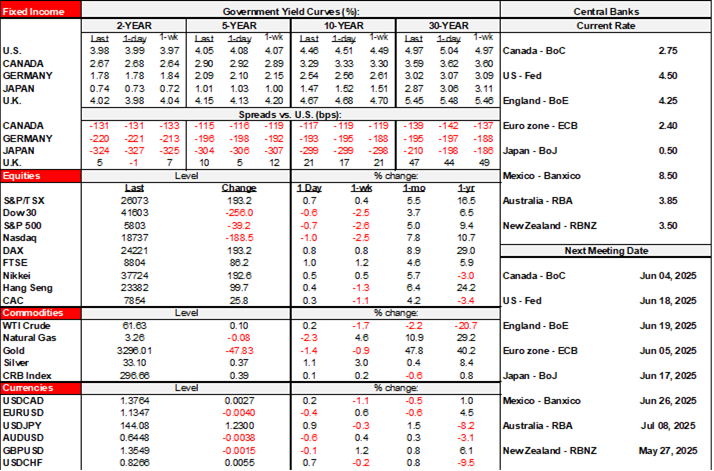

It’s all about the long end this morning and thanks to Japan. Sovereign curves are bull flattening globally with Japan as the epicentre (see below). The dollar is broadly stronger with the yen among the weakest crosses while potentially impactful US data lies ahead. Stocks are rallying with US futures up 1½% and also in delayed reaction to Trump’s postponement of his 50% tariff threat on the EU as US markets come back from the Memorial Day holiday. Milder rallies are occurring across most other equity benchmarks that had already factored in the tariff news. Softer French inflation didn’t hurt and watch market reaction to BNS’s higher divided and stock buybacks. The gilts front-end is underperforming after an FT report indicated a shift toward short-term issuance (here).

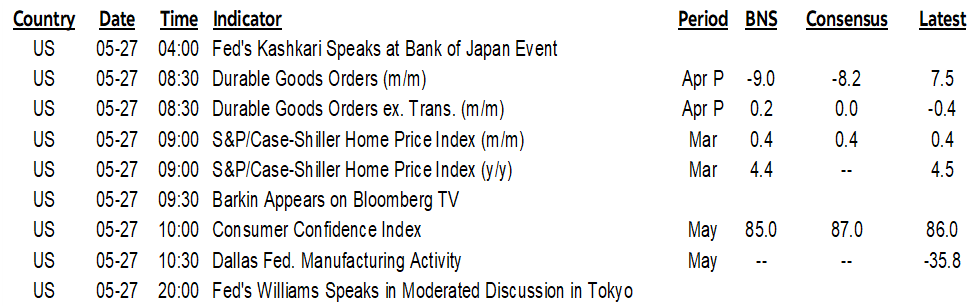

JGBS CURVE BULL FLATTENS ON MOF HINT, BOJ’S UEDA

The JGBs long-end is the key mover on the day as 30s rallied by 19bps and 10s were 5bps richer (chart 1). That’s motivating carry influences into other long-ends such as the US 30-year yield that’s down 7bps this morning. The yen is the worst performing cross against the dollar on a generally strong session for the USD. The catalyst is a sign from the Ministry of Finance that Japan is considering a decrease in long-bond issuance given recently tepid demand and rising yields. The reason for such speculation appears to be traced back to a questionnaire sent by the MoF to market participants asking for views on issuance and market conditions which was treated as unusual. The damage being done by the US government to the long-end took Japan to rein it in somewhat.

The JGBs front-end was anchored, however, after BoJ Governor Ueda dug in on relatively hawkish rate guidance by reaffirming he thinks Japan is on the longer-run path toward achieving its sustainable 2% inflation goal. Still, markets don’t have a full 25bps hike priced this year with about half a hike priced by October and a little more priced for the December meeting.

BNS ANNOUNCES BUYBACK, DIVIDEND HIKE

BNS (my employer) was the second of the Canadian banks to report this morning. Key was that it announced a buyback program of up to 20 million shares and raised its dividend 4% to C$1.10. Adjusted EPS was C$1.52 (consensus $1.56). Revenues slightly beat at $9.08B with adjusted ROE close to estimates at 10.4% (consensus 10.5%) but provisions were higher than expected at $1.4B (consensus $1.34) amid forward-looking risks to the economy.

CANADA’S SPEECH FROM THE THRONE

Canada’s Speech from the Throne will be delivered in Parliament by King Charles III at about 11amET for 20–30 minutes. It will lay out some of the high-level priorities for the Government to open a new session of Parliament.

OVERNIGHT DEVELOPMENTS

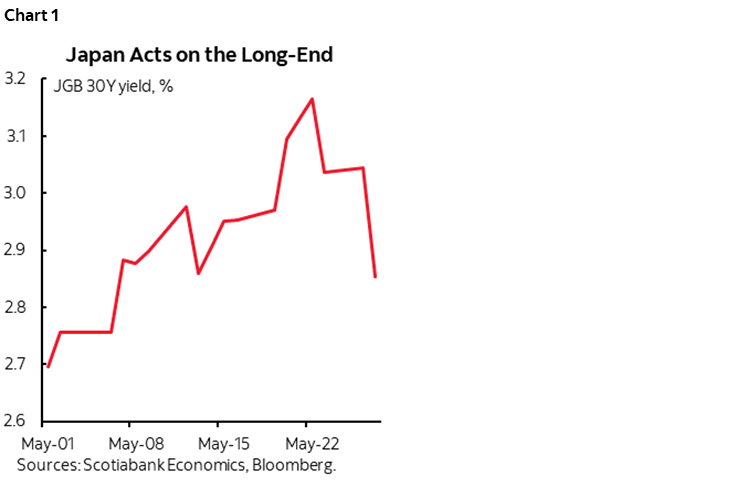

French CPI surprised lower at -0.2% m/m NSA (+0.1% consensus) which pulled the y/y rate down to 0.6% (consensus and prior 0.9%). Even though that’s not seasonally adjusted, it was the lowest m/m reading on record for like months of May (chart 2). Services were soft at -0.2% m/m, but the main driver was another 1½% m/m drop in energy prices. That drew a reaction from Banque du France Governor Villeroy who said it’s “another very encouraging sign of disinflation in action. So the normalization of monetary policy is doubtless not complete and we could—in the conditional—see this at our Governing Council Meeting next week.”

German consumer confidence was stable in the latest reading (-19.9, -20.8 prior) and has been floating around present levels since about mid-2024.

US DATA ON TAP

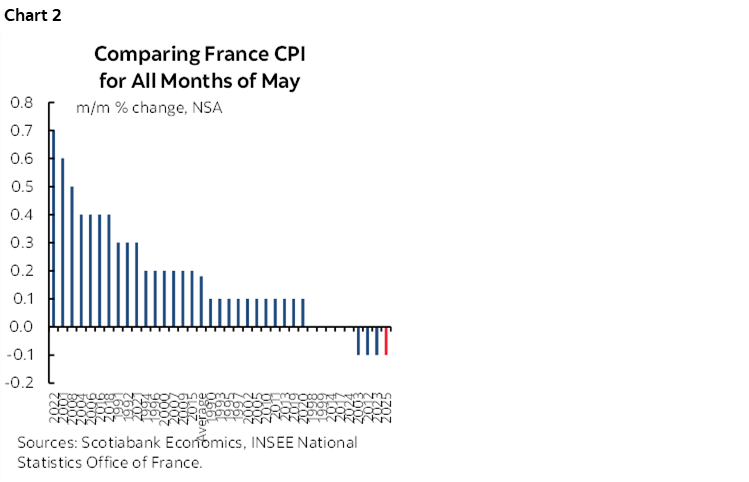

A trio of US macro readings lies in store for this morning’s markets. Durable goods orders are expected to reverse much of the prior month’s surge that was fed by plane orders as they fell back in April (8:30amET). Key will be core orders ex-defence and air as a gauge of underlying business investment and in light of a volatile but generally upward trend (chart 3).

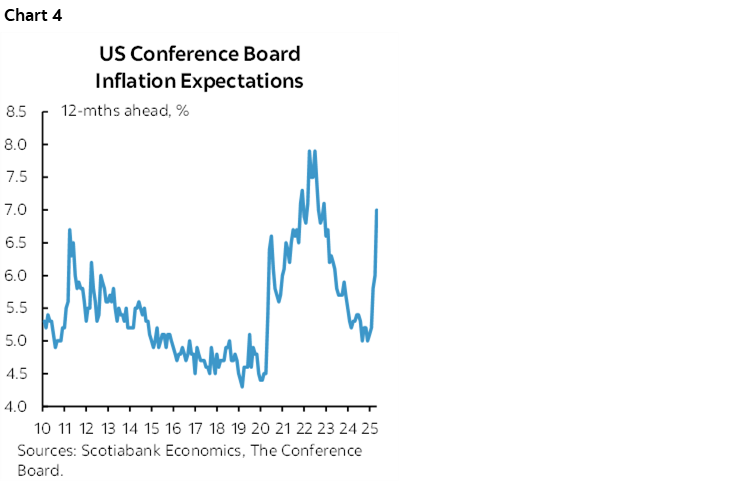

US consumer confidence in May could be more important to markets and has been riding at the lowest reading since May 2020 (10amET). Watch inflation expectations (chart 4). Also due out are house prices for March (9amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.