ON DECK FOR FRIDAY, MAY 23

KEY POINTS:

- Trump slams equities as he escalates trade wars again…

- ...with a threat of 50% tariff against EU starting June 1st…

- ….that is sure to provoke retaliation...

- ...and by threatening a 25%+ tariff on iPhones…

- ...while make the US less and less welcoming to foreigners

- Tariff pass through in the US isn’t just a Walmart thing

- Trump has killed the dollar as a safe haven

- EU negotiated wage growth cools

- UK retail sales smash estimates

- Canadian consumers continue to spend

- JGBs underperform on CPI

- US new home sales probably fell

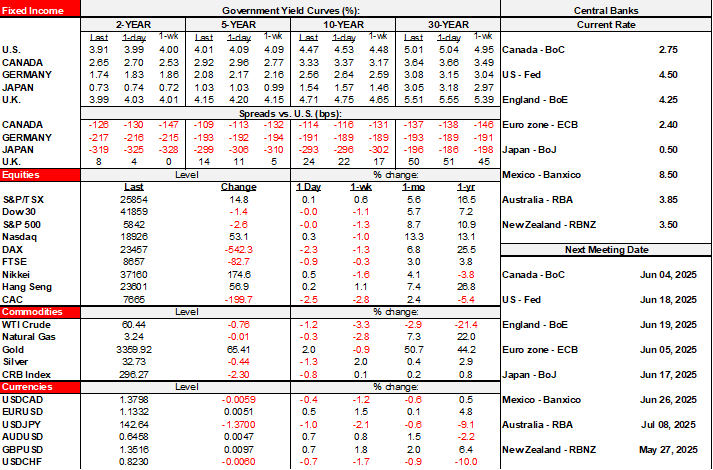

The dollar is broadly weaker against major crosses as sovereign yields decline across maturities and markets. The dollar is not playing the role of safe haven as risk appetite sinks but so is the dollar which is a strong warning to the US. Higher inflation risk and uncertainty toward the basis are messing up covered interest parity math for international investors in dollar assets. US equity futures are down by over 1.5–2% with European cash markets falling by more than that. Gold is up by over US$50/oz. Oil is down about 1%.

Key is that Trump escalated trade wars again in a series of social media posts where he prefers to conduct policy. The EU and Apple are his targets. Otherwise, we’re just left with a sprinkling of generally stale data releases to consider. The US fiscal morass will be bogged down in the Senate for weeks to come and will ultimately look very different from the garbage that passed as a plan in the House.

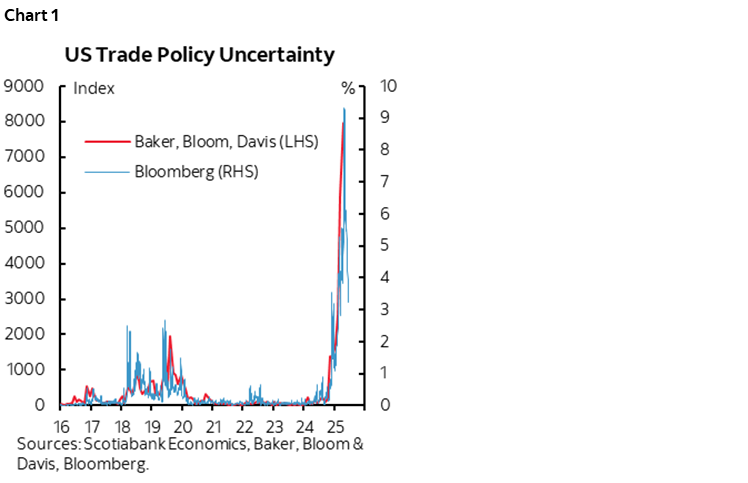

UNCERTAINTY REMAINS HIGH AS US CONTINUES TO PRACTICE SELF-HARM

BoC Governor Macklem remarked yesterday that uncertainty has declined. He spoke too soon. Chart 1 kind of backs him up in one sense by juxtaposing a monthly measure up to April alongside a daily measure up to the present. I think the decline in the daily measure is exaggerated and a narrow reflection of uncertainty. It’s also about to shoot way back up again in the wake of this morning’s remarks by Trump. Further, look at confidence gauges and you’ll see what I mean; consumers and businesses are not so convinced that uncertainty is down. Macklem should also have a look at this latest evidence of tariff pass through at US businesses, how it’s not just Walmart, and the likely spillover effects into Canada through supply chains.

We remain on a knife’s edge as not a day goes by without the US administration practicing self-harm against US interests and taking the world down with it. From tariffs to irresponsible fiscal profligacy, to destroying the value of the US signature on international agreements it has signed, and to debasing the dollar’s credibility, great damage has clearly been done. The evidence continues to mount.

Trump warned this morning that if Apple doesn’t make its iPhones in the US, then he will impose a 25% tariff on them. Apple’s share price plunged. iPhones would be prohibitively expensive if made in the US where manufacturing costs are simply uncompetitive.

More important is that this further showcases how volatile Trump is. Nothing he says on trade policy can be taken to the bank as it always depends upon how his mood shifts, what he seeks to detract attention away from, and perhaps when he wants to make it clear he’s the boss.

Trump also threatened a 50% tariff against the EU starting June 1st given that trade negotiations are going nowhere. The EU is likely to retaliate as they had previously warned that absent traction toward an agreement they would respond more forcefully. Watch for further headline risk. The Trump administration fundamentally misjudged the EU that never acts in unified fashion which limits its negotiating abilities especially in the face of constant threats.

Enter exhibit three in this entry. It’s about the all-out assault on foreigners that makes the US rather unwelcoming. Whether for employment, studying, or vacationing, one has to re-think travel in any form to the United States given a combination of immigration rule changes, harassment and frankly petty moves. The effects could be lasting for years to come.

The latest is the assault on 1.1 million international students studying at US universities. They make up an estimated 6% of all students at US universities and colleges but more than a quarter of students studying at the graduate level and especially at the best universities. Their numbers have already been on the decline (here). The actions against international students at Harvard are mean, petty, and disproportionate to the concerns. Ditto for the warning against Colombia University. They are a blow to the ability of the US to attract the best and brightest from all over the world. It’s also a gift to foreign universities in Europe, Canada, and elsewhere that will motivate a brain drain away from the US. To compensate for problems in its own K-12 educational system, the US relies upon foreign student enrollment and the hope that many of the students will stay once their studies have been completed. Cutting off this supply chain will dent innovation and prosperity in America and damage faith that the US is a safe, secure and welcoming nation. The perpetrator is Kristi Noem acting on behalf of Trump and known for stomping on the Canada-US border, harming animals, and photo ops from foreign prisons. I’ll leave it to you to look up Ms. Noem’s rather limited education.

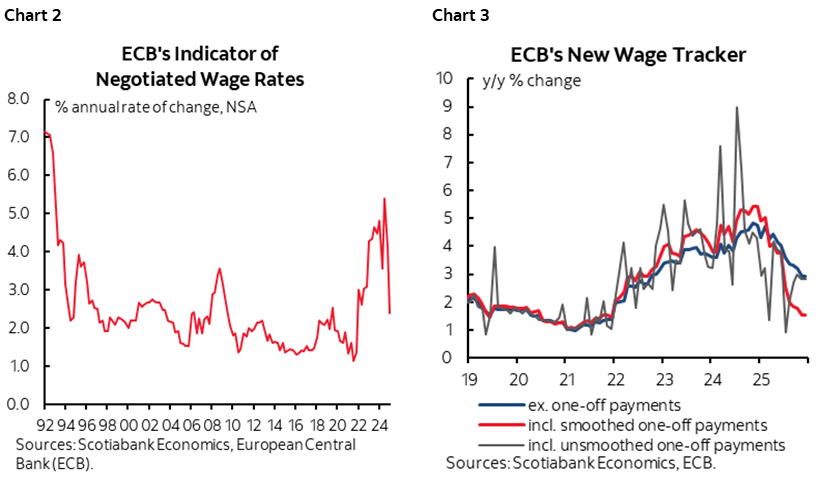

EU WAGE GROWTH COOLS, REAFFIRMING ECB CUT PRICING

EU negotiated wage growth slowed sharply in Q1 data released this morning. From 4.1% y/y in 2024Q4, it slowed to 2.4% in 2025Q1 which is the slowest rate of increase since 2021Q4 (chart 2). The measures that track future wage agreements and estimates wages through to December of this year are also cooling (chart 3). Following the data, ECB Chief Economist Philip Lane said “So we are confident services inflation will come down.” There was minimal market reaction relative to what was already priced by way of an expected further 50bps of ECB cuts this year that would take the policy rate down to 1.75%.

UK RETAIL SALES STRONGLY BEAT, MARKETS IGNORED

UK retail sales volumes strongly beat expectations for the month of April and drove mild underperformance of short-term gilts relative to other global benchmarks. They were up by 1.2% m/m which was four times consensus. Ex-gasoline they were up 1.3% (consensus 0.1%). Breadth was soft. The main driver was a 3.9% m/m jump in sales at food stores that rebounded from the prior drop. Non-food store sales fell -0.7% as clothing and footwear fell 1.8%, ‘other’ stores fell 3.1%, but gains were posted by household goods (2.1%) and non-specialized stores (2.8%).

CANADA TO REFRESH RETAIL SALES

Canadian consumers continue to spend. March nominal retail sales were up 0.8% m/m SA which is a tick above prior guidance from Statcan. In volume terms, sales were up by 0.9% m/m, indicating a touch of retail price softness. Advance guidance for April’s sales points to a further nominal rise of 0.5% m/m, but never includes any details.

Canadian March GDP is looking like it was up 0.2–0.3% m/m, compared to earlier flash guidance it would be up 0.1. April is looking like another 0.3%. We’ll get those numbers next Friday. That suggests Q1 GDP at 1.7% q/q SAAR and very tentatively provides tracking at a similar pace for Q2 based on limited known info to date. That's an economy that prior to tariff effects going forward was growing at about potential.

There remains a serious disconnect between sentiment toward the Canadian consumer and select anecdotes from individual retailers, versus the data. That’s true at least up to now, with obvious forward-looking risks. Real consumption growth in q/q SAAR % terms was up 3.6% in 2024Q1, then 1.0% in Q2, then 4.2% in Q3 and 5.6% in Q4. Now 2025Q1 is likely to be weak based on retail sales volumes but probably somewhat offset by services spending. So far, 2025Q2 looks poised to sharply rebound but with a lot of data and risk ahead (chart 4). And it's not just tariffs. It's also the fact we're all still ice blocks around here as this month of May is the coolest May in decades. Seasonal sales like at garden stores, patios, building supply stores etc have got to be reeling this month.

US NEW HOME SALES LIKELY TO REVERSE PRIOR GAIN

The US will just release new home sales for April that are expected to fall after the prior month’s surge that was disconnected from the weak trend in model home foot traffic (10amET). Just wait until tariffs hit building costs alongside high mortgage rates and job market uncertainty.

JGBS UNDERPERFORM POST-CPI

JGBs underperformed other global benchmarks overnight after April CPI was a smidge firmer than expected (3.6% y/y, 3.5% consensus). The greater vulnerability is likely to be May’s Tokyo CPI reading and whether the core measure extends the recent pattern of very strong rises.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.