ON DECK FOR THURSDAY, MAY 22

KEY POINTS:

- Risk-off sentiment continues

- US House passes a Bill that adds to structural deficits and fiscal largesse

- Trump 2.0 warnings have been on the mark

- What’s in the House Bill

- Global PMIs were generally soft

- BoC’s Macklem, Gravelle on tap

- Canada’s bank earnings season is off to a solid start

- What prompted yesterday’s market actions ahead of another auction today

- US home sales due out, claims held steady

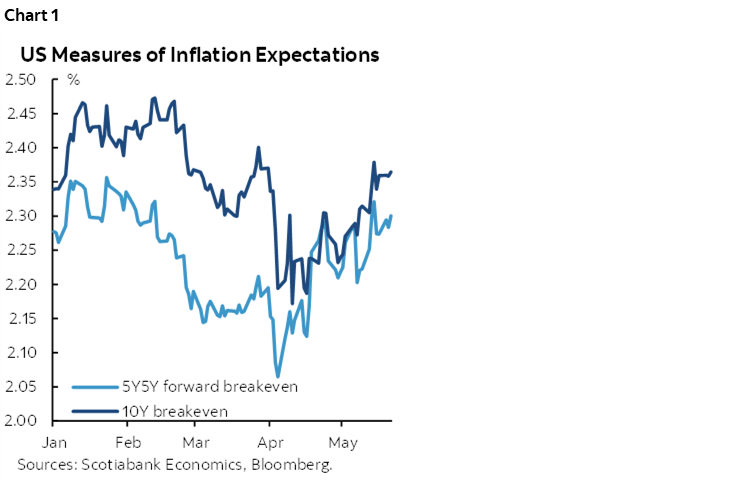

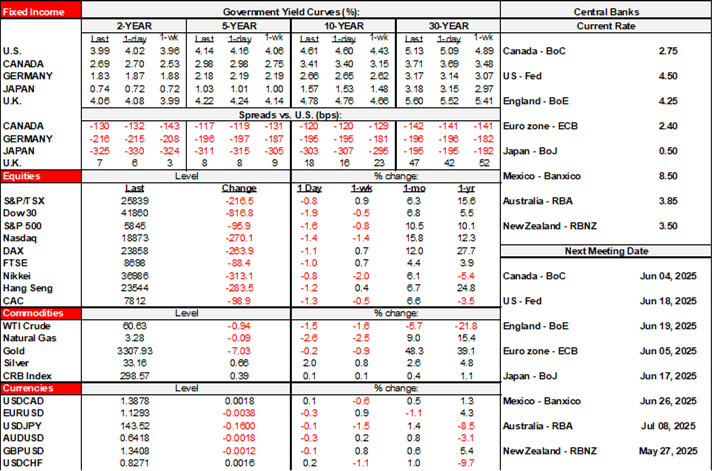

Global equities continue to sell off in the wake of more US fiscal largesse and following yesterday’s weak 20-year Treasury auction. US equity futures are down about half a percent while European cash markets are down by over 1% following widespread red ink across Asia-Pacific bourses. Sovereign bond yields are mixed but cheapening again at the longer ends everywhere. The dollar is slightly firmer except against the yen. Oil is off a buck. Powell’s comfort in anchored inflation expectations should be waning (chart 1).

An ongoing concern is the sea of red ink that the US is running. See the next section on the House bill. A wave of global PMIs didn’t have much influence on markets. TD Bank beat expectations, and there will be BoC communications later today. The US auctions 10-year TIPS as another possible test of market appetite for debt and inflation risk.

US HOUSE BILL PASSES, ADDS TO FISCAL LARGESSE

The US House voted in favour of a budget reconciliation bill by a one-vote 215–214 margin this morning. The House was deeply divided mostly along party lines with a couple of GOP members voting against. The next hurdle is the Senate which is expected to be a long and arduous journey and resulting in committee mark-ups before anything goes to Trump’s desk for his signature.

The vote followed more concessions that were made overnight including higher SALT deductions and deeper cuts to Medicaid. There is nothing beautiful about a bill that deepens US fiscal largesse and further postpones the need to pursue reform of its unsustainable debt path.

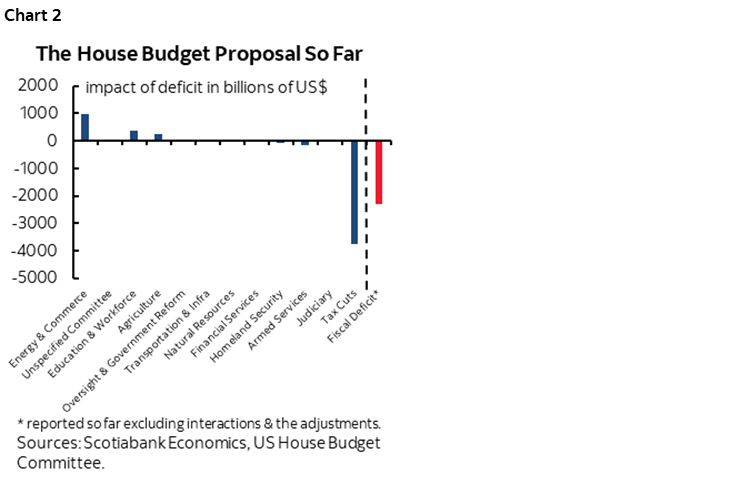

Key elements of the House bill are highlighted below and see chart 2. Also see this post from the Committee for a Responsible Budget that is mostly up to date except for the relatively minor impact of the changes introduced early this morning. Overall, it amounts to more debt, bigger structural deficits, unwise tax policy distortions and even at that it's not including up to half a trillion for Trump's 'Golden Dome' which means that the true deficit and debt projections would be considerably higher over time. There is nothing substantive on infrastructure, it's all about funding tax cut extensions.

In short, the US is a fiscal basket case that the bond market, the Fed, and the dollar are sterilizing which is exactly what I argued would happen in my pre-election pieces such as this one that strongly warned about his tariffs, his immigration policies, and the market effects of his fiscal plans under Trump 2.0 that is set against very different conditions than under Trump 1.0.

- The debt ceiling goes up by US$4 trillion to $40T. The CBRE estimates that debt will go up by $3.1T over the next ten years toward US$40 trillion. Defence spending not included in the Bill could have them returning for another debt ceiling increase. Recall Trump railing against higher debt when he was out of office.

- There is a $2.3T increase in cumulative deficit over 10 years from a baseline projection. That is driven by the loss of $3.49T of tax revenues only partially offset by $1.18T of spending cuts. Tax cuts don’t pay for themselves

- $3.8T of tax cuts mostly extending the TCJA provisions that would have otherwise expired at the end of this year. This is very mildly offset by other revenue measures.

- no tax on tips and overtime with distorting effects on labour markets. Employers face greater incentive to shift more pay in affected industries toward tips away from wages. Not taxing o/t could encourage more shirking during regular hours and damage productivity.

- SALT deductions are increased to $40k from $10k for households earning up to $500k and increased by 1% per year for 10 years. That’s a highly regressive measure that reduces the incentive for high spending and high tax states to pursue fiscal reforms of their own.

- Auto loan interest is deductible which is as bad and distorting policy as mortgage interest deductibility. It will further distort the composition of household debt toward auto loans at the expense of other revolving and nonrevolving credit products.

- The bill introduces an 80 hour per month work requirement for Medicaid benefits and tighter requirements. The CBO estimates that another 8.6 million Americans will lose access to health care.

- Clean energy tax credits are being phased out.

- There is a $1k increase in the standard deduction to $16k for individuals and a $2k increase to $32k for joint filers.

- The estate tax exemption increased.

- A new 'Trump' account will contribute $1k for babies.

- $46.5B for deportation and wall funding with a target to remove 1 million immigrants annually that slows population growth.

- A small downpayment on the 'Golden Dome' of $25B with full cost estimates not included in the bill but estimated by the CBO to be anywhere from about $160B to over half a trillion.

GLOBAL PMIS

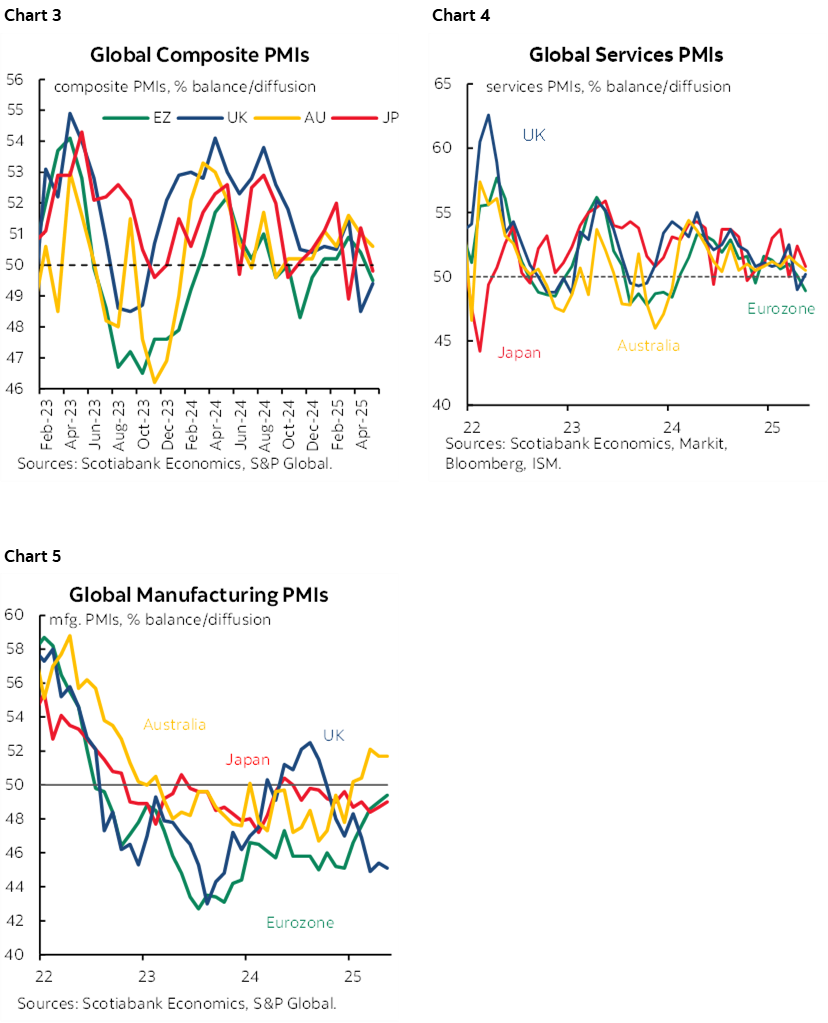

The monthly onslaught of global PMI measures unfolded across major markets with the US still ahead. See charts 3–5.

- Australia’s composite PMI slipped four-tenths to 50.6 entirely due to weaker services as manufacturing continued to expand at an unchanged modest pace.

- Japan’s composite PMI fell into contraction (49.8, 51.2 prior) entirely due to softer growth in services as manufacturing continued to contract at a similar pace.

- India’s composite PMI increased by 1.5 points to 61.2 due to faster growth in services and continued solid growth in manufacturing.

- The Eurozone’s composite PMI fell by 0.9 points into contraction at 49.5 entirely due to weaker services as manufacturing remains slightly in contraction. Germany joined France in contraction.

- The UK’s composite PMI improved a bit toward a slightly slower pace of contraction as services shifted from mild contraction to slight growth.

- The US measures are due out this morning (9:45amET).

CANADIAN BANK EARNINGS SEASON

Troubled TD Bank led the start of the season this morning with a solid beat. EPS was C$1.97 (consensus $1.78). BNS is next on Tuesday, then BMO and National on Wednesday, and RBC and CIBC next Thursday.

G7 PRE-MEETING AND BOC TALK

BoC Governor Macklem and Canadian FinMin Champagne host a press conference at 2:30pmET. The purpose is to wrap up the meeting of G7 FinMins and central bank heads in Banff, Alberta ahead of next month’s meeting of G7 heads of state that I’m sure Trump will crash despite—or because—Canada holds the Presidency. It’s not clear whether they will broach policy matters of direct relevance to Canada or stay at a higher level with a summary communique of general things that were discussed during closed sessions today and tomorrow. We might also hear comments from the sidelines by other G7 central bankers and Finance/Treasury officials. Or it might just be about the gorgeous view in one of my favourite regions of Canada.

BoC DepGov Gravelle will be on a six-person panel at a NY Fed conference on monetary policy implementation and unwinding large central bank balance sheets (3pmET). His session is titled “Monetary Policy Implementation Around the World: More Similarities than Differences?” There will be no published remarks or webcast or press conference. Six people in 90 minutes gives each person 15 minutes of fame on the panel. Or not. I hate panels personally, especially massive ones like this one when there is almost no chance of getting into anything substantive.

There will also some other light data out of the US including existing home sales (10amET) after initial jobless claims held steady at 227k.

WHAT PROMPTED YESTERDAY’S MARKET MOVES

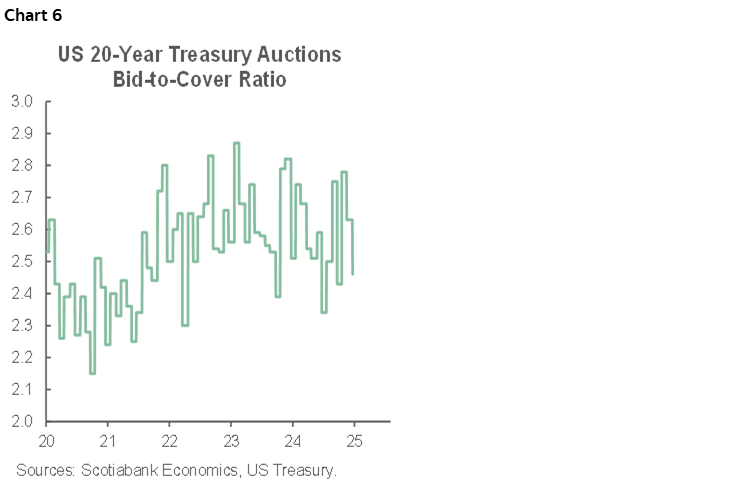

Yesterday’s session brought back memories of the debate a few weeks ago over lost US exceptionalism as the dollar sank and Treasury yields climbed sharply at the longer end. Textbook economics says that’s not usually something that’s supposed to happen. Some of this action occurred earlier in the session, but most of the bond sell off was triggered by the 1pmET 20y auction that markets begrudgingly took down at a weaker bid-to-cover ratio of 2.46 (2.63 prior) which is toward the lower end of the multi-year norm (chart 6).

Today brings a 10-year TIPS auction at 1pmET.

Why such a reaction to the auction? The bun fight over how big to raise the US deficit and the new addition of potentially hundreds of billions of funding for the “Golden Dome” initiative were among the reasons.

That markets are concerned about US fiscal largesse and the pressure to ram it through is also highlighted by the knock-on effects on money markets. BoC cut pricing is now down to a little over a quarter point for the full year. Fed cut pricing is at about a half point even. The latter remains too rich imo.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.