ON DECK FOR WEDNESDAY, MAY 21

KEY POINTS:

- Risk-off sentiment on global inflation worries

- UK core inflation surprises higher one day after Canada’s likewise experience

- Bank Indonesia cuts, rupiah holds steady on intervention threat

- SARB hold may be more likely after mixed CPI

- US budget reconciliation talks still in scramble mode

- Canada’s contribution to the ‘Golden Dome’ could cost hundreds of billions

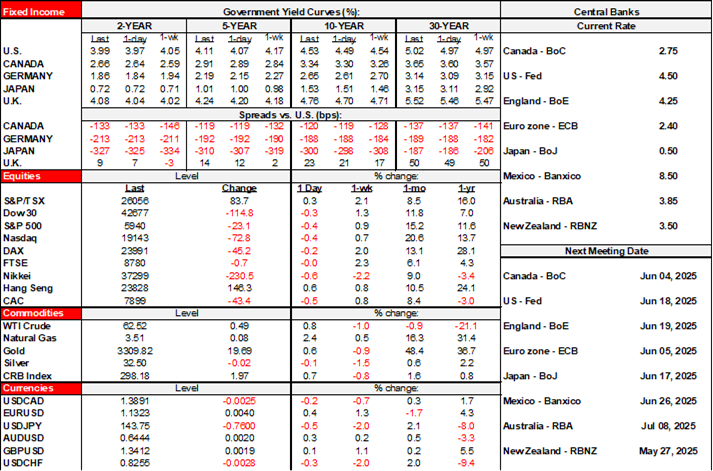

It’s a light session with nothing of direct consequence for this side of the pond. Strong UK inflation is the main event over in Europe. Oil prices are about 1% higher after reports that US intelligence believes Israel may be preparing to attack nuclear facilities in Iran. The combined effects have gilts underperforming other global benchmarks with yields up by 4–7bps across the curve, but sovereign yields are a little higher everywhere. Stocks are lower and led by a ½% drop in US futures while TSX futures and European cash markets are down by a little less. The dollar is in retreat against most major crosses. They’re still spinning their wheels in Washington over exactly how much further damage to do to US government finances. BoC cut pricing is holding around post-CPI levels (recap here) with about 8bps of a cut priced for June 4th, 15 for July 30th and about 35bps for the full year.

BOE CUT PRICING TRIMMED POST-CPI

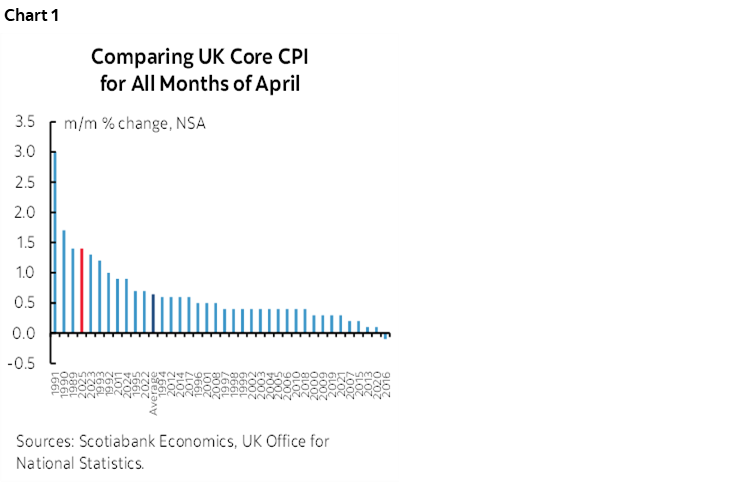

To see UK core inflation any higher than it was last month on a m/m NSA basis you have to go back to the early 1990s. Core was up by 1.4% on this basis and when compared to like months of April given the lack of seasonal adjustment it was tied with April 1989 and eclipsed only by April 1990 (chart 1). The y/y core rate jumped to 3.8% (3.4% prior, 3.6% consensus). Headline inflation was up 1.2% m/m (1.0% consensus) and heavily driven by Ofgem’s hike to the energy price cap.

Markets were already attuned to the BoE’s guidance that June was likely to be a hold, but shaved a few points off of August pricing that is now on the fence between a cut and a hold. Full year pricing was reduced to between 25–50bps of cuts this year.

BANK INDONESIA CUT

BI cut its policy reference rate by 25bps as widely expected, thereby averting the surprise risk they are famous for delivering. The rupiah held its ground partly because the move was largely expected, but also on guidance from Governor Warjiyo that BI “will not hesitate to stabilize the rupiah through market intervention.” Indonesia has a record high US$141 billion of foreign exchange reserves.

SARB LIKELY TO HOLD AFTER WARM CPI

South Africa’s CPI inflation rate was 0.3% m/m (0.2% consensus) and 2.8% y/y (2.7% prior and consensus). Core CPI, however, was up by just 0.1% (0.2% consensus) and 3.0% y/y (3.1% prior and consensus). The mixed results nevertheless continue to suggest that the South African Reserve Bank may keep its repo rate unchanged at 7.5% on Thursday next week.

US BUDGET TALKS

House Republicans are girding for a vote on a messy budget reconciliation bill as soon as tonight or tomorrow. They still can’t agree on the combination of tax cuts, spending cuts and SALT deductions but are seeking to do so before heading off for the Memorial Day weekend. If it passes in the House , then it’s unlikely to pass in the Senate absent big modifications.

‘GOLDEN DOME’ COST ESTIMATES—AND CANADA’S SHARE

A new wrench has been thrown into the works by ‘Golden Dome’ promises from Trump for a missile defence shield. He claims it will cost US$175B and be completed in three years and hence by the end of his term. Fat chance.

The CBO’s estimates run from as low as US$161 billion to as high as $542 billion (here) and so Trump is picking the lowest number. We all know the history of Pentagon cost overruns and delays, so it’s probably prudent to pad those figures as well. And the CBO says it would take two decades to operationalize—not three years; here too, Trump is lowballing the estimates. Efficacy may be another matter altogether and who knows how that turns out. Regardless, it’s an added entry in an already fiscally irresponsible set of measures.

As Canada apparently declares interest in joining the ‘Golden Dome’ project—confirmed by a spokesperson for PM Carney yesterday—Canadian taxpayers should be fully aware of these points on cost, timing and efficacy. Cost is a key consideration from a fiscal policy standpoint. Trump merely said yesterday that Canada will “pay their fair share.” Whatever that means.

If the costs of a system fully covering Canada and the US are proportional to area—which they may or may not be—then Canada’s inclusion would more than double the US$161–542B cost estimates from the CBO given that Canada covers a bigger area than the US. That could mean a total price tag of, say, US$350B to over US$1.1 trillion. There could be economies of scale to using the infrastructure that mean a lower total cost. Maybe the costs could be lower yet if the system were to only cover the major population centers in the southern half or quarter of Canada. What Canada’s share of the cost could be is unclear but needs to be disclosed and debated perhaps with PBO costing efforts along with the expression of interest it has apparently made. Would Canada’s share be calculated by its share of the land mass to be covered by the system? In that case, the bill could be around half of the estimated range or a little higher. If it’s done on a share of GDP or population basis, then the tally would be much lower. If it’s a blackmail payment to encourage the US to drop tariffs in exchange for buying more defence goodies from the US, then maybe it could be worth it given the longer-run damage tariffs would do. Until the next blackmail.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.