ON DECK FOR FRIDAY, MAY 2

KEY POINTS:

- Risk-on sentiment may be tested by nonfarm payrolls

- Markets are selectively interpreting headlines out of China…

- …that set a high hurdle for engaging the US in trade negotiations

- Japan douses optimism on US trade talks

- Nonfarm payrolls preview

- Canadian PM Carney to map out priorities

- Why Canadian auto sales are not reflecting tariff front-running like the US

Risk-on sentiment so far this morning will be tested by the state of the US job market when we get nonfarm payrolls. So far, sentiment is being buoyed by a selective interpretation of trade headlines out of China that hit last evening shortly after 8pmET and reversed US equity futures that had been falling after disappointing results and guidance from Apple and Amazon. European equities are outperforming in part because they are also catching up to yesterday’s US rally when much of the world was off for May Day. EGBs are outperforming US Ts partly in response to the tally for Eurozone CPI that came in a tick hotter than a stale consensus that was better informed by the country-level data over the past couple of days. Also watch PM Carney’s press conference this morning.

CHINA’S HUGE CONDITION FOR TRADE TALKS

It’s important to read the full statement (possibly with online translation help) from China’s Commerce Ministry that was in response to a reporter’s question and not just the snippets in the press. It noted that the US has reached out on trade talks and the “China is currently evaluating this,” while stipulating that in order to have trade talks, the US “should show its sincerity and be prepared to correct its wrong practices and cancel the unilateral tariffs,” and that “if the United States does not correct its wrong unilateral tariff measures, it means that the United States has no sincerity at all and will further damage mutual trust between the two sides. Saying one thing and doing another, or even trying to coerce and blackmail under the guise of talks, will not work with China.”

And so, the question we need to ask is how likely it is that Trump removes all tariffs before China agrees to talks? Not very in my opinion. It’s impossible to tell what is actually going on behind the scenes on both sides given all the face-saving activity, but I’m inclined to treat this skeptically.

JAPAN DOUSES OPTIMISM ON US TRADE TALKS

A series of headlines out of Japan this morning are applying a dose of reality to US propaganda on the state of trade talks with the nation. Prime Minister Ishiba said US auto tariffs are “absolutely unacceptable” and that the country won’t rush into decisions, Kyodo newspaper quote anonymous Japanese government officials who stated the US is unwilling to grant Japan exemptions on auto and steel tariffs and the 10% reciprocal tariffs that apply against everything. FinMin Kato said earlier this morning that “It does exist as a card” in reference to weaponizing Japan’s holdings of US Treasuries.

All of this indicates that there is no real progress on trade talks with Japan despite the US administration’s efforts to make it sound like a deal with Japan could come before others and perhaps soon.

As for weaponizing Treasury holdings, be careful, and I don’t view it as credible. Why not credible? If Japan were to sell US Ts, where would the money go? Back into JGBs and drive yen appreciation? Good one, that's just what Japan's exporters need on top of tariffs! And nowhere else offers the depth and liquidity of US Ts. Plus, it would be cutting off Japan's nose to spite its face given the impact on its own holdings. Further, that impact may be mitigated or countered by other forces and buyers after initial effects, like domestic buyers, other foreign buyers, perhaps a response from the Federal Reserve, and perhaps by finally adjusting the SLR to exempt Treasury securities.

NONFARM PAYROLLS

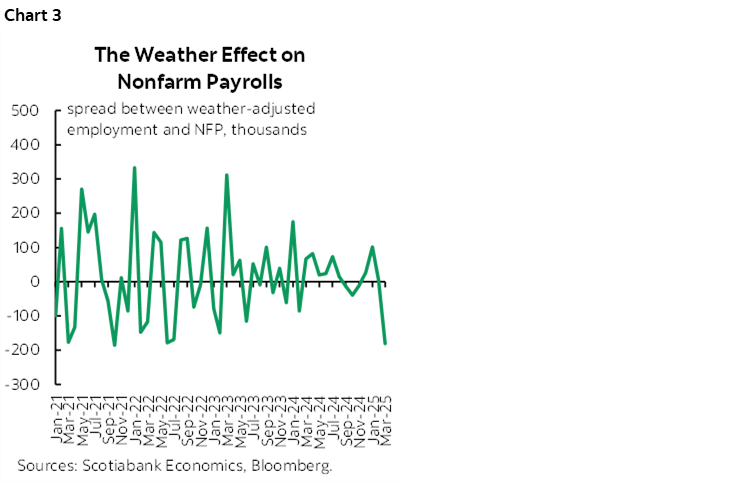

Nonfarm payrolls and related labour market readings for April will be updated at 8:30amET. Here are nonfarm expectations:

Consensus median: 137

Consensus mean: 132 (minor skewness)

Range: +50 to +171

Scotia: 165 (I’m ranked 2nd out of 72)

Whisper: 120

Std. Dev: 27

90% confidence interval: +/-136k

UR: 4.2% consensus and Scotia

Wages: 0.3% m/m consensus and Scotia

Drivers:

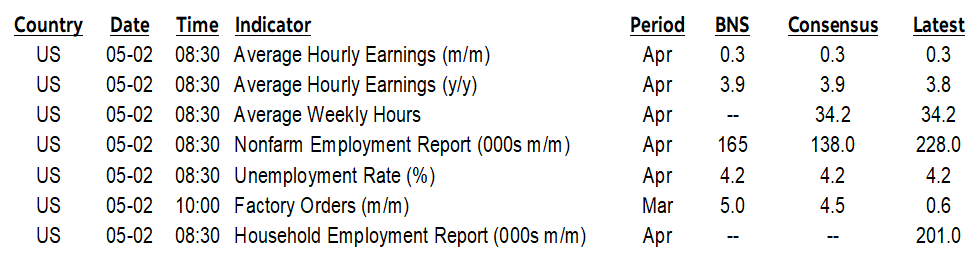

- Recent months of April tend to have among the highest SA factors for like months of April on record which reflects a recency bias in how they are calculated. This may overstate actual job growth if not for this recency bias in SA factors (chart 1).

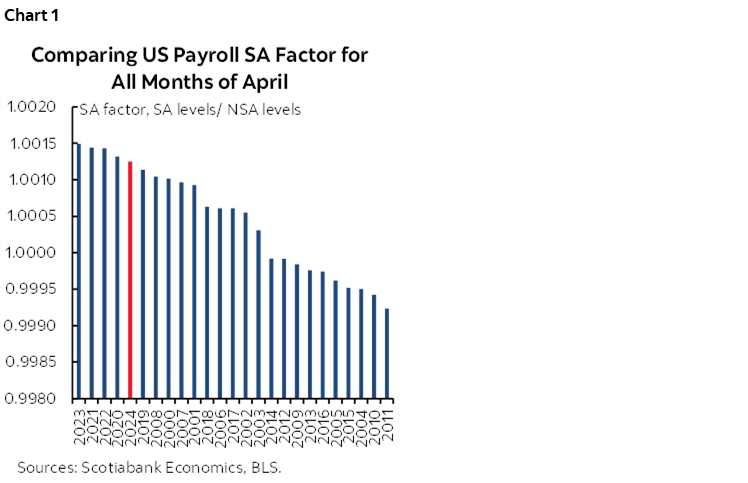

- April is normally a strong seasonal up-month for jobs (chart 2). Combine that with a likely overstated SA factor and it could be supportive.

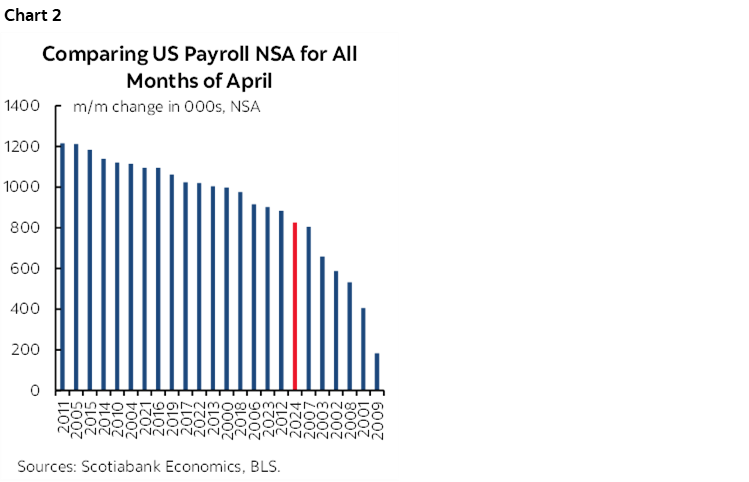

- Weather shouldn’t be a factor this time, but this is on the heels of the San Fran Fed’s weather-adjusted payrolls that indicate March payrolls were overstated by weather effects as opposed to understated in February (chart 3).

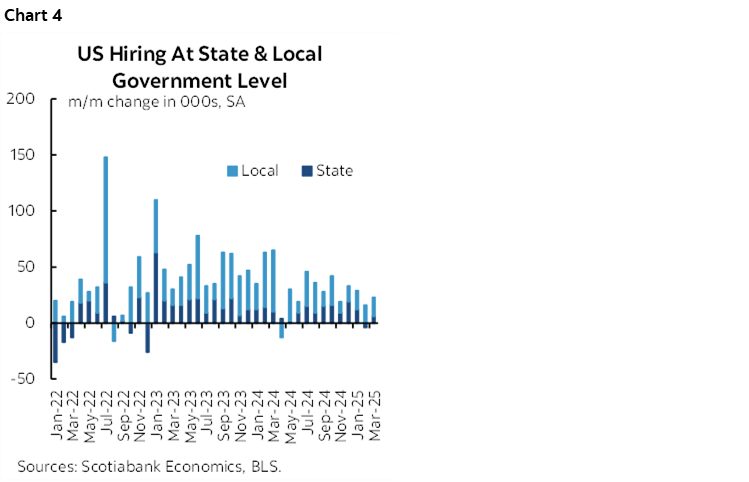

- a key uncertainty remains when DOGE firings of government workers will impact jobs. I think state and local hiring will continue to offset this month (chart 4).

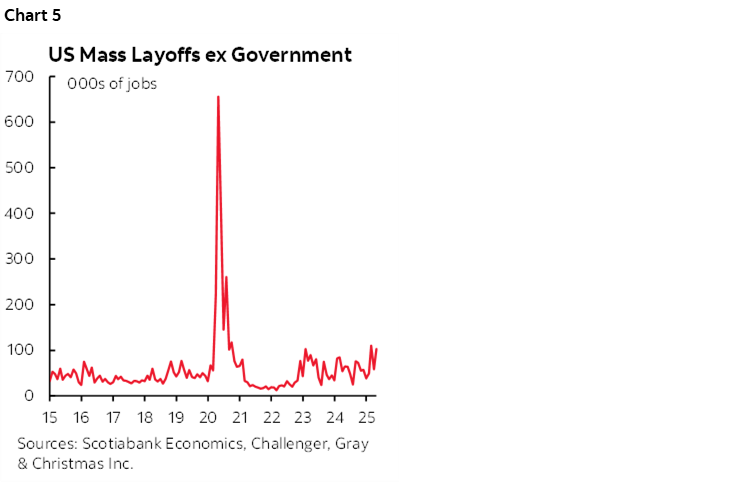

- Another key uncertainty is whether the pick-up in private sector layoffs shows up given April’s rise (chart 5). I expect this to be a modest effect in the reference period.

- Striking workers were not material in April.

- on tariffs, it’s likely too early to see much of an effect to the lagging consequences. They could perversely buoy hiring in the short-term through tariff front-running and hesitation to invest which tilts the capital-labour ratio toward labour. Uncertainty could also have driven more people to accept more part-time jobs.

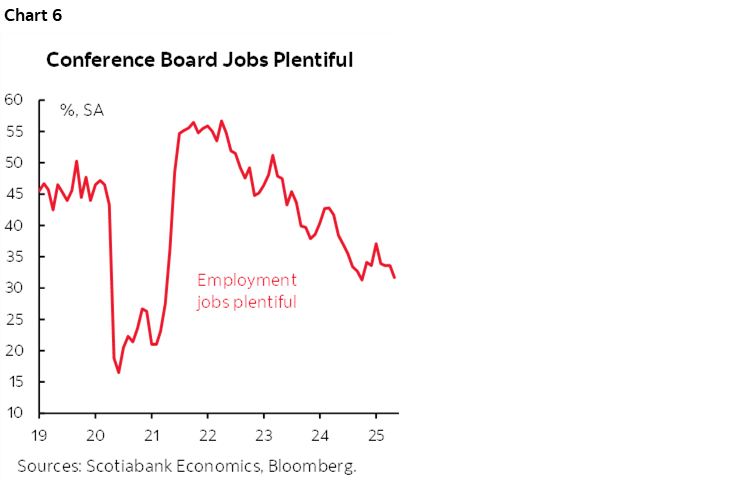

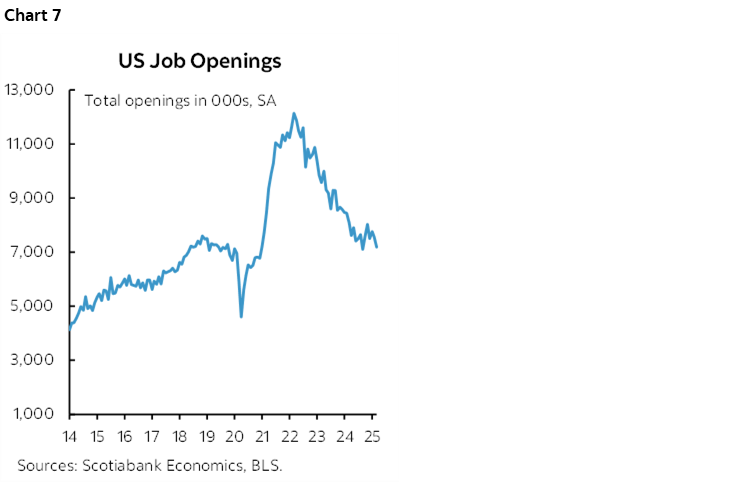

On leading indicators, they’re mixed and it would be irresponsible to read too much into them. Nonfarm is its own beast with its own methodology and quirks, such as counting multiple job holders instead of bodies, its own seasonal factors, the birth-death model effects, etc. None of these advance indicators tend to do very well at predicting m/m changes in payrolls.

- Consumer confidence jobs plentiful weakened (chart 6)

- NFIB hiring attitudes among small businesses arrives next week for April.

- ISM-manufacturing-employment suggests a reduced rate of contraction in manufacturing jobs.

- ISM-services-employment doesn’t arrive until next week.

- initial jobless claims were little changed between March and April nonfarm reference periods

- JOLTS job openings fell with downward revisions (chart 7).

- ADP slipped to 62k but tends to offer very poor tracking of private nonfarm payrolls

While nonfarm matters to the immediate market reaction, it's only one step along in the FOMC's quest to ascertain the impact of trade wars on the dual mandate that could be at odds with itself. Thus, one or two reports will settle nothing for Chair Powell.

CARNEY TO SPEAK TO GOVERNMENT’S PRIORITIES

PM Carney will host a press conference at 11amET in which he “will outline the new government’s priorities” and take questions. Watch for possible guidance on goals and red lines around trade policy into his meeting at some point next week with Trump. Also watch for initial outlines of what he seeks to advance in a first Budget that prioritizes elements of the platform. Anything goes on the regs front as well. It may or may not be instructive, but the event is billed as something that would inform steps along the way toward a Speech from the Throne when Parliament reconvenes.

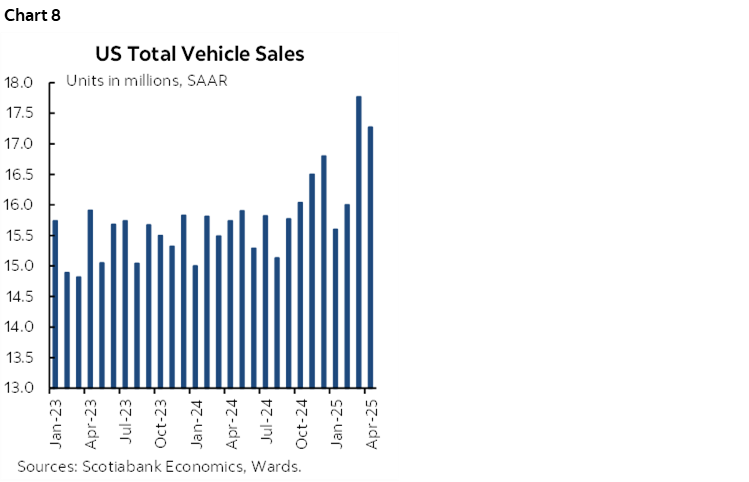

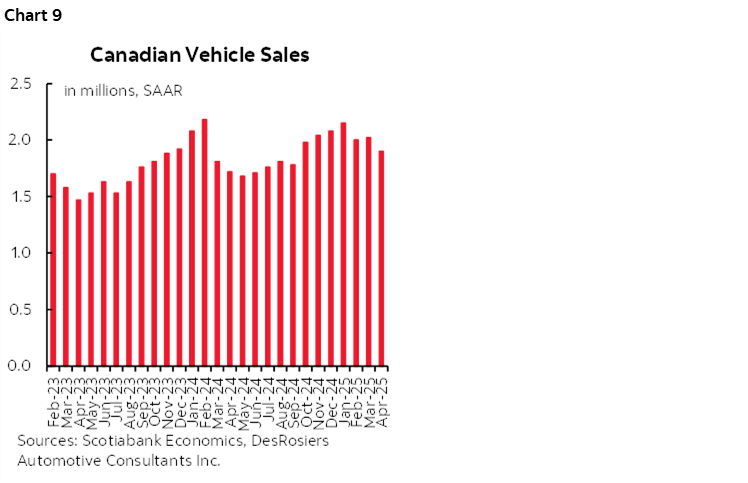

CONTINUED TARIFF FRONT-RUNNING IN US VEHICLE SALES, NOT IN CANADA

We got vehicle sales figures from the US and Canada late yesterday. The US figures were buoyant once more at 17.27 million SAAR in April after 17.77 in March for the two hottest back to back months since early 2021 (chart 8). The April figures either suggest that industry guidance was way too high and based on the first 17 selling days, and/or that sales really trailed off over the remained of April.

In Canada, however, auto sales have not demonstrated any front-running (chart 9). They fell by over 5% m/m SA in April after sales in March were up only by about ½% m/m following a sharp drop in February which broke a four-month upward trend over October through January. One possible reason for no front-running in Canada versus front-running in the US is that the US imposed high tariffs on everyone whereas Canada’s trade in autos with Europe and Asia was unaffected and so there was no need for front-running. Another possible reason is that Canada has more at stake in trade frictions which may be hitting demand harder.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.