ON DECK FOR TUESDAY, MAY 13

KEY POINTS:

- Mild risk-off sentiment into US CPI

- Markets may care more about this US CPI print than the FOMC will

- US CPI preview

- The US administration’s European education

- The UK job market continues to weaken

- Carney to announce his leaner—not lean—cabinet this morning

- Other light stuff: German ZEW, Indian CPI

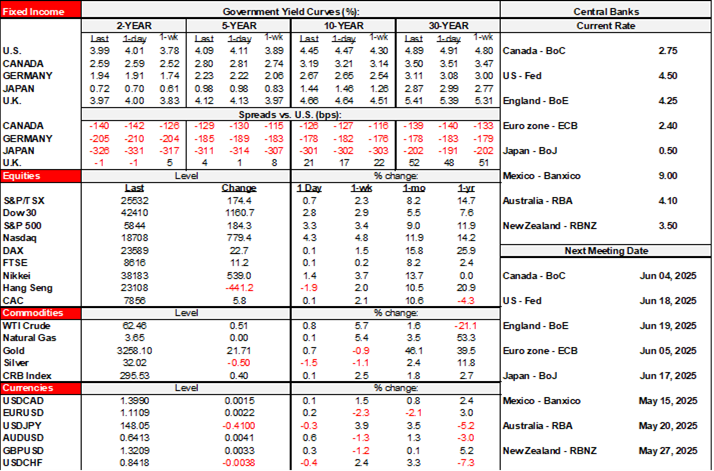

We’ll see if it sticks after US CPI, but for now, a mild risk-off tone is unfolding on this side of the pond. US and Canadian equity futures are gently lower versus mostly small gains in European cash markets. US Ts are outperforming EGBs by a few basis points across the curve with only the UK front-end giving the US a run for the money. The dollar is mildly softer. Developments to consider including weak UK job market readings, little news on the trade front, expectations into US CPI, and PM Carney’s new cabinet.

THE US ADMINISTRATION IS BEING EDUCATED ON EUROPEAN DYSFUNCTION

There are no major developments on trade to flag. US Treasury Secretary Bessent’s comments on Europe’s “collective action problem,” as he put it, coupled with Trump’s “nastier than China” reference to the EU finally reflects recognition of what we’ve all known for years about the EU but that this US administration fundamentally misjudged. The EU is a disparate array of voices from a highly heterogeneous collection of member states, with many differences across their economies, cultures, and politics. When Bessent flags differences between the Italian versus French stances on trade negotiations that are in the way of a quick agreement, it’s a sign that it is finally dawning upon the US administration that it will take a long while to negotiate with Europe. The US administration naively judged the EU.

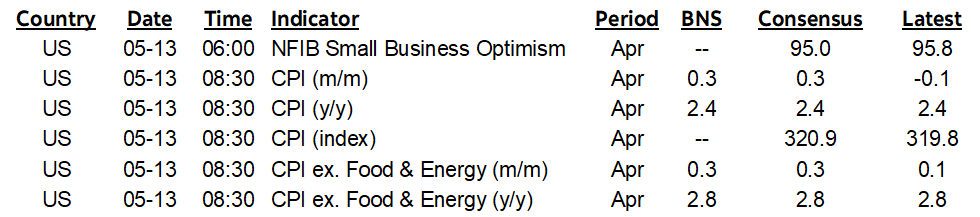

US CPI PREVIEW

US CPI for April might be the last of the relatively stale CPI prints (8:30amET). It’s likely to mean little for the patient FOMC that wants reams of dual mandate data before determining whether the policy shocks—namely tariffs—pose more risk to price stability or full employment and hence what the suitable policy response should be.

Nevertheless, we might get some early signs of tariff effects mixed in with other influences. Scotia’s estimate this time is in line with consensus estimates for 0.3% m/m SA increases in both headline and core CPI.

Adjusting for weighting differences in CPI and PCE and then factoring in relevant PPI components on Thursday will give us a good idea of what to expect for core PCE due out on May 30th.

Among the drivers are the following:

- SA factors: They are likely to extend the multi-year recency bias toward higher than usual estimates such as the all-time record high for April SA factors set last April (chart 1). This may overstate underlying inflation.

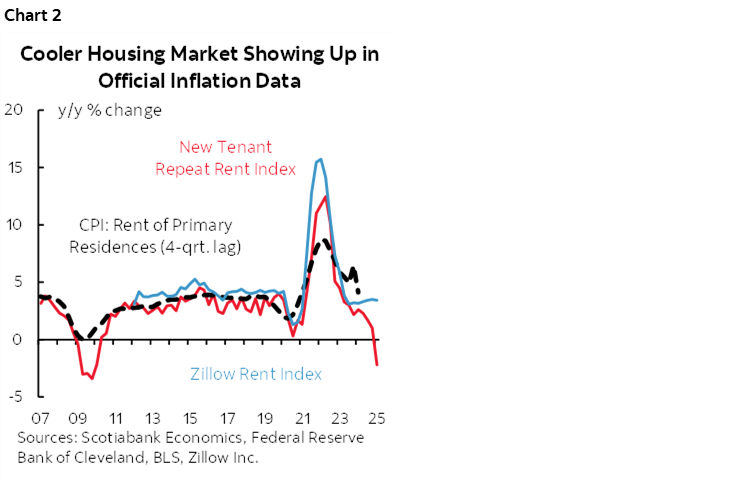

- Shelter costs—namely primary rent and OER—may add a combined 0.1% m/m SA to CPI on a weighted contributions basis and very slightly more to core CPI. Waning market rents should show up more significantly in CPI later on (chart 2).

- Vehicle prices are likely to be a minimal net effect this time, based on industry guidance. A mild rise in new vehicle prices is expected to be offset by a mild dip in used vehicle prices, but both are likely to begin heating up with tariffs and substitution effects going forward.

- Watch core services CPI (ex-housing and energy services). They were abnormally soft the prior month and possibly poised for a rebound.

- Core goods prices (ie: commodities ex-food and energy) could be the area where tariff effects show up including among the components. They were abnormally soft in March.

- tariff effects are extremely difficult to judge because it’s not just the weighted tariff rates we need to consider. Pass through effects could be delayed by selling down inventories at older prices, could be temporarily absorbed by high profit margins, and it takes weeks to months for supply chains to begin resetting prices and sparking widespread product shortages. More of the effects are likely to begin to show up in the next and subsequent reports.

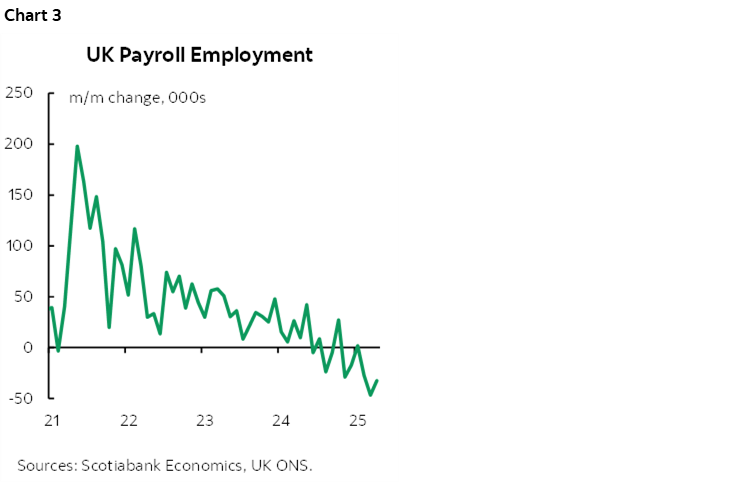

THE UK JOB MARKET CONTINUES TO WEAKEN

UK markets paid little heed to job market readings this morning. Gilts are outperforming EGBs but took a while to do so after the release of the figures, while sterling barely batted an eye at them.

- Payroll employment fell by another 32.5k in April (chart 3). 106.4k payroll position have been lost in the past three months. 148k positions have been lost since losses first began to appear in May 2024.

- Total employment lags with figures available to March, but 21k jobs were lost back then for the first drop since February 2024. Off-payroll small businesses are holding up the job market, but the loss of many higher paying payroll spots is disconcerting.

- The unemployment rate edged up a tick to 4.5%. It’s up from the cycle low of 3.6% set back in 2022.

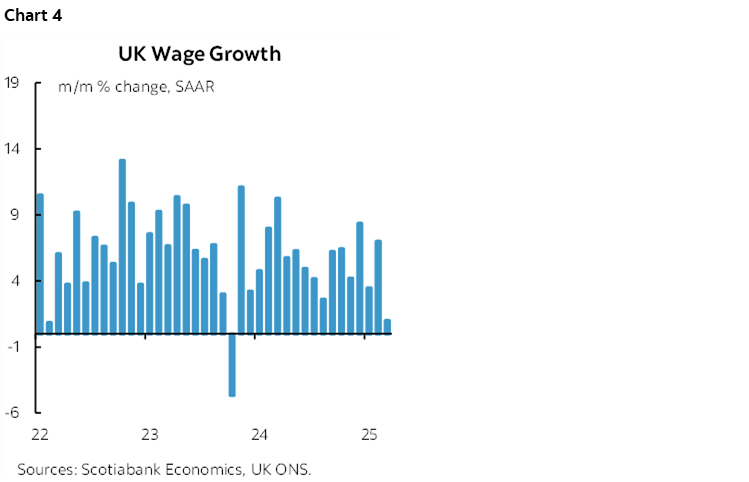

- wage growth slowed to 1% m/m SAAR in March for the weakest rate since October 2023 (chart 4). The three-month moving average slowed to 3.8% m/m SAAR.

- job vacancies fell to 761k from 783k for the lowest since April 2021, but they are still higher than the long-run average.

OTHER LIGHT DATA

German ZEW investor confidence is notoriously volatile, and so the 39 point turnaround in May’s expectations component that reverses the prior month’s drop to the lowest reading since 2023 is nothing particularly eye-catching.

India’s CPI inflation rate slipped to 3.16% y/y (3.3% prior) which is about what consensus expected.

CARNEY’S CABINET ANNOUNCEMENT

We’ll also find out who Canada’s next FinMin will be when PM Carney announces his slimmer—but not slim—cabinet. The swearing in ceremony is scheduled for around 10:30amET. Unconfirmed reports in the press indicate the cabinet will include around 30 ministers. That’s smaller than many of Trudeau’s cabinets, but not small, and a bigger one than Carney’s interim cabinet. Same, but different, as many carryovers from the prior administration will mix in with some new faces. Who will be Finance Minister is closely guarded despite leaks about multiple other posts (Hodgson in Resources, Fraser in Justice, Freeland and Guilbeault both in but unclear doing what etc). Then again, PM Carney is likely to have a very heavy say in Finance anyway and perhaps even more so than former PM Trudeau. Despite all the billing, that’s not terribly leaner than Trudeau’s last one at 39; see chart 5 for the history of cabinet sizes. Ottawa is a bloated government town, captured by excessive numbers of civil servants after ten explosive years in terms of their numbers. I wouldn’t seriously expect a vastly leaner cabinet today and history suggests that more time in office only grows their numbers.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.