ON DECK FOR MONDAY, MAY 12

KEY POINTS:

- The 90-Day Fiancé Deal is driving risk-appetite higher

- The US and China sharply reduce bilateral tariffs…

- …to still punishing levels with all other measures intact

- The path toward a true deal will keep markets on tenterhooks into mid-August

- Markets continue to slash Fed cut pricing

- Global Week Ahead reminder here

The ‘90-day fiancé’ deal is driving a solid risk-on session to start the week. US S&P equity futures are up by 3¼% with a percentage point more for the Nasdaq, while European cash markets are gaining by between ½% and 1½%. Mainland China’s stocks rallied by between ¾% and 1¾%. US Treasury yields are bear flattening with the 2-year yield up 10bps as Fed cut pricing is being scaled back to about 50bps this year including nothing in June, and the first full cut priced for September. Compare that to roughly 125bps of cuts that were being priced for this year a little over a month ago as markets went way overboard. The dollar is broadly stronger with only the CNH and CNY also firming. Oil is up by over 3% and gold is down by over $100.

The US and China agreed to step back from some of their tariffs on each other for a period of 90 days. The US will temporarily drop its tariffs to 30% from 145% and China will reduce its duties to 10% from 125% which is better, but still punishing with huge caveats.

For one, all tariffs prior to April 2nd when Trump’s trade wars escalated will remain in place, including sector-specific US tariffs on Chinese EVs, solar panels, semiconductors, steel and aluminum and select other goods. De minimis exemptions are still gone as of last week, slamming low-value trade. China’s other measures such as restrictions on critical minerals, and measures targeting individual US companies also remain in place.

For another, a 90-day suspension obviously leaves great uncertainty in place. Will Trump and Xi JinPing put rings on each other’s fingers and, if so, would the engagement last? This is not a deal, it’s just a de-escalation of tariff lunacy and we’ve seen temporary deals fall apart in the past. None of the core issues are being addressed.

Third, it’s unclear that 30% plus pre-existing tariffs doesn’t still grind US-China commerce to a halt. Worsened data, product shortages and inflation are still coming.

So, celebrate for now, but the volatile history of relations between these two countries combined with Trump’s extremely erratic ways will leave markets on tenterhooks into the mid-August timeframe by which point either some heroic attempt at a grand deal is miraculously pulled off in record time, or we’re back at it all again.

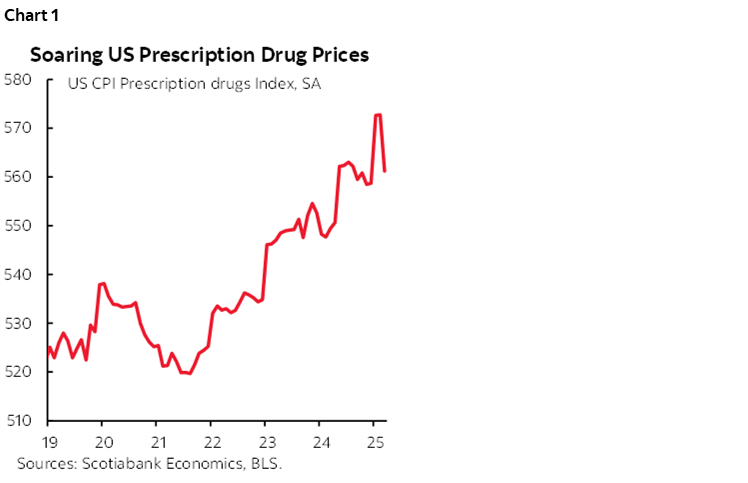

There is one sector not celebrating, however, as Big Pharma doesn’t like Trump’s plans to sign an executive order this morning to address soaring prices (chart 1). Trump claims he’ll cut pharmaceuticals prices by 30–80% by implementing a most-favoured nation policy to pay no more than people in countries that have the lowest price. No details at all, not least of which whether we’re talking government-run programs or broader reductions, which drugs, and how it would be executed. All hubris in my opinion. If successfully pulled off it would probably drastically impact access to drugs in the US and future innovation.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.