ON DECK FOR MONDAY, JUNE 9

KEY POINTS:

- Markets shake off the nonfarm high

- Canada’s curve is mildly underperforming US Ts on strong jobs, defence spending

- The explosive math behind Canada’s defence spending surge

- Canada needs a budget now to explain how to fund defence spending plans

- Chinese trade softens as tariffs kick in

- Chinese inflation remains weak

- Mexico to refresh CPI in an otherwise quiet N.A. session

- Global Week Ahead—It’ll Come in Waves (reminder here)

Markets are starting a fresh week with mixed performances across asset classes. Canada’s curve may be vulnerable to underperformance as the defence spending math sinks in (see below). Global equity benchmarks are flat to slightly lower across most of N.A. and Europe as Asia-Pacific markets rallied while catching up to Friday’s solid payrolls report especially considering a large estimated dent from weather. Sovereign bond yields are a few points lower across US and EGB curves with the UK front-end slightly underperforming. The dollar is broadly softer.

THE MATH BEHIND CANADA’S DEFENCE SPENDING SURGE

Canada is set to announce a major increase in defence spending today and key will be how it is funded and the likely amount of debt issuance. PM Carney will make the formal announcement at 10amET, then tour a military facility at noon, and then hold a press conference at 1pmET. The Globe and Mail is reporting that Canada will rapidly expedite its plan to increase defence spending by hitting 2% this fiscal year instead of 5+ years from now and then target further subsequent increases. This is ahead of a NATO summit on June 24–25th when Secretary-General Mark Rutte has said he expects members to raise military spending to 3½% of GDP plus 1½% on related security measures for a total of 5%.

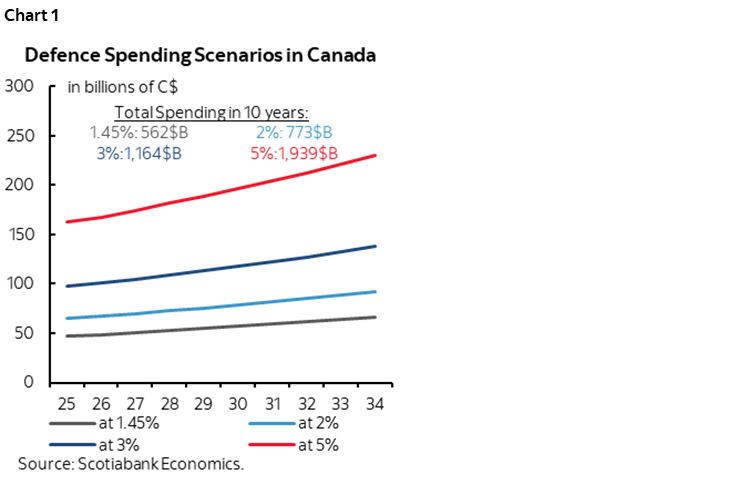

Chart 1 shows projections for annual spending in nominal dollars under various targets for defence spending as a share of projected nominal GDP. They update what was here.

Canada spent 1.45% of NGDP on defence last year, or about C$45 billion las year. 2% this year would mean raising that to about $65B for an increase of $20. Over ten years, a 2% of NGDP target that includes economic growth using our current forecasts for 2025–26 and then trend growth thereafter would amount to spending about C$775B, versus $560B at a steady 1.45% of NGDP for a cumulative ten-year rise of about $210B.

At 3% of NGDP, Canada would be spending about $1.16 trillion on defence and related security measures over a ten-year period for a cumulative $600B increase. At 5% of NGDP, Canada would be spending C$1.94 trillion for a cumulative $1.38T increase. Yes, ‘T’ as in trillions.

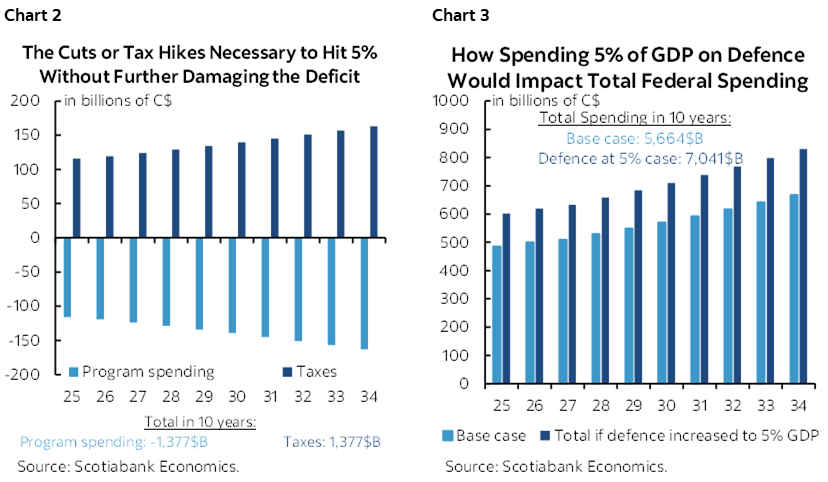

These amounts are obviously large and quite possibly very large for what is at present about a C$3.1T economy in terms of annual nominal GDP. A key question is how the defence spending surge will be funded. Will core program spending outside of defence be gutted? If the defence surge comes entirely from this source then chart 2 shows the annual reductions in program spending ex-defence that would be necessary to hit 5% of NGDP spent on the military. That’s unlikely, and unclear how it would be achieved given some parts that cannot be reduced (interest payments) or are very difficult to do, but Carney has said he will target operating spending increases at about 2% which is below the likely NGDP growth rates and would incrementally increase some room in the budget. Will taxes go sharply higher and, if so, then who pays? Chart 2 also shows the massive increase in tax revenues that would be needed if this is entirely relied upon. If higher taxes, then will it be a soak-the-corporations plan? Will the middle class and upper income households be soaked? All of the above? If so, then that could sterilize some of the economic impact but come at a cost to private sector growth. Will it all come from higher deficits and debt issuance? Chart 3 shows how much federal spending would increase over time if there were no other spending cuts and hence this amount would have to be funded by debt. That could compound risks to the bond market and term borrowing costs.

That’s why we need a budget! Now. Not in the fall which could stretch to days before Christmas. Now. You cannot go throwing around such massive spending targets with glamorous photo ops without a plan for how to fund it relative to everything else.

There are also implications for the Bank of Canada. An extra half percent of GDP spent on defence and related security measures is a material boost to nearer-term growth. How much so depends upon details behind the numbers that would inform how much of this boost leaks out through imports from foreign military equipment providers, versus how much is spent on domestic military equipment providers and how much is spent on transfers such as what appear to be plans to boost pay and benefits for the military. If Canada rapidly acts to increase spending beyond this fiscal year, then that—and the composition of spending—would have to figure into revised projections for the economy.

At this point, I would tentatively say that the spending surge is a modest additional argument for the BoC to stay on hold.

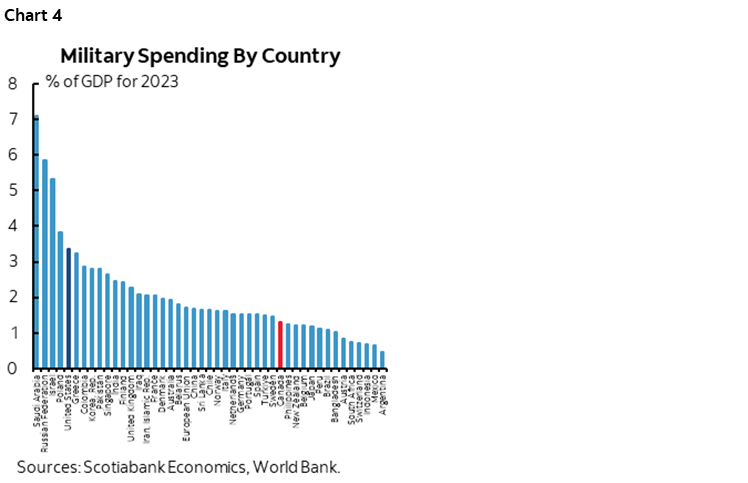

Then the politics enters the equation. Canada should be spending at 2% and thus meeting its NATO commitment. It has been an international laggard as shown in chart 4 that ranks military spending as a share of NGDP using World Bank comparable numbers from 2023; Canada would vault up the list at 2% and even more so at wherever it ultimately lands, but so would other NATO members. Yet Carney targeted 2% of NGDP on defence five years from now during the election campaign and so massively increasing this amount and the knock-on effects such as how to fund it are not what voters chose on April 28th.

Another issue is whether this is Canada’s ransom payment for getting out of US tariffs. If so, then the higher scenarios are one heck of a ransom payment for releasing the Canadian economy from the grips of Donald Trump’s protectionism and a massive departure from standing the country’s ground against US belligerence.

The question of value for money is also critically important. Canada faces no immediate threats to its borders. To what purpose would spending more on defence go toward? More peacekeeping missions? More active involvement in the world’s hot spots? Putting out forest fires raging across the country? Or sitting idly by and being another source of Canada’s productivity issues?

Perhaps the biggest question of all is whether all of this sudden love affair with military toys will make the world a safer place, or a more dangerous one. One argument is that it’s necessary because of Russian aggression, and to counter China’s build-up. A counter is that the world has rarely been a safer place when everyone is surrounded by the temptation to use their toys.

CHINA DEVELOPMENTS

The US and China restart trade negotiations in London today so keep an eye on any headline risk going forward.

China’s trade figures slowed a bit more than consensus expected for the month of May. In USD terms, export growth was 4.8% y/y (6% consensus, 8.1% prior) while import’s contracted by -3.4% y/y (-0.8% consensus, -0.2% prior). Some of that was a currency effect as yuan-denominated exports were up 6.3% y/y (9.3% prior) and imports fell -2.1% y/y (+0.8% prior).

China’s inflation stats offered little surprise. CPI was unchanged but still soft (-0.1% y/y, -0.2% consensus). Producer prices fell a little more rapidly (-3.3% y/y, -3.2% consensus, -2.7% prior) partly as oil prices fell.

QUIET N.A. CALENDAR

There is little on tap into the N.A. session. Mexican CPI for May is due out, but monthly tallies rarely offer material surprises since the figures are released on a bi-weekly basis (8amET). Consensus expects 0.2% m/m with core up 0.3%. The NY Fed’s 1-year inflation expectations measure is also due for the month of May (11amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.