ON DECK FOR THURSDAY, JUNE 5

KEY POINTS:

- Long-ends shake off a weak Japanese long bond auction

- Bowman’s confirmation clears the way for regulatory reforms like the SLR

- ECB to cut, but forecasts could be more important

- US job cuts to be refreshed; mind the seasonality

- Waiting for Russia’s retaliation that Trump ignores

- The BoC has a chance to clarify muddled communications today

- German factories surprise

- Swedish rates outperform on soft CPI

- Canada-US trade figures on tap

Global markets are on decent footings so far this morning alongside some key developments. Equities are slightly higher across N.A. futures and European cash markets. The dollar is broadly softer except against traditional safe havens like the yen and CHF. Bond yields are gently lower across most global benchmarks except for a slightly cheaper US front-end. There is no material follow-through on the Bank of Canada’s decisions after they did the right thing holding the policy rate unchanged (recap reminder here) but we’ll see if a BoC official clarifies contradictory communications today.

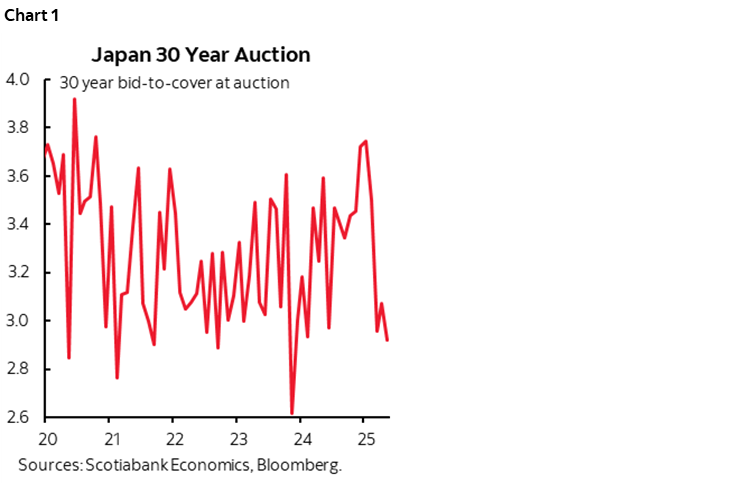

GLOBAL LONG BONDS SHAKE OFF A POOR JAPANESE AUCTION

Japan’s long-bond auction didn’t go so well but was quickly shaken off in favour of broader drivers. The bid-to-cover ratio of 2.91 (3.07 prior) wasn’t great (chart 1), and it settled at a yield of 2.9% that was higher than the yield going into the auction. And yet the long-end rallied into this morning with local participants fingering short-covering as the explanation. Or maybe its apprehension ahead of the ECB and US payrolls and confidence that US banks will be allowed to ramp up Treasury holdings (see below). Still, the yen is the weakest performer to the dollar this morning, but so is CHF on a general risk-on day that is weakening the dollar.

ECB TO CUT

Now it’s onto the ECB that is widely expected to cut. The statement arrives at 8:15amET and will be followed by President Lagarde’s press conference 30 minutes later. I’m sure we’ll get another rant from Trump about why the Fed isn’t cutting, notwithstanding the fact that the Eurozone isn’t the one that imposed absurdly high and protectionist tariffs that are roiling supply chains and sparking higher US inflation risk.

The ECB's updated forecast will be crucial in assessing the potential impact, especially given that this will be its first revision following the latest round of tariffs imposed by former U.S. President Donald Trump on Liberation Day. Given that the ECB is approaching a neutral setting, the bias may continue to be expressed in guarded, careful, data dependent fashion.

US JOB CUTS TO BE REFRESHED SHORTLY

On tap will be US Challenger job cuts shortly (7:30amET). They peaked at 275k in March for the highest reading since 2020 before falling back to 105.4k in April. The figures are not seasonally adjusted and so while they are higher than the start of recent years, there has been a seasonal pattern of coming in higher early in the year and then quickly ebbing. We could be on that same path again, especially since DOGE cuts to federal government employees have peaked.

WAITING FOR RUSSIA’S RETALIATION

Geopolitical risk is also lurking in the background, waiting to pounce forward at any moment after Putin told Trump (according to Trump…) that he would retaliate against Ukraine’s brilliant drone attacks. It’s uncanny that a Russian leader would tell a US President that he’ll attack an ally or quasi-ally and a US President basically shrugs. America First means standing by your allies and knowing who your foes are and I’m not sure anyone knows where the US stands on either count these days.

BOWMAN’S CONFIRMATION CLEARS THE DECKS FOR REGULATORY REFORMS

Michelle Bowman was confirmed by the Senate last evening as Vice Chair for Supervision at the Federal Reserve. This opens the door to now pursuing select regulatory reforms such as altering the Supplementary Leverage Ratio to enable banks to play a more active role in the Treasury market and simplifying capital requirements.

OVERNIGHT RELEASES

There were a few overnight releases that didn’t sway much.

German factory orders surprised higher with a 0.6% m/m rise in April (-1.5% consensus) following a prior gain of 3.4%. It’s possible that tariff front-running continued to exert influences. Autos were up 1.5% m/m, computers/electronics were up 5.4%, and metal production gained 1.5%.

Sweden’s front-end is outperforming after a soft CPI reading. CPI was flat at 0% m/m (0.2% consensus) and underlying inflation ex-energy was up 0.2% (0.3% consensus).

China’s private composite PMI fell 1.5 points into contraction at 49.6. That was entirely due to the already known 2.1 point drop in the manufacturing PMI to 48.3 as the services PMI increased 0.4 pts to 51.1.

TRADE FIGURES ON TAP

Canada updates trade figures for April this morning that will help to track implications for GDP growth (8:30amET). The US also refreshes trade figures, but we already know the goods component onto which a usually stable services balance is tacked. Other minor releases including US weekly initial claims (8:30amET) and Canada’s Ivey PMI (10amET).

BOC TO SPEAK ON COMMUNICATIONS TODAY

After the BoC did the right thing holding, one of its Deputy Governors will speak about communications. DepGov Kozicki’s address titled “Talking to Canadians: How Real-World Insights Shape Monetary Policy” will be available online at 12:20pmET with audience Q&A to follow but no press conference. I’m much less interested in the title than what I hope to be a question that reconciles the conflict in the BoC’s communications that I wrote about in my recap (here).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.