ON DECK FOR TUESDAY, JUNE 3

KEY POINTS:

- Risk-off sentiment driven by ongoing concerns about US policies

- OECD forecasts are merely catching up to tariffs

- Eurozone core CPI softens, ECB pricing holds steady

- Light US data: JOLTS, factory orders, vehicle sales

- More Fed-speak—and countless iterations of ‘patience’

- Canada waves the pom poms

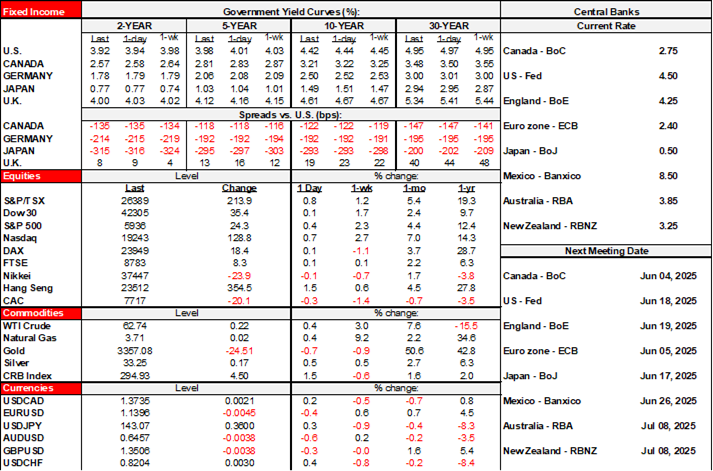

Risk off sentiment is driving equities lower, bond prices higher and the USD higher against all major crosses in a classic set of cross-asset moves. I don’t see any major new catalysts as opposed to dealing with the same volatility around Trump’s anachronistic policies that seek to impose great damage on the world economy.

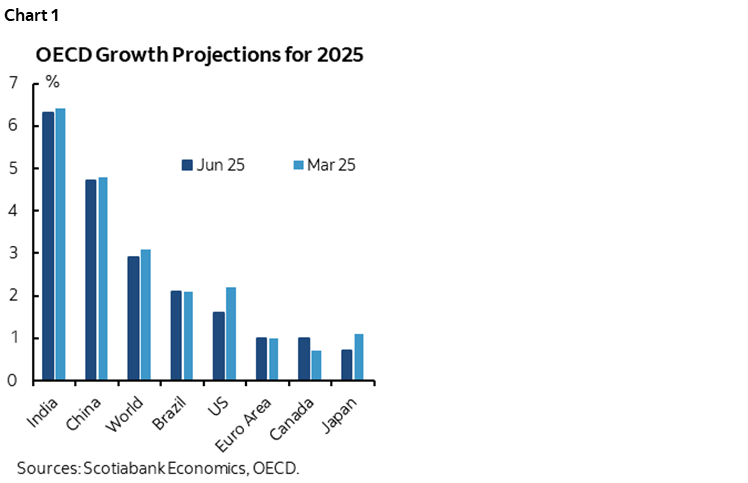

OECD DOWNGRADES STALE PROJECTIONS

OECD forecasts are making headlines, but only because they forecast so infrequently; the downgrades to global growth are relative to its interim projections in March before ‘Liberation Day’ and to the main projections every six months. Tariffs are here, and the OECD just got the memo. Chart 1 shows that the biggest downgrade was to the US.

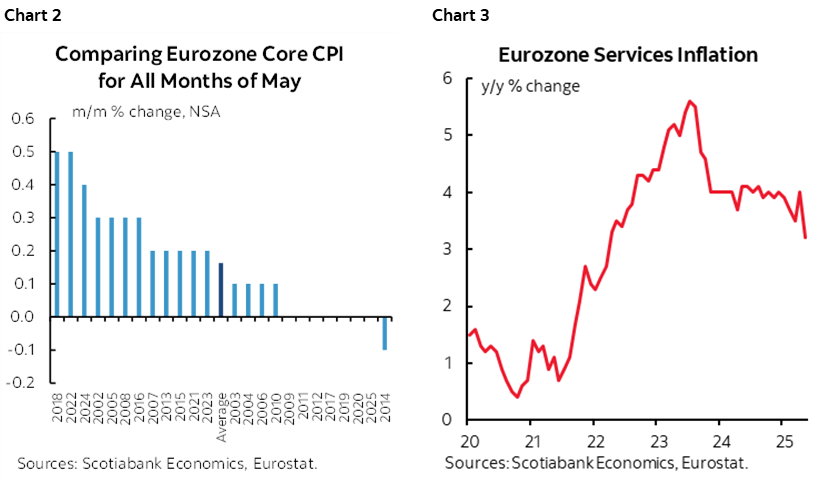

EUROZONE CORE CPI SOFTENS

Nor was it Eurozone CPI that mattered much. Eurozone CPI was about as expected because the thrill had come and gone after last week’s releases by major economies, but core offered a little new information. CPI was flat (0% m/m) and edged lower to 1.9% y/y (2.2% prior). Core CPI was up 2.3% y/y (2.7% prior) which was a touch lower than all but three out of thirty-five forecasters expected. Core in m/m seasonally unadjusted terms was on the softer side of history (chart 2). Services inflation also decelerated (chart 3). There was little impact upon ECB pricing and EGB yields that had slightly rallied before CPI at the open.

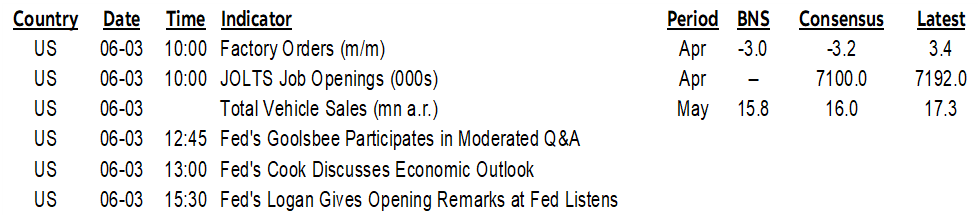

US DATA — WEAK FACTORY ORDERS, LOWER VEHICLE SALES, JOLTS WILDCARD

Light US data may concentrate risk around JOLTS job openings in April (10amET) but using them to forecast payrolls is futile. Factory orders are expected to be soft in the wake of the already known 6.3% m/m plunge in durable goods orders and probably modest resilience in nondurable goods orders (10amET). Vehicle sales in May are also due out at the end of the day and industry guidance points to the beginning of the other side of the pulled forward tariff frontrunning effect that drove them much higher from February through April.

FED-SPEAK — COUNTLESS ITERATIONS OF ‘PATIENCE’

There will be more Fed-speak before the FOMC communications blackout kicks in on Saturday ahead of the June 18th decision. It’s hard to imagine what they could say that would be new given the whole Committee subscribes to some variation of being ‘patient.’ Chicago’s Goolsbee (12:45pmET), Governor Cook (1pmET) and Dallas President Logan (3:30pmET) are all on tap.

QUIET IN CANADA

There is nothing on tap in Canada where the pom poms and cheerleading of shorter approval periods and the laying down of loose criteria for preferred infrastructure projects sounds encouraging in a sense but will take ages to deliver. That may be what Canada simply has to accept as opposed to the past tendencies to prop up short-term growth with endless supports that compound problems in the economy at the expense of tackling important long-run issues. Eighteen years after its discovery, maybe, just maybe we’ll see Ontario’s mineral-rich ‘Ring of Fire’ being developed—in the decades to come. That could be wonderful. So could development of a new pipeline—again, many years from now and dependent upon how all the special interest groups jockey to get a piece of the action.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.