ON DECK FOR FRIDAY, JUNE 27

KEY POINTS:

- Markets ending the week with a deluge of global data

- Eurozone inflation tracking is off to a rocky start

- Japanese inflation ebbed

- Canada’s economy is probably tracking softly in Q2

- Ho hum, another soft US core PCE report beckons…

- …with the usual counters about why it doesn’t matter

- BanRep expected to hold with cut risk

- Canada’s Bill C-5 passed. Now the work begins as higher deficits & taxes loom large

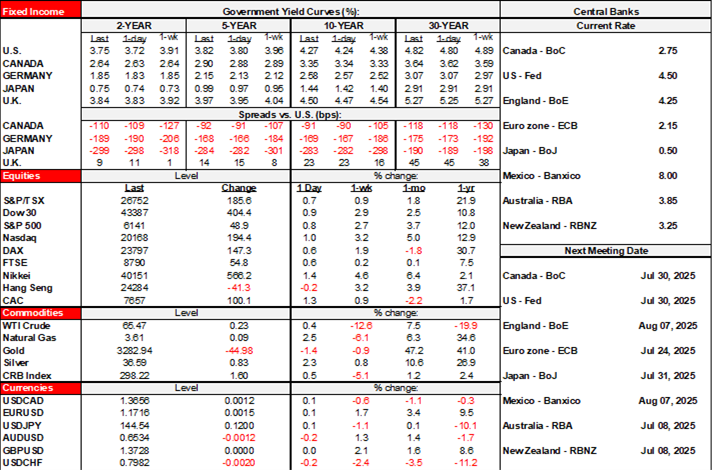

Sovereign bonds have a slight cheapening bias into the N.A. open, equities are largely bid by between ¼% on the S&P and significantly more for most European benchmarks but Toronto is flat. Currencies are mixed versus the dollar. Significant US and Canadian data follows on the heels of firmer than expected hints at Eurozone inflation while Japanese inflation went the other way. All of this is heading into a quieter holiday-driven calendar in N.A. next week as month-end, nonfarm payrolls, the ECB’s Sintra forum, the push to pass the ‘big, beautiful bill’ in the US senate and national holidays in Canada and the US.

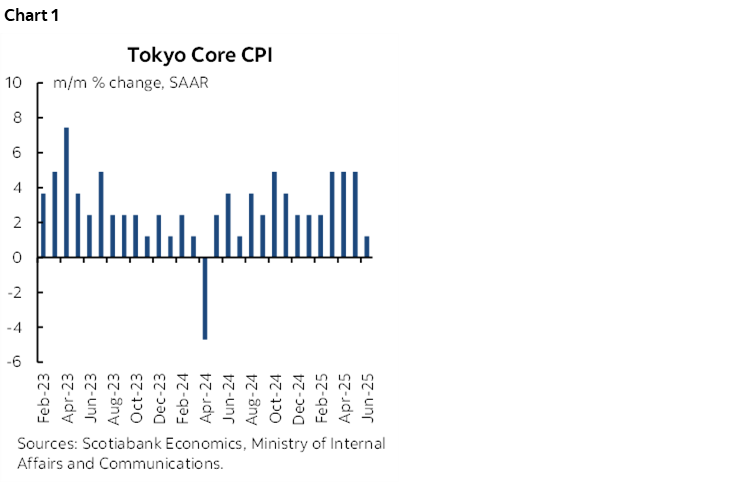

JAPANESE MARKETS IGNORED INFLATION

Japanese inflation ebbed more than expected in June. The Tokyo CPI measure was up by 3.1% y/y (3.4% prior, 3.3% consensus) and the measure excluding food and energy was up 3.1% y/y (3.3% prior and consensus). In month-ago, seasonally adjusted terms, core Tokyo CPI was the weakest since last summer (chart 1). The yen and JGBs shook it off.

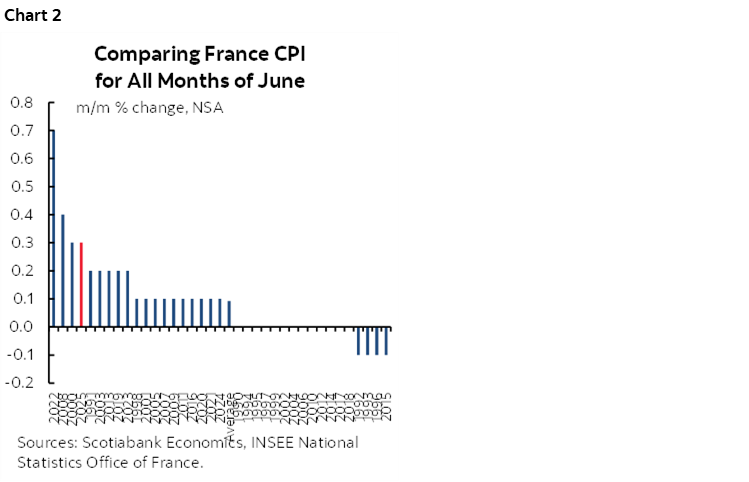

FRENCH INFLATION DRIVES CHEAPER EGBS

Eurozone inflation readings are off to a rocky start as France and Spain released ahead of next week’s readings from Germany and Italy and the Eurozone tally.

- France reported CPI up 0.4% m/m NSA, doubling consensus, but still leaving inflation at just 0.8% y/y (0.6% prior, 0.7% consensus). Given it’s seasonally unadjusted data, we need to compare this June to other months of June to see how much of a stand-out this was and that’s done in chart 2. When those figures landed they drove an immediate 2–3bps jump in the 2-year French yield that carried other EGBs with it.

- Spain recorded CPI up 0.6% m/m, matching consensus, and up 2.2% y/y from 2.0% prior but also matching consensus. Core CPI was unchanged at 2.2% as expected.

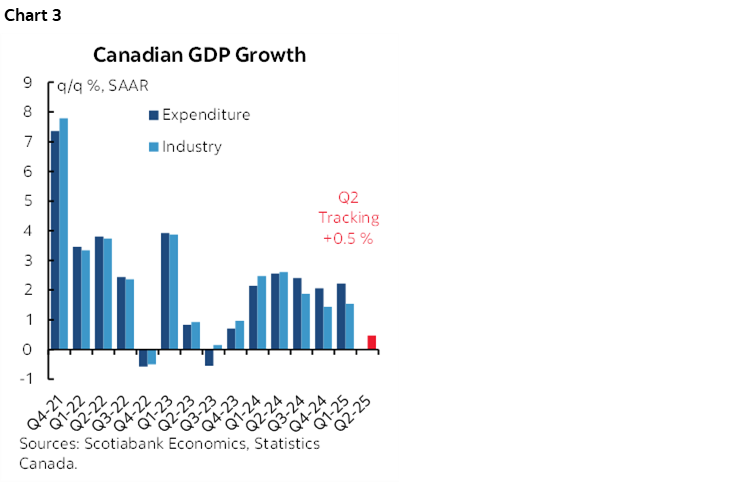

CANADA’S ECONOMY IS PROBABLY TRACKING SOFTLY IN Q2

Canada updates GDP figures for April and May this morning that will provide a better sense of how the economy is tracking in Q2 (8:30amET). April was previously guided by Statcan to be up by 0.1% m/m SA. I went with 0%. Since their initial estimate on May 30th, the data flow has been softer than guided which points to more downside than upside risk. There is more likelihood of a negative print than a higher reading. May’s weather this year may have also dampened seasonal categories.

May GDP is uncertain, but several advance readings point to another soft month. Hours worked were flat, the prior surge in housing starts levelled off and limited other readings like the retail sales flash were soft. How all of these readings translate into value-added GDP concepts is unclear, but a simple regression tends to work reasonably well and suggests softness in both months.

What’s missing from these readings are the ingredients for quarterly expenditure-based GDP like trade and inventory effects that are likely to reverse some of the prior quarter’s contributions. Chart 3 offers tracking before we get these readings.

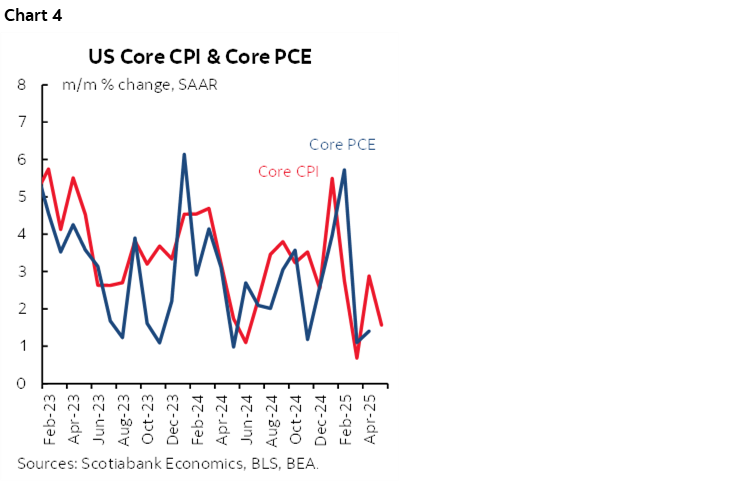

US CORE INFLATION—THE FUN LIES AHEAD, NOT TODAY

The US will release the monthly batch of readings on the state of the consumer and the Fed’s preferred inflation gauges for May (8:30amET).

Core PCE inflation is expected to be soft again. Consensus is overwhelmingly at 0.1% m/m SA with a few at 0.2% and a couple of us at 0.0%. Core CPI was up by only 0.1% m/m as one ingredient and offers at best a loose guide (chart 4), but then I think the combination of weighting differences on the categories compared to how they are captured in PCE plus the contribution from PPI components that get captured in PCE may combine to just barely drive core PCE to be flat.

I’m sure you’ll hear the usual cats saying there is no inflation in the US and no tariff effect. The same counters hold. It’s premature to judge tariff pass through as we need months and months of data stretching into Fall in order to assess early effects. The data quality is poor with 30% of the basket being guessed at and wonky SA factors. We’ve seen plenty of soft patches in the past and should know better by now than to overreact to them given the tendency to subsequently zoom higher.

US income growth is expected to outpace consumption growth again in May, but by a narrower margin this time. If that happens, then the saving rate may continue to edge higher and possibly hit 5% as precautionary saving rises. I went a little higher than consensus on consumption growth based on the gain in the retail sales control group.

THE REAL WORK BEGINS IN CANADA AFTER A PIECE OF PAPER PASSES

Bill C-5 has passed in Canada (here). It’s the bill to fast-track major projects that the government deems to be in the national interest to obtain quicker approvals. It’s a welcome effort to reduce bureaucracy that too often stops initiatives in their tracks, but it’s merely a first step. Now we need to know what those projects are, whether they are truly sensible or not, how they are funded, how deep opposition from interest groups will extend as a barrier to success, how broadly the benefits may apply outside of the directly impacted interests etc. Piece of cake. Much bigger deficits and bond issuance and higher taxes are likely to arise to pay for lofty public spending ambitions as the government remains committed to an extra >$1 trillion of spending on defence and very loosely related infrastructure over the next decade compared to the current run rate on defence spending. Asset sales are at best a drop in the bucket that do nothing to counter the risk of explosive structural deficits.

BANREP TO HOLD WITH CUT RISK

Colombia’s central bank is expected to hold its overnight rate at 9.25% with a minority including our economics in Colombia expecting a cut (2pmET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.