ON DECK FOR WEDNESDAY, JUNE 25

KEY POINTS:

- US markets await the Fed’s capital plans

- Fed Board to meet today on potential changes to the SLR/eSLR

- Key takeaways from Powell’s second round testimony ahead of round two

- The explosive math behind Canada’s defence and infrastructure spending spree…

- …and what it means to deficits, bond issuance, taxes and program spending…

- ...as Canada’s borrowing advantage to the US is vulnerable

- US to refresh new home sales

- Australian CPI fully prices RBA cut in July

- BoT held as expected

Markets are going into the Federal Reserve Board’s meeting on capital requirements with a cautious tone across asset classes. Equities are little changed across N.A. futures and European cash markets. Ditto for global sovereign bonds. The dollar is mixed. Oil is up by about 1%.

Round two of Chair Powell’s testimony will unfold this time before the Senate Committee on Banking, Housing, and Urban Affairs (10amET). It’s hard to imagine Powell saying much of anything different after his smack down of Waller’s and Bowman’s views yesterday.

As soon as he’s done by around 1pmET, Powell will be whisked across to the Board of Governors meeting on proposed revisions to the supplementary leverage ratio standards at 2pmET. It’s an open hearing available by webcast if you’d like to watch and dependent upon your interest in capital policies.

The Bank of Thailand held its policy rate at 1.75% as expected.

Australian CPI fell a little more than expected (2.3% y/y, 2.4% prior, 2.3% consensus). Trimmed mean ‘core’ inflation ebbed four-tenths to 2.4%. Australia’s shorter-term government bonds are outperforming other global benchmarks as July RBA 8th RBA cut pricing increased a few points to almost a full quarter-point.

The US will refresh new home sales in May at 10amET (consensus -6.7% m/m SA, Scotia -5.8%).

RECAP OF WHAT POWELL SAID YESTERDAY

From a market standpoint, Powell's testimony before the House Financial Services Committee didn't matter one bit yesterday. Instead, markets spent the time throughout his testimony reacting to the drop in oil prices on speculation that Iran and Israel have a durable ceasefire, and to the drop in consumer confidence and the components like softer inflation expectations one-year forward and a small softening of the 'jobs plentiful' gauge. That's why rates rallied, not really because of anything Powell said.

And yet, confidence is a poor measure of inflation expectations that remains high, and the 'jobs plentiful' subindex is not a good advance indicator for nonfarm payrolls (chart 1) while having residual seasonality issues that are evident in the obvious seasonal trends in recent years despite being adjusted for seasonality (chart 2). Further, actions speak louder than words, so confidence should be faded in favour of data for all those reasons imo.

Regardless, here’s what unfolded in Powell’s written testimony (here) and the banter after listening to the whole three hours of it:

- Powell stuck to what he said last week during the post-FOMC meeting press conference with no signs of a pivot on needing more data before deciding on what is the appropriate next step.

- Powell largely rejected the bait to comment on references to a possible cut in July by Governors Waller and Bowman, saying there is a variety of opinions on the Committee. The Chair's opinion remains skewed toward being patient.

- when directly invited to comment on July, he said he wouldn't want to attach a timeline to a potential policy shift and that significant data is required. What's missing is more important which is the continued absence of any reference to being open to a move "somewhat soon" or "soon" assuming he'll still wish to hold the market's hand in the midst of another potential policy pivot point.

- On tariff pass through, he emphasized June and July data that we'll only get in total by August before Jackson Hole for CPI and PPI, and after Jackson Hole for PCE. Later in his testimony he even added August data as a litmus test which might mean he’ll be patient for even longer. This is a strong indication that the Fed Chair will guide a Committee through several rounds of data before deciding on next steps.

- That suggests the first time to expect a pivot may not be until Jackson Hole or the September FOMC as long as data cooperates. I'm doubtful. I think higher prices will be pushing through those reports and subsequent ones, leaving the debate over price level versus inflation effects still undetermined which would continue to counsel patience. An environment of potentially spiking prices would not be one in which it is possible to determine whether it is a temporary effect.

- on the SLR/eSLR he basically said including/excluding Treasuries is something they've asked for comments on and deferred to today’s Board meeting on the topic after his Senate testimony.

- Powell was asked about the run-off of MBS as a contributor to wide spreads and housing market frailties and said he doesn't think it's a driver, and that there are cost pressures pushing up housing costs as well and that's influencing the housing market. He could've also noted the level impact of slashing Treasury run-off at the March FOMC.

- Interestingly, when asked if Trump can appoint himself as Fed Chair, Powell said he doesn’t know and it’s "not a question for me. I wouldn't speculate." In my view, markets would be the ones to answer that question in short order!

- Asked about price level versus inflation effects of tariffs, Powell said "you don't respond to a one-time shock, but this is different. We need to take some care. In 2018–19 not only did we not raise rates but we cut rates because the tariffs were much smaller than now and we hadn't back then had a surge in inflation going into it with the effects on expectations." I found that to be a more balanced view than, say, Waller's strong view that makes it sound obvious that it's a mere one-off price level adjustment. This is the crux of the debate. We don't know, unless you're forcing a trade. We also don't know how Trump's actions may change; he could sweep away tariffs, escalate again, and remain volatile on trade policy with ups and downs on tariffs that create confusion in terms of forming expectations etc.

- Asked about the end of dollar dominance and its role as a safe haven, Powell said "I think the dollar is still the number one safe haven currency. I would say these narratives about decline are premature and over done." Of course, a Fed Chair wouldn't be expected to say anything that would trash the dollar, but I generally agree with the Chair on this matter.

CANADA’S COSTLY DEFENCE AND INFRASTRUCTURE PLANS

What follows is an extension of previous notes (like here in February, plus earlier and subsequent notes) on the potential effects of Canada’s plans to increase defence and infrastructure spending on the bond market. I’ve long been of the view that deficits and bond issuance are being understated in much of the bond analyst community in Canada at first through tariff effects, then through likely stimulus announcements and then through defence and infrastructure plans.

Canada has a plan that PM Carney spoke about again yesterday in this CNN interview. I’m not entirely sure what it is yet, but it has a plan. The plan is to spend a lot of money on defence and infrastructure including critical minerals. Other than missing parts like how it gets implemented and on what will the money be spent, the part that’s missing is who pays for it.

PM Carney has stated that Canada will sign on to a NATO pledge today that will entail spending 5% of nominal GDP on defence by ten years from now which is loosely defined to also include critical minerals projects, airports, roads and ports plus other spending even remotely associated with security. Defence would account for around 3 ½% of GDP and the other stuff would be another 1 ½% to get to the 5% NATO target. I suspect the NATO accountants are scratching their head over the kitchen sink approach to defence spending. Maybe toss in spending on nostalgic Avro Arrow model plane kits to go along with the IT spending and pay hikes that get Canada to 2% of NGDP on defence as the first act.

The first point is how to distribute the spending. Carney’s 5% goal is stated to be targeted for 2035. How to phase this in over time is important to the amounts to be spent. There is no guidance on that part. That leaves us to speculate.

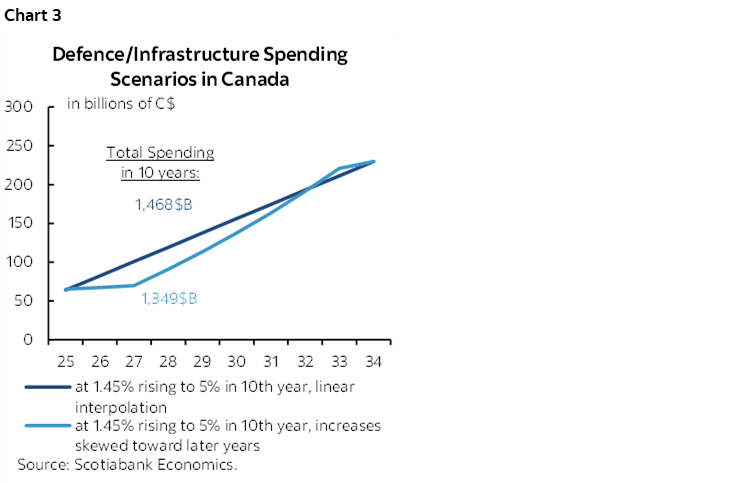

For example, chart 3 shows what happens if we distribute the spending increase from just over 1.4% of NGDP last year to 5% ten years from now using linear interpolation. It shows the straight-line path for the annual spending amounts without controlling for inflation. This is calculated by applying a steady rise in the percentage share of nominal GDP in equal increments each year while assuming NGDP grows by about 4% per year over time (2% real growth plus 2% inflation). It’s not C$150B/year as many stories mistakenly stated; that was just Carney’s response to what 5% of current NGDP would be, but the annual amounts start off less than that and ramped up to considerably more than that amount per year. The grand total would entail spending about C$1.4–1.5 trillion over ten years which assumes a similar defence price index to the overall NGDP deflator that may be understated. In plain English, defence prices may rise faster than overall prices especially given Canada’s weaknesses when it comes to procurement spending and so a considerable portion of the target may be eaten up by higher prices.

Chart 3 also shows an alternative scenario as one among many others absent an actual budget. In this scenario, I’ve held defence spending flat at 2% of NGDP for the first couple of years, and then hiked it by about half a percent per year toward 5% by the ninth or tenth year. In this scenario, defence and infrastructure spending rises by C$1.33 trillion over ten years.

You could also extend that 2% through a longer period with the supporting narrative being that Carney spends enough to get by but waits out Trump’s term only to ultimately fail to meet Canada’s 5% pledge just like it never really attained its 2% pledge in the past. Canada’s defence pledges have a history of not being something its allies can take to the bank. This scenario—and maybe the previous one—is basically the one that strings Trump along long enough to get tariff relief with no real intention of actually hitting 5%.

Still another scenario is that Canada seeks to target 1.5% of NGDP on ‘stuff’ other than direct defence spending—like the ports, roads, railways etc—in a shorter period of time than ten years and achieve the defence part later on to eventually arrive at the 5% target. We don’t know.

We also know that the Canadian government’s procurement programs are a weakness. There is high likelihood that seeking to spend more on defence and infrastructure will only lead to large cost overruns and backed by a global database that tracks these overruns (chart 4). If you had to pick two areas of focus for governments that are most prone to overruns, you couldn’t pick any better than defence and infrastructure especially in a country that manages its purchases so poorly.

Now for the clincher. Who pays? Right, Ottawa will get back to you on that. Somehow Canada has to come up with well over C$1 trillion over ten years to fund such a spending surge, unless there is no serious intent to ever actually hit 5% of NGDP. And there is no plan for this. Not a visible one at least, and there won’t be at least until a Fall budget and perhaps not even then given that forecast horizons in budgets cut out at half of the ten-year horizon for this spending plan. There are only so many choices and they keep bond markets guessing. Here too we are left to speculate, but the street cannot just ignore the issue and stand idly by waiting for updates on the government’s timeline.

Asset sales to the private sector could do a little of it as a temporary consideration but nowhere close to enough and assuming there are buyers. And bear in mind that as someone else buys them, they too must fund the purchases. That either draws on domestic savings or adds to external debt.

Maybe revenues from royalties and mineral rights will be raised but quantifying that is difficult.

Chart 5 shows the implications for program spending and taxes if they are relied upon without inflaming the deficit and bond issuance. You’d need $1.3T+ of spending cuts over ten years. Core program spending cuts are unlikely and I’m skeptical that Canada’s government will go from rapid annual program spending increases to flat in real terms according to Carney’s pledge. Besides, as they roll out pharmacare, childcare, and dental care and seem to remain committed to future planned spending increases, cutting well over $1T in spending over ten years doesn’t seem likely.

Higher taxes are feasible but $1.3T means a lot of tax hikes. Carney has batted away that fear and noted they are cutting taxes now, but that’s for the lowest income tax bracket with trickle through benefits for middle class households. This says nothing about whether corporations and the relatively wealthy won’t be tapped for more. Marginal rates on upper income earners are already high and Canada has lost its relative tax advantage to the US and so taxing more heavily could be a treacherous anti-productivity path.

Bigger deficits are the remaining option. With that goes more bond issuance. It seems highly reasonable to expect Canada’s deficit-to-gdp ratio to rise materially further for an extended period. The Liberal government since 2015 has been relaxed on the deficit and one senses that continues under the current regime. There has been a serial pattern of understating deficit risks in the analyst community.

Which brings us back to my narrative on the Canada rates curve relative to the US. Canada is rich, the US is not, strictly speaking about bond valuations. The BoC is already at around neutral, while the Fed is still materially restrictive and so the better odds for more material medium-run easing are out of the US, not Canada despite the usual wars around the fine-tuning stage of possible Canadian monetary policy actions.

Relative supply could place Canada at a disadvantage to the US curve. The US ‘one big, beautiful bill’ is stuck in the Senate as they scramble to get something through before leaving town for the summer, but the roughly US$2½ trillion in cumulative deficits over the next ten years given CBO costing could be funded in whole or significantly by tariff revenues that the CBO by law cannot include if Trump sets a minimum baseline tariff for all countries. Last evening’s comments by Canada’s ambassador to the US, Kirsten Hillman, indicated that Trump appears to be intent on tariff revenues as part of any deal with Canada which leans to this permanence scenario.

Absent a credible funding plan, however, Canada’s massive spending plans could swamp the market with bond auctions of a bigger and more frequent variety. The present roughly 100bps funding advantage to Canada versus the US in 10s and about 125bps long-end advantage could be vulnerable over time and depending upon budget plans and execution. Our yield curve forecasts into the Fall could be subject to material revision relative to the US depending on what’s in the Budget and how credible any plan appears to be.

I suspect we’ll see some combination of funding plans unfold with higher taxes, at least an attempt at containing operating spending growth howsoever successful in the end, some asset sales, and more debt.

Of course, if the Trump administration is intent upon tariffs on Canadian exports as last evening’s remarks by Canada’s ambassador suggest, then Canada should forget about any quid pro quo. Stuff Canada with permanent tariffs? Ok, then Canada should sell critical minerals to other countries. Forget about the ‘Golden Dome’ that’s extraordinarily costly for unproven technology while Israel’s ‘Iron Dome’ lets through a material number of missiles. Trump won’t even unconditionally stand by Article 5 of the treaty. Ditto for any defence spending surge that jeopardizes the cost of funding to businesses, households and governments themselves while still getting stuffed with tariffs.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.