ON DECK FOR TUESDAY, JUNE 24

KEY POINTS:

- Stocks up, dollar down as risk-on driven by two developments

- Israel-Iran ceasefire stirs market hope, may be failing already

- Three issues Chair Powell’s testimony may address

- Hinging a July Fed cut on one more inflation report is unwise…

- …as three proponents must have their motives questioned

- Canadian CPI: one of two that Macklem placed high emphasis upon…

- …with the focus on the preferred core measures

Stocks are broadly higher and the dollar is broadly softer this morning as risk-on sentiment may have two main catalysts. One is last evening’s Iran-Israel cease fire announced by Trump, confirmed by both countries, and now up in the air again (see below). Two is positioning into Chair Powell’s testimony and how he handles dissenters on his Board. Canadian markets will focus on the CPI update.

IRAN CEASEFIRE VIOLATED ALREADY?

A ceasefire would be good if true and if the goal of containing Iran’s nuclear program has truly been achieved. Unfortunately, that’s in question, while Israel is already accusing Iran of having violated the agreement by firing missiles at Israel that has pledged to retaliate.

I've lost count of Middle East ceasefires that failed. I’ve also lost count of Trump’s failed pledges, like he’s going to end the war in Ukraine. Gaza too. Then Iran, while pledging no more forever wars. Trump 'obliterated everything' except they don't actually know where 'everything' is and it doesn’t seem like anything was truly obliterated. In short, I’ll believe it all when I see it as trust is the commodity in shortest supply on all sides. Iran’s foreign minister isn’t doing the tour of the west’s enemies for nothing. For all we know, just as Trump boasted about moving B2 decoys and his fake two-week notice, Iran’s performative missile attack on a US base in Qatar and its ceasefire pledge may have been designed to create a false sense of security.

FED CHAIR POWELL’S TESTIMONY—ADDRESSING CUT TIMING, DIVISIONS

Chair Powell’s testimony before the House Financial Services Committee could be key for three reasons (10amET).

First, will he revise his thinking on cut timing by making July a ‘live’ meeting? I think that would do more damage than good because it would make the Chair look like he is bending the knee to Trump’s criticisms and catering to the recently dissenting voices on the Board. Nothing material has arisen in the past week that would justify a change of tone by the Chair. He may repeat last week’s communications that emphasized policy is in a good place to evaluate further evidence with the tone suggesting this would take place over several months. He did not indicate last week that July would be a potentially ‘live’ meeting but watch for any reference during written testimony or the ensuing grilling to how a cut could be appropriate ‘somewhat soon’ or ‘soon’ depending on data.

Second, he may weigh address the issue of dissenting colleagues. Two of his Governors (Waller, Bowman) are open to a July cut if the next inflation report merits doing so. Ditto for Kevin Hassett, Director of the National Economic Council in the administration. All three may have impure motives with sights set on becoming the next Fed Chair while seeking to curry favour with Trump. Maybe we've only heard this view from the two on the Committee who are in the -75bps dots for this year and hence a tail minority with 7 saying no cut this year, 2 in the -25bps camp, 8 in the -50bps camp and 2 in the -75bps camp. I suspect Powell will shrug, say they have a right to their opinions, but that the overall Committee felt strongly that policy was in a good place and they could take their time to assess conditions affecting the dual mandate. To signal July is ‘live’ and to cut could bring forward market pricing for a series of cuts that the FOMC may not be comfortable with inviting at this point. Ultimately, the best course of action may be for the other FOMC voices to speak up more aggressively with their views.

But to hinge a cut in July on one more inflation report is not credible in my view:

- First, we've seen plenty of soft patches over several months in recent years, only to see inflation jump again.

- Second, I'd repeat a lack of trust for ytd US inflation data. SA factors are biased. 30% of the basket has been guessed at by the BLS for two months in a row which is double the pandemic peak.

- Third, it's far too soon to evaluate tariffs and broader forces. Inventory stockpiling at pre-tariff prices, absorbing initial effects in profit margins, lagging effects through supply chain contracts, and expectations for trade deals that could drive businesses to look through tariff blips are all among the considerations for why tariff effects on prices may be delayed but still ahead.

- Fourth, it’s an open question whether tariffs are merely a one-off price level adjustment or the spark for another round of inflationary pressures. The US economy is in excess aggregate demand with a positive output gap, inflation expectations are above target, and supply chains are being roiled by trade wars with no clear de-escalation in sight.

- Fifth, the dual mandate also includes the job market and hiring is resilient to date. What I find odd about some disinflationary voices is that they are also of the view that the US economy will continue to grow strongly throughout the trade wars.

The third issue on Powell’s plate is to also watch for any further guidance on capital plans ahead of tomorrow’s Fed Board open meeting on potential changes to the Supplementary Leverage Ratio and enhanced Supplementary Leverage Ratio for GSIBs.

See my weekly for a further preview of this week’s Fed developments.

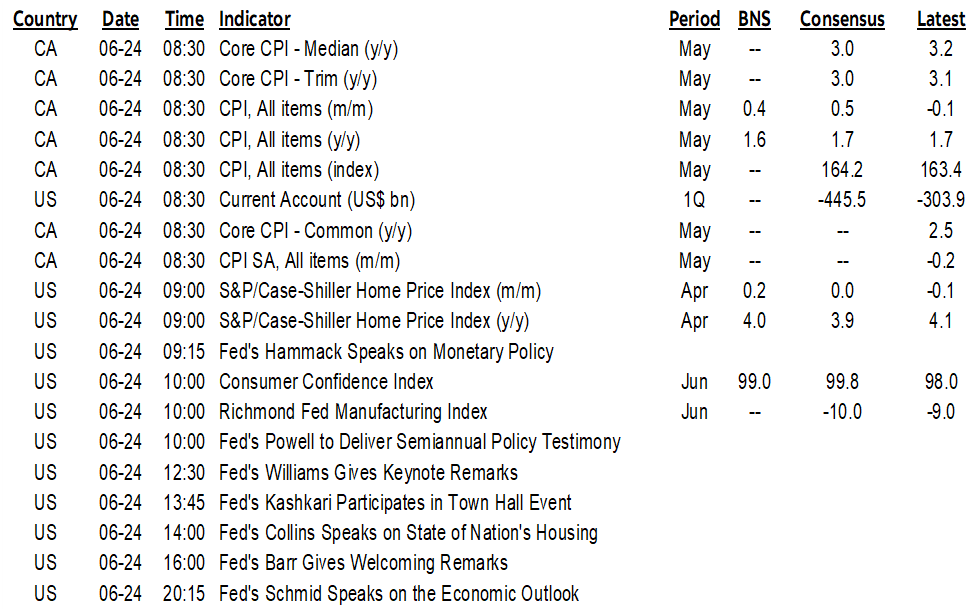

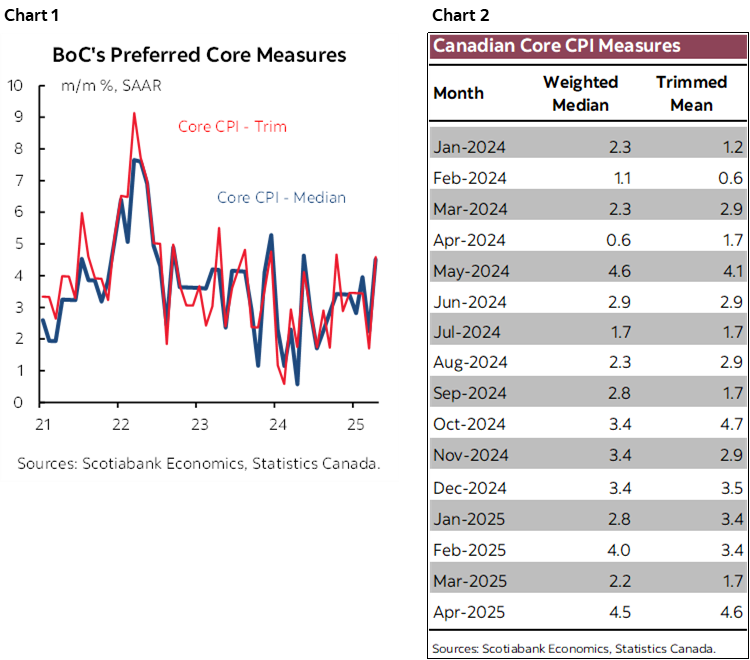

CANADIAN INFLATION—ONE OF TWO REPORTS THAT MAY MATTER

Canadian CPI for May is expected to rise by several tenths in m/m NSA fashion, but key will be the BoC’s preferred core measures (8:30amET). I wouldn’t be surprised to see volatility drive a softer reading after the 4 ½% m/m SAAR increases in trimmed mean and weighted median CPI the prior month, but this month brings added complications. It’s one of two CPI reports before the next BoC decision plus other data on jobs and GDP and the 30-day deadline for a possible Canada-US agreement on trade and security. Canada has been in a prolonged state of high core inflation readings dating back over the past year with no signs that the BoC has contained inflationary pressures to date, let alone addressed forward looking risks. See chart 1 and 2 for evidence. See my CPI preview in the Global Week Ahead for more detail on the estimates and implications.

OTHER STUFF

US consumer confidence in June (10amET) and repeat sale home prices in April (9amET) are also on tap along with the Richmond Fed’s manufacturing index (10amET). Confidence is the most likely factor to be impactful but could be quickly swept aside by Powell’s testimony.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.