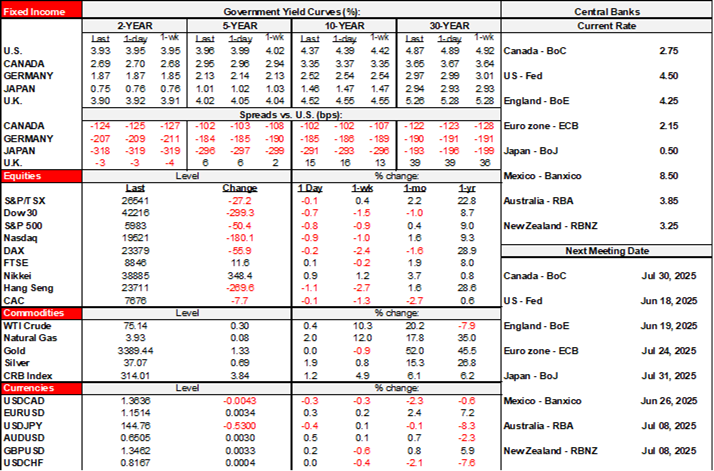

ON DECK FOR WEDNESDAY, JUNE 18

KEY POINTS:

- Markets on tenterhooks, eyeing the interplay between the Fed and Iran

- Iran’s Supreme Leader strikes defiant tone; watch US response

- Fed moving toward easing the SLR in one week

- BoC’s Macklem to speak on tariffs and trade…

- ...and has sounded neutral-hawkish on the topic in the past

- FOMC preview: what to expect in the dots, projections and press conference

- The US job market is resilient…

- ...and why an experienced FOMC should fade recent inflation data

- Riksbank cuts with slightly dovish forward guidance

- Bank Indonesia sits tight again

- UK services CPI eases

- SARB watchers took down dovish inflation data

- US housing starts sink, jobless claims have mildly picked up

Markets are feeling uneasy with divided outcomes across asset classes on what could be a big day for developments at the Fed, in Iran, and at the BoC while digesting headlines on Fed regulatory moves and overnight developments. US Ts are outperforming with a bull flattener that is also bringing a dearer front-end that might be a dicey bet into the FOMC. Stocks are little changed across global benchmarks. The dollar is also mixed with some narratives around local central bank decisions and data driving currency moves.

IRAN’S SUPREME LEADER STRIKES DEFIANT TONE

Markets remain on tenterhooks awaiting further possible developments in Iran. The Supreme Leader Ayatollah Ali Khamenei just aired a televised address that was defiant in its tone, warning that it won’t surrender and that US actions will be met with force. It may further inform the US stance and any joint actions by Israel and the US with the potential for headlines to mess up the Fed reaction if any.

FED MOVING TOWARD EASING THE SLR

A contributing factor to outperformance of US Treasury yields is last evening’s headline that the Fed will hold a meeting next Wednesday to discuss cutting the Supplementary Leverage Ratio by as much as 1.5 ppts.

BOC’S MACKLEM TO HOPEFULLY CLARIFY HIS STANCE

BoC Governor Macklem speaks on ‘tariffs, trade, employment and inflation’ and will offer a press conference afterward. The speech will be released at 11:15amET and the press conference will be held by around 12:40pmET, give or take. Key will be whether he clarifies his stance during the June decision’s press conference that on the one hand said they didn’t have confidence in the outlook to provide forward guidance and therefore suggesting no rush to act, versus emphasizing the next two CPI reports that are due before the July 30th decision which suggested the meeting may be ‘live’.

FOMC—WILL THEY REDUCE PROJECTED CUTS?

Then it’s the Fed. The statement (2pmET) will be accompanied by an updated Summary of Economic Projections (SEP) including a fresh ‘dot plot.’ Then at 2:30pmET, Chair Powell holds his customary press conference for around 45 minutes. See my preview here and more comments below.

A policy rate hold with no changes to balance sheet policies are widely expected. Key will be the SEP’s projections for growth, inflation, and the unemployment rate and the fresh dot plot.

I wouldn’t be surprised if the Committee removed one cut from its dots this year, but it’s uncertain they will. Their 50bps of cuts in 2025 in the March plot has five remaining meetings in which to deliver them. June and probably July seem out. It’s unclear that the Committee will have the confidence to cut twice in the remaining three meetings after July. My hunch is they could trim that down to one which would be consistent with the views expressed by some members, while others have indicated they are still fine with the March projection.

Why reduce the pace of easing? Nonfarm payrolls remains resilient especially in weather-adjusted terms. 139k official payrolls in May was 220k according to the San Fran Fed’s weather-adjusted payroll gain. The FOMC will also expect a cooler breakeven rate of payroll expansion as the labour force cools through tighter immigration policy. Overall, I don’t expect Powell to sound concerned about the full employment side of the mandate at this meeting.

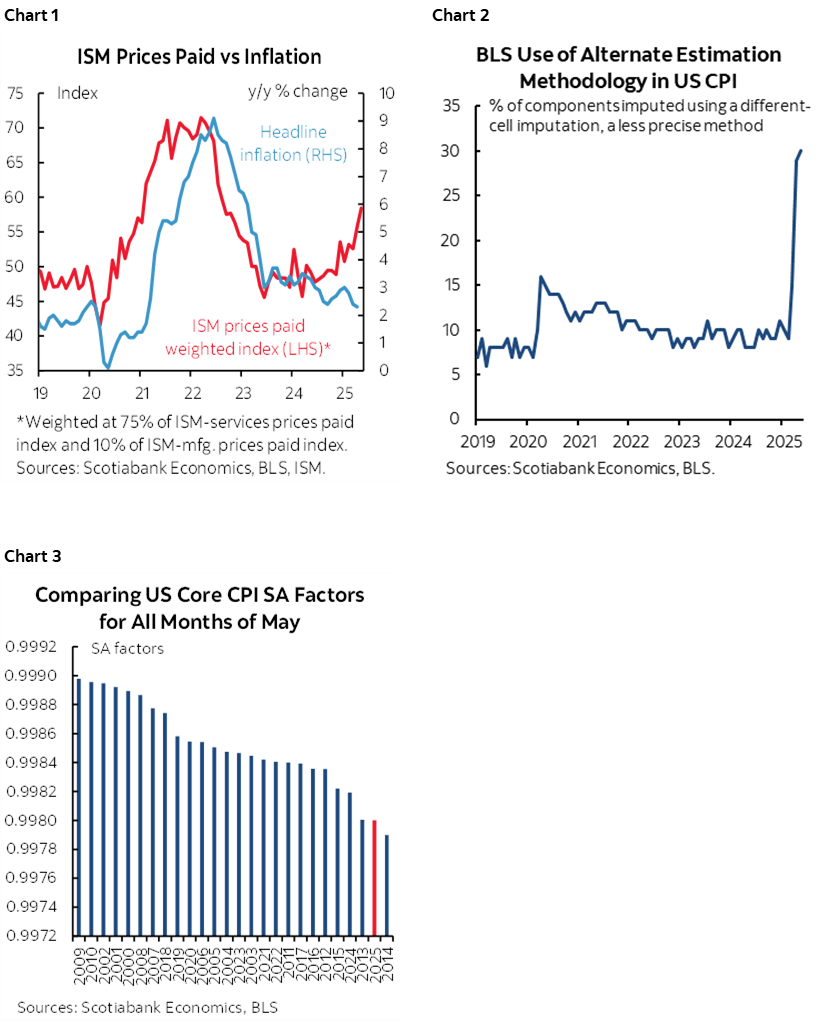

As for the price stability side of the dual mandate, the FOMC has seen many false head fakes on soft core inflation, only to be surprised again even absent any tariff effects. They’re experienced enough to fade the data and require a lot more. On said tariff effects on inflation, it’s ridiculous to dismiss them based on inflation data to date since we can’t tell whether prices have been held at bay because of no pass-through effect now or ever, or if that’s just temporarily stalled by front-running orders into inventory at old prices and by absorbing some of the effects in profit margins. Retailers may try to smooth out the effects on prices over time and, in an expectations sense, adjust prices carefully in light of the possibility that tariff de-escalation lies ahead over coming months. Prudence would require an open mind to pass through especially given the number of major firms indicating they are indeed raising prices plus the soft data such as ISM price signals that lead inflation (chart 1). The Fed may also be on the verge of another oil price shock pending volatile developments in the Middle East as higher oil and tariffs risk reinforcing one another’s inflation effects. Last, there is also the question of confidence in data; I don’t have any confidence in US inflation data given the 30% share of the basket that is now guesswork due to budget cuts (chart 2) and the fudged seasonal adjustment factors that assume today’s seasonality is the same as it was emerging from the pandemic in light of the recency bias to how they are calculated (chart 3).

Additional issues in the press conference could include two other things. Someone will probably ask about a proposal by a few US Senators for the Fed to stop paying interest on reserves. Anyone who knows anything about US monetary policy and the Fed would expect Powell to bat that away and quickly move on. Secondly, Powell may be asked about last evening’s SLR headlines, so watch any guidance on timing of implementation, magnitude of change, and composition of change as it may affect other asset classes. In fact, the SLR comments might well carry the day in terms of market effects coming out of this meeting.

DOVISH RIKSBANK

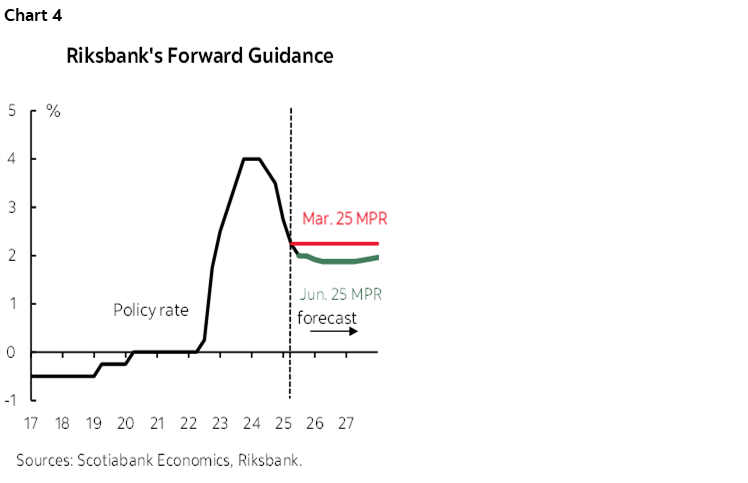

Sweden’s Riksbank cut its policy rate by 25bps as widely expected. Guidance was more dovish than expected as the statement noted that “The forecast for the policy rate entails some probability of another cut this year.” Their explicit forward guidance is on the fence with only a few basis points of a cut reflected by year-end while the two alternative scenarios are split between materially more cuts and hikes should inflation surprise higher (chart 4).

GUARDED BANK INDONESIA

Bank Indonesia held its policy rate at 5.5% as many expected, although there was a significant minority expecting a cut. Guidance continued to point to the usual concerns about the rupiah and financial stability, tariff concerns, while the growth outlook was revised a touch lower.

UK SERVICES CPI EASES

UK CPI came and went without much fanfare. Headline CPI was on the screws at 0.2% m/m and slipped to 3.4% y/y (3.5% prior, 3.3% consensus). Core CPI was on consensus at 3.5% y/y (3.8% prior). One slightly more dovish hint came through CPI services that fell to 4.7% (5.4% prior, 4.8% consensus).

RAND SOFTENS ON WEAKER CORE CPI

South African Reserve Bank watchers got a bit more of a dovish CPI reading than expected. Core CPI was flat against expectations for a mild up-tick and that kept the y/y rate at 3% (3.1% consensus). There is another CPI report due before the July 31st SARB decision.

MINOR US DATA INTO THE OPEN

US housing starts in May fell by 9.8% m/m SA in May (consensus –0.8%) only partly due to upward revisions to the prior month (+2.7% m/m instead of 1.6%). Initial jobless claims landed at 245k last week which is slightly significant in that it makes three weeks in a row of readings around that range as a slight pick-up from the 220s range previously.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.