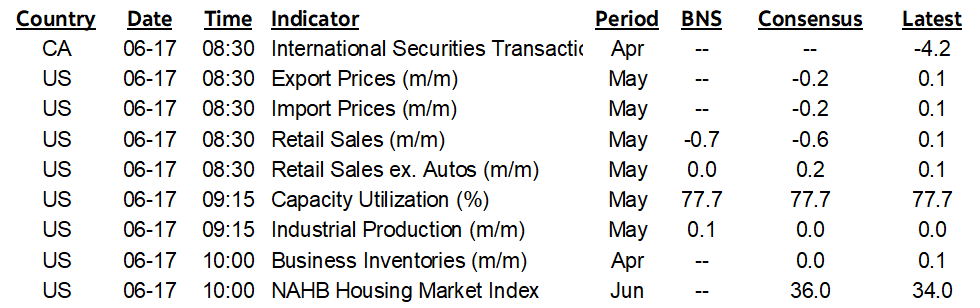

ON DECK FOR TUESDAY, JUNE 17

KEY POINTS:

- Oil and gold up, stocks down as markets await developments in Iran

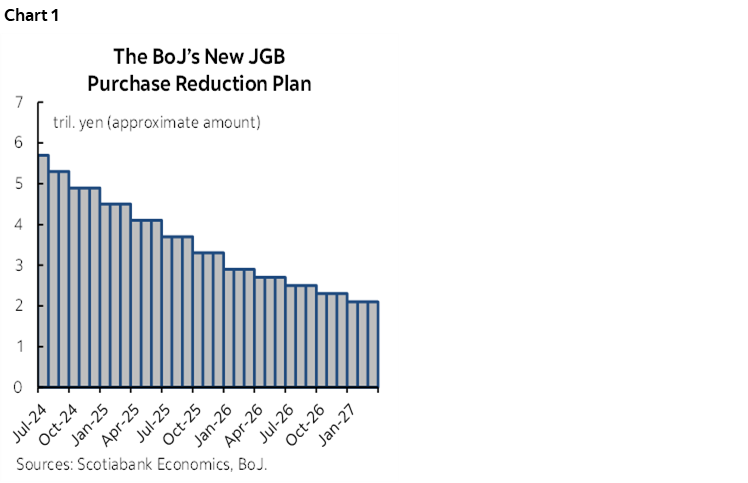

- BoJ scales back JGB purchase reductions starting in April 2026

- Debating the signal from Trump’s G7 departure

- US retail sales are expected to be weak

- BoC’s SoD: informing messy forward guidance, or stale?

- BoC to update CPI weights today for next week’s May release

- BCCh to hold with cut risk after the close

Risk-off sentiment is rearing its ugly head once more. Stocks are broadly lower with losses of between about ½% and 1¼% across US futures and European cash markets, but with the energy-rich TSX performing a little better. US Ts are a touch richer by 3–4bps across the curve while Canadian government bonds are slightly less rich than US Ts at the front-end. The USD is mixed against major crosses. Oil is up by just over a buck and gold is up by a few bucks.

The main driver is uncertainty around further developments in the Middle East. Trump says he had to split the G7 Summit early because of developments in the Middle East while repeating Israel’s warning for Iranians to leave Tehran. It could just as well have been a ruse designed to cover his boredom, or that he was feeling awkward.

The BoJ did what was expected with no real impact. US retail sales, fresh CPI basket weights from StatCan and the BoC’s Summary of Deliberations are on tap.

BOJ COMMITS TO SLOWER PATH OF PURCHASE REDUCTIONS

The Bank of Japan held its policy rate, continued to sound data dependent on hike guidance, and reduced planned cutbacks in bond purchases starting next April.

Its annual review of the JGB purchase program presented a new plan for purchase reductions (here, last year’s here) that tapers the flow of JGB purchases starting in April 2026 to 200 billion yen per quarter on a monthly basis (chart 1). The current pace of quarterly reductions is 400 billion yen quarter which remains intact until March 2026. The BoJ reissued annual guidance that it will reassess this plan at the June 2026 meeting and repeated the same sentence it had last year that said “In the case of a rapid rise in long-term interest rates, the Bank will make nimble responses by, for example, increasing the amount of JGB purchases.” The yen was not noticeable impacted. The JGBs curve slightly bear steepened. There were minimal effects on meeting pricing through to the end of the year with markets still only pricing a cumulative 14bps of a hike by year-end.

NEW CPI WEIGHTS FROM STATCAN

Statcan will refresh CPI basket weights this morning for inclusion in next week's May CPI report (8:30amET). It's the annual process, this time updating to the composition of spending in 2023 instead of 2022. Lower weights are likely on furniture, household appliances and vehicles. Higher weights are likely on shelter via mortgage interest and rent partly offset by replacement cost, air transportation, travel tours, other cultural and rec services, and personal care services. Usually there is a small to negligible effect on CPI at the link month.

BOC’S SOD MAY ALREADY BE STALE

The Bank of Canada will release its Summary of Deliberations to the discussions leading up to the June 4th decision to hold the policy rate (1:30pmET). Key may be any further clarity around forward guidance. If that isn’t shared, then it may be in Macklem’s speech tomorrow. During his post-decision press conference, Macklem said they did not have the confidence in the outlook to provide any forward guidance—not that it’s very useful when they do—but then proceeded to provide a form of forward guidance by emphasizing the importance of the next two CPI reports that are due before the July decision. So, does that mean your July decision is ‘live’? After its core measures in m/m SAAR terms have been hot dating back over a year, suddenly it’s down to just the next two CPI prints? That would be so Macklem, ready to opportunistically pounce on any excuse to turn dovish, yet this whole issue could be a Macklem thing that won’t appear in the SoD. All that said, the comments could well be stale on arrival in light of guidance from the G7 Summit that PM Carney and Trump are striving toward a trade and security deal within 30 days—and therefore before the July 30th BoC decision and MPR.

US RETAIL SALES TO DOMINATE

Any further remarks out of the G7+ Summit and US retail sales will be the two main calendar-based developments today.

US retail sales figures for May (8:30amET) are expected to soften based on lower new vehicle sales and soft CPI and its components, but key will be expectations for modest growth in nominal core sales ex-autos and gas. For purposes of tracking total consumer spending, key will be whether or not the retail sales control group bounces back from the drop in April for the second decline of the year. Recall that the control group is how retail translates into consumption within GDP accounts and it excludes auto dealers, building materials and gas stations.

The US will also release import prices for May (8:30amET) and industrial output for May (9:15amET).

On the geopolitical side of things, further attacks are ongoing. Iran’s mixed signals that it may be trying to deescalate are not convincing the Israelis after Iran withdrew from the nuclear non-proliferation treaty and launched more missile strikes on civilian targets in Israel overnight.

After today’s close we’ll hear from Chile’s central bank that consensus expects to hold but a minority including our Chilean economists expect to deliver a 25bps cut (6pmET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.