ON DECK FOR MONDAY, JULY 7

KEY POINTS:

- The dollar is broadly firmer post-payrolls amid tariff headlines

- The US administration is pushing out its tariff threats again…

- ...as revisiting ‘Liberation Day’ tariffs lacks credibility

- Oil shakes off OPEC+ theatrics

- Why US payrolls were solid

- German factories sprang back to life

- Krona outperforms after Swedish inflation surprises

- Global Week Ahead highlights for a light calendar

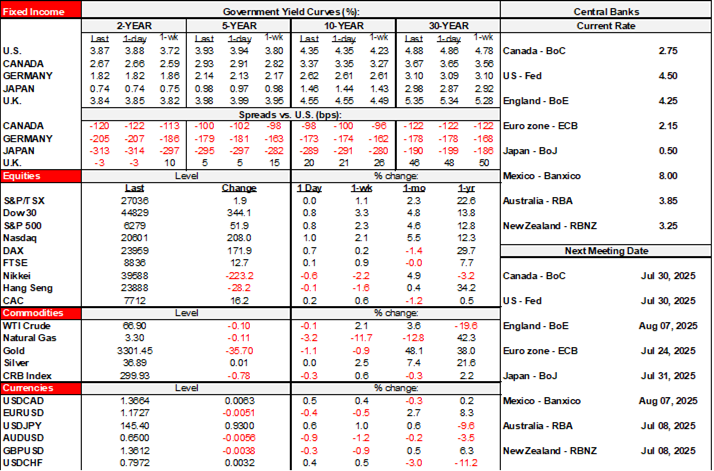

Light developments are driving muted action across most global asset classes to kick off the new trading week. The overall week should be relatively light in terms of calendar-based macro risk.

The dollar is firmer against most major crosses. Sovereign bond yields are little changed with minor underperformance across EGBs relative to US Ts. The US long-end is underperforming after the US administration achieved its ‘One big beautiful bill’ that modelers estimate will add US$3.2 trillion to primary deficits over the next 10 years in highly regressive fashion that will negatively impact much of Trump’s base (here, plus here for subscribers to The Economist). US equity futures are slightly negative, TSX futures are slightly positive, European cash markets are little changed, and Asia-Pacific markets ranged from small losses in Japan and HK to little change elsewhere. Oil prices are little changed after OPEC+ increased August’s targeted output by 548kbpd this weekend; we’ll see how enforceable the target may be.

ANOTHER PUSHED OUT US TARIFF DEADLINE

The US administration appears to be pushing out its tariff warnings again. Few may be surprised. US Treasury Bessent said yesterday that failure to strike trade agreements with the US by August 1st will result in tariffs going back to April 2nd ‘Liberation Day’ levels. That pushes out this Wednesday’s deadline by several more weeks. Trump vowed to have more to say on tariffs today. The pushed out deadline probably isn’t a credible threat given the pattern of behaviour by the Trump administration and given the severe damage to the US and global economies that would result from that day’s sky-high tariffs.

I’ll say it again: The rest of the world understands the US political cycle better than the US administration and it’s Trump that is under pressure into midterms more than the other countries. Any ‘deals’ with the US administration are likely to be token ones as major trading partners resist longer-term damage emanating from deeply misguided US economic policies.

WHY US PAYROLLS WERE SOLID

Why were US nonfarm payrolls resilient again in June last Thursday before US clients headed to the exits for a long weekend? Other than a surge of hiring across state and local governments, the 147k payroll increase was close to my above-consensus estimate (160k) and was primarily due to the fact that the seasonal adjustment factor was the highest for a month of June on record (chart 1). Chart 2 shows what would have happened at any other SA factor. This conformed to the expected recency bias in how seasonal adjustment factors are calculated by skewing them to the experience of recent years. I remain deeply skeptical toward such SA adjustments and think it’s wrong of Federal Reserve Chair Powell to have sounded dismissive toward the issue with no elaboration as to why in his June FOMC press conference.

LIGHT OVERNIGHT DATA

German factories sprang back to life in May. Industrial output was up by 1.2% m/m SA (-0.2% consensus), thereby reversing most of the decline in April. Most of the gain came through capital goods.

Sweden’s krona is outperforming all other currencies and its short-term rates are underperforming all other markets after CPI jumped 0.5% m/m in June (0.1% consensus) with underlying CPI ex-energy up 0.7%.

THE WEEK AHEAD’S HIGHLIGHTS

Now that the US tariff deadline has been pushed out again, the rest of the week’s expected developments are likely to pale by comparison.

- Canada: Friday’s jobs report will be the main feature. I’ll have my estimate soon, given I was away last week. A light consensus presently ranges from -10k to +10k with 0k being the median call.

- US: Minutes to the June 17th–18th FOMC meeting arrive on Wednesday afternoon. The US data line-up is very light.

- Central banks: Five regional central banks will weigh in this week. The RBA is expected to cut 25bps overnight tonight. The RBNZ is expected to hold at 3.25% tomorrow night (ET). Consensus is divided between a 25bps cut and a hold for Bank Negara Malaysia on Wednesday. The Bank of Korea is forecast to hold at 2.5% on Thursday. Peru’s central bank is expected to hold at 4.5% on Thursday.

- Inflation: Several countries will update inflation figures for June this week. Colombia releases tonight. China is out tomorrow along with Chile and Taiwan. Mexico (Wednesday) and Norway (Thursday) will follow.

- Other data: Germany updates trade figures for May tomorrow. The UK monthly data dump arrives on Friday including May readings for GDP, industrial output, services, and trade.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.